Adidas AG – The Best Turnaround Story in Europe? I see Room for 17% annualized returns

Margins are back, Yeezy is gone, and growth is compounding — but the market hasn’t priced it in, with adidas trading at a 0.7x PEG.

Earlier this week, I sent out my list of 5 stocks that are too cheap to ignore right now to paid subscribers. Real opportunities. No hype. Just stocks with big upside and strong fundamentals.

If you missed it, check it out through the hyperlink above! The list is also partially available to free subscribers and will be fully available to free subs by May 31st.

This list will be updated every two weeks and sent immediately to Paid subscribers (made available to all subscribers 10 days later)

On that note, let’s delve into adidas!

It’s safe to say Adidas has been going through a rough patch, as is very well reflected by its share price performance, with shares having returned only 10% over the last five years, and for good reason.

Over the last 5-10 years, Adidas has been plagued by years of mismanagement, operational flaws, and, most notably, a lack of innovation and a poor design team. Yes, the company has also faced a toxic mix of headwinds that weren’t entirely within its own control, but adidas has also been falling short operationally for most of the last 5-10 years, facing competitive pressure from Nike, Puma, and New Balance, among others, and has been struggling to keep up with competitors in terms of product innovation, particularly in performance sportswear and athleisure.

As a result, the second-largest apparel brand has been bleeding market share during most of this period across all segments. For example, in footwear, which is its most important market, Adidas has been falling significantly behind Nike over the last decade. Today, Nike is over 2x as big in terms of revenue following years of market share losses by adidas and brilliant execution by Nike.

Today, Adidas holds a market share of roughly 10.9% in the footwear industry, which remains the second-largest globally. However, this share has declined by a whopping 300 basis points since 2019, representing extremely poor performance; there is no denying it.

And the pain extends beyond footwear. You see, whereas adidas was the largest apparel brand in market share back in 2011, capturing 11.2% of the market, ahead of Nike’s 9.9%, this share has been declining ever since, with Nike surpassing it and newer brands like Lululemon and Under Armour also gaining market share.

Again, this is all the result of extremely poor execution, with Adidas failing to match peer innovation, numerous promotional mishaps, and simple strategic mistakes, which all put it on the back foot.

In addition to this, the company also faced considerable headwinds that weren’t entirely within its control. This includes the COVID-19 pandemic, which had a significant impact on adidas due to its extensive exposure to the Chinese market. However, the biggest impact in recent years came from the sudden ending of the Kanye West partnership, which turned from an incredible success into a complete disaster in no time.

In 2022, Adidas faced significant controversy and financial losses due to its partnership with Kanye West, following his antisemitic statements, which led to the company being forced to immediately end the partnership. However, this left adidas in an extremely vulnerable position, with the company losing its most famous brand ambassador, its best-selling and most profitable product line (accounting for 5% of annual revenue and a quarter of operating profits), and being left with billions worth of Yeezy inventory, which was a massive blow to not only its brand and top line, but also its balance sheet and profits.

As a result, adidas hit a new low, reporting an operating loss for the first time in over 30 years, perfectly accentuating how much this company and beautiful brand have been struggling. This likely was the company’s most challenging period in its 75-year history. It reported its first operating loss in over 30 years, lost market share across the board, and failed to revitalize its brand image, particularly among younger generations.

Alright, that then brings me to the good news, because there is some (surprisingly)!

As I outlined in my initial deep dive into the company back in August 2024, under its new rockstar CEO, Adidas is actually working on achieving a successful turnaround, and it’s doing rather well, with growth accelerating throughout 2024.

You see, after years of struggles, adidas announced a CEO change in 2023. Kasper Rørsted, adidas CEO since 2016, left the company to be replaced by Bjorn Gulden, then-acting Puma CEO and a former adidas employee.

Just how happy were shareholders with this news? Shares gained over 30% in the few trading days following the news, and rightfully so. Gulden is a rockstar in the sector. During his tenure at Puma, he led the struggling brand to remarkable success with a differentiated strategy that focused on enhancing brand visibility and increasing availability.

The result? During this tenure, revenue almost tripled, as did the company’s market cap and share price. For reference, during his eight years at the company, revenue grew at a 14% compound annual growth rate (CAGR), and footwear revenue more than tripled.

In his time at adidas so far, Gulden has employed a similar strategy. He has led the culture within adidas to shift quickly to a far less bureaucratic environment, enabling it to operate more effectively. Additionally, he has quickly abandoned the DTC strategy, once again embracing independent retailers to expand Adidas’ brand and product availability, which had declined in recent years.

So far, this renewed strategy and focus have been paying off handsomely. While Nike has struggled in recent years (sticking with the DTC strategy until recently), adidas is firing on all cylinders, taking market share across all product categories, signing massive brand ambassodors, and outgrowing most of its peers, as the adidas brand appears to have been revitalized.

Meanwhile, Gulden still has a mighty brand to work with. Adidas is still one of the world’s top apparel and footwear brands. The brand's distinctive three-stripe logo is recognized worldwide, symbolizing quality, durability, and sportiness. In fact, it’s ranked #51 on Interbrand’s list of most valuable brands, making it the 5th most valuable apparel and fashion brand, trailing only brands like Nike and Louis Vuitton.

Taking all of this into account, along with the great promise adidas showed under Gulden, I named adidas a great turnaround candidate back in August, rating its shares a buy. Since then, the company has far outperformed expectations, delivering even better financial results than I had anticipated, prompting analysts to further revise their financial projections upward.

However, even as Wall Street analysts have considerably raised their medium-term financial estimates in response to the company’s better-than-expected performance over recent quarters and the strong progress it’s making on its turnaround plan, the Adidas share price is essentially flat from when I last covered them back in August, at €219 per share.

In other words, despite the company performing exceptionally well and showing considerable long-term promise with its revised strategy, shares have actually become quite a bit cheaper.

Why? Well, this is where Trump’s tariff plans come into play. You see, countries like Vietnam, Indonesia, and China together account for 62% of adidas production, and with these hit with insane tariffs, adidas was, seemingly, facing incredible cost-related headwinds.

However, most of this pressure has now eased. Not only have the majority of these tariffs been delayed by 90 days to leave time for negotiations, but adidas management has also downplayed the potential impact. First of all, as of 2024, only 22% of adidas’ revenue is derived from the U.S. Second, only 5% of adidas’ U.S.-sold products are manufactured in China, making the actual effect far less significant than feared.

And with countries like Vietnam and Indonesia unlikely to face heightened tariffs again after this 90-day period, given their willingness to negotiate, I don’t think adidas shareholders have much to worry about. Confirming this is management’s own confidence, with Gulden reaffirming his expectation for at least 10% growth for the adidas brand in 2025, while operating profits are expected to improve to between €1.7 and €1.8 billion. In other words, management remains really confident.

So, with concerns overblown, adidas executing strongly, and shares priced lower, are Adidas shares still a good buy, or has the operating environment worsened too much? Is it still a compelling turnaround pick?

Let’s find out by delving a little deeper into the numbers and developments!

Adidas truly is firing on all cylinders.

Since I last covered the company in August, it has delivered several excellent quarterly reports, with improving margins, strong double-digit sales growth, and visible market share gains.

In its latest Q1 quarter, the company once again delivered better-than-expected results, despite some weakness in the U.S. consumer market, as it continues to make substantial progress toward its 2026 goals.

The company is seemingly the hottest apparel brand out there right now, as the company’s branding efforts are paying off big time. High promotional investments are growing brand visibility and stature. The company has signed massively popular Latin American artist Bad Bunny to its brand ambassador roster, which is giving the company a massive boost, particularly in Latin America.

Meanwhile, the company is also finally outbidding Nike again. For example, adidas signed a very lucrative deal with English football club Liverpool, the reigning champion, replacing Nike effective August. Additionally, adidas replaced Tommy Hilfiger as the official kit sponsor of the Mercedes F1 team, providing the brand with terrific visibility across various sports, something the company had lacked in recent years, as it had failed to outbid Nike in many instances and had been solely focused on a handful of sports.

What we are seeing now is the execution of a much better strategy. As a result, in the footwear market, adidas is the most popular brand right now, with notable success in the Samba, Gazelle, and SL72 product lines. Meanwhile, the company is also innovating at a high level, introducing new high-end product lines, limited editions, and collaborations to generate excitement for the brand and keep customers engaged.

It’s these actions that are putting adidas back on track. The company is maximizing the potential of its popular product lines, continues to innovate in sports categories, and is significantly enhancing brand visibility.

As a result, adidas is, for the first time in a long time, showing gains in market share. For reference, while Nike’s market share in the global sportswear market has declined to 14.1% (from 15.2%), according to recent data, adidas has seen its share increase to 8.9% from a previous 8.2%.

Now, the company isn’t suddenly conquering the market or anything, but it is showing solid progress, even as it faces intense competition from emerging brands like New Balance, On Running, and Hoka.

Driven by this strong underlying performance and improved execution, revenue growth has been strong. In Q1, adidas reported currency-neutral growth of 13% YoY or 17% excluding some final impact from Yeezy. This is absolutely brilliant growth, especially considering the somewhat challenging operating environment, with consumer sentiment and spending not so impressive.

Since early 2024, adidas has been delivering solid growth numbers, as visible below.

Breaking down Q1 growth a bit further, adidas reported that growth was supported by healthy market dynamics across all regions. In North America, revenue was somewhat less impressive at 3% YoY, but excluding Yeezy and focusing on the actual adidas brand, growth actually was 13% YoY, which is quite remarkable, considering the weakness of the U.S. consumer reflected in the latest numbers from Nike and Lululemon – adidas is outpacing both.

Meanwhile, the company’s traction in Europe remains strong, with 16% growth for the adidas brand in Q1. Additionally, China was up 14%, highlighting another region where adidas is significantly outperforming its peers and capturing market share. Finally, LatAm is also doing very well, in part thanks to the influence of Bad Bunny, but also thanks to growing marketing efforts. In Q1, this resulted in an impressive 27% growth, bringing emerging market growth to 25% YoY.

In other words, adidas is seeing strength across all regions.

Meanwhile, adidas’ wholesale strategy is also clearly paying off. The wholesale channel continued to be the fastest growing in Q1, registering 18% YoY growth. Adidas retail stores also saw strong growth of 13% YoY, offset by a 3% decline in e-commerce sales, although this would be up 18% YoY excluding Yeezy.

Finally, breaking down revenue by product category, footwear once again led with 17% year-over-year (YoY) growth, thanks to the strong traction of adidas’ largest and most popular lines. Meanwhile, apparel growth recovered strongly to the high-single digits, though weakness persisted somewhat as management doesn’t want to flood an overheated apparel market, as this could lead to unnecessary discounting to burn through inventory. Ultimately, this now means footwear accounts for 61% of adidas revenue, followed by apparel at 32% and accessories at 7%.

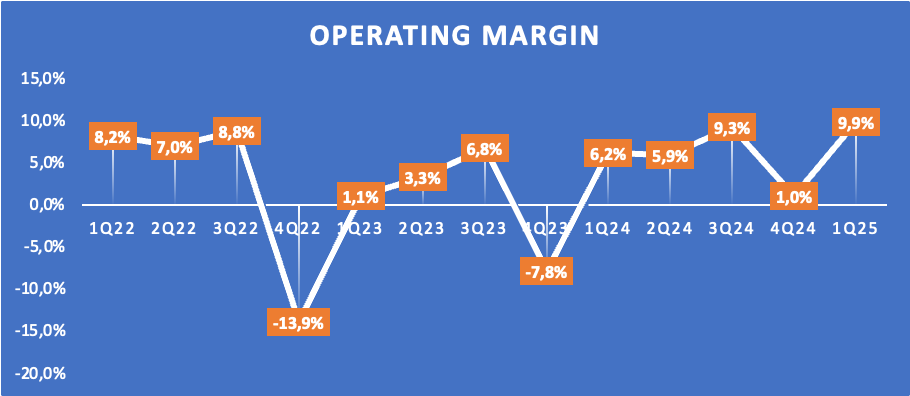

Moving to the bottom line, adidas is showing solid and steady progress as well, with both the gross and operating margin at a multi-year high.

The gross margin in Q1 hit 52.1%, up 90 bps YoY and up 160 bps excluding Yeezy. As shown below, adidas is making solid progress on its margin profile, driven by an improving top-line performance and strict cost management. More volumes are leading to operating leverage, and according to management, Asian factories are functioning much more efficiently. Additionally, the promotional cadence has been limited due to strong demand, and the company has not faced any foreign exchange headwinds, resulting in a clean and strong margin performance.

Meanwhile, despite strict cost management, adidas has continued to make significant investments in marketing. Marketing expenses increased by 14% year-over-year (YoY) and now account for 12% of revenue. Additionally, overhead expenses increased by only 3% year-over-year, demonstrating solid cost control.

Ultimately, this resulted in an operating profit of €610 million, representing an 82% year-over-year increase and a 9.9% operating margin, up 370 basis points year-over-year. This shows very impressive progress by adidas, only 2 years into its 4-year turnaround plan, already pushing against its 10% operating margin target for 2026.

Further down the line, this resulted in a net income of €436 million, up 155% YoY. This translated into a very impressive EPS of €2.44.

Moving to the balance sheet, we can see adidas’ inventory is up 15% YoY, in line with management’s target. Adidas is now targeting slightly higher inventory for the adidas brand to fuel continued double-digit growth.

Adidas ended Q1 with a total cash position of €1.4 billion, down from €2.4 billion at the end of Q4, as the company is investing heavily in its business. Meanwhile, adidas also holds roughly €5.7 billion in debt on the balance sheet, leaving it in a considerable net debt position, which isn’t ideal.

I am not overly concerned at the moment, but I would like to see this leverage trend decline over time.

Making up the balance so far, I am actually really pleased with the progress adidas has made since mid-2024, as proven by the solid financial numbers delivered over recent quarters. The company is firing on all cylinders, and the adidas brand is the hottest in apparel out there right now, leading to market share gains across the board. Management is making good on its promises and is delivering. We can’t wish for much more.

Before we move on, just a quick word…

Want more out of your subscription?

Get exclusive stock picks, premium research, timely earnings breakdowns, direct access to my watchlist, thinking, and full portfolio through InvestInsights PRO — built for serious long-term investors who want an edge.

Deeper dives. Sharper takes. Full insight into my actions.

InvestInsights PRO - $7.50/month ($70/annually)

An additional 2-6x/month premium stock analysis.

Full insight into my own portfolio (15% return CAGR since 2022).

Monthly portfolio updates + Instant transaction alerts (Fully transparent)

A complete overview of all my target prices and ratings (Excel file).

2x/month The Watchlist Report

Instant access to earlier premium analysis on, for example, Adobe, Thermo Fisher, Spotify, and The Trade Desk.

Outlook & Valuation

As I mentioned earlier, despite current headwinds, including a weakening consumer, concerns about a U.S. recession, and the looming threat of a trade war, adidas management remains fairly confident. Adidas continues to aim for double-digit growth in 2025, excluding Yeezy, and continued market share gains. Meanwhile, the operating profit is expected to be between €1.7 billion and €1.8 billion.

Crucially, this guidance now includes the potential tariff impact and changing demand conditions. Adidas has rerouted products coming out of China to other markets than the U.S. to avoid a large tariff impact in recent and coming months. As a result, adidas has so far seen no need to raise prices to offset tariff-driven cost increases.

Of course, if Trump fully reinstates his earlier announced reciprocal tariffs, adidas could be hit harder than it currently estimates; however, I believe this to be highly unlikely, considering the backlash it would have on the U.S. economy and Trump’s presidency. Also, even if the U.S. economy weakens much further, this is still only 20% of adidas’ business, allowing it to offset weakness here with strength in other regions, like Europe and LatAm, which should be much more isolated from these headwinds.

Anyway, adidas’ current guidance seems fairly robust, especially following the strong Q1 performance. According to management, if it weren’t for the sudden tariff increases announced in Q1 and their potential impact later this year, the strong Q1 performance would have led to a guidance raise on both top and bottom lines. Therefore, adidas’ current guidance takes into account some potential downside later in 2025.

Ultimately, taking into account this guidance, adidas’ remarkably strong performance over recent quarters, and macroeconomic developments, I can safely say I was too cautious back in August. Therefore, I have significantly increased my FY25 estimates for both revenue and EPS, now assuming high-single-digit revenue growth and rapid margin expansion.

At the same time, my FY26 estimates aren’t much higher compared to before, as I assume some lingering economic weakness in 2026. However, this is expected to recover by 2027, allowing adidas to experience strong sales growth through 2028. Meanwhile, the bottom line is expected to continue improving rapidly, resulting in a very impressive EPS outlook through the end of the decade.

Here are my full and updated projections:

With financial projections revised upward and adidas trading at nearly the same price as it did back in August, at €214 per share, adidas shares have actually become slightly cheaper, even as the company has outperformed expectations and is showing rapid progress. This performance difference can be mainly attributed to recent tariff headwinds, which pushed shares down all the way to €186 per share in early April.

However, as pointed out several times now, the actual impact is unlikely to be meaningful, so this lower share price, still below a recent February high of €263 per share, isn’t easily justified.

Based on the projections above, adidas shares now trade at roughly 28x this year’s EPS, which sits roughly in line with Nike and well above Lululemon’s 22x multiple. However, out of the three, adidas has by far the best-looking profit outlook and is currently showing the strongest performance. For reference, using a growth-adjusted PEG, adidas shares trade at just a 0.7x multiple, which is generally perceived as deep value territory (anything below 1x).

In other words, the current share price does not accurately reflect the current profit outlook for adidas, as estimated growth has not been fully priced in.

So, are adidas shares a buy?

Using a PEG of 1x and a 24x long-term P/E multiple, which I believe are still quite conservative estimates, not fully reflecting adidas’ excellent execution and growth outlook, I calculate an end-of-2027 target price of €322 per share. From a current share price of €214 per share, this represents potential returns of 17% annually (CAGR), which is pretty neat.

So, yes, I believe adidas shares at current prices represent excellent value, with a very favorable risk-reward ratio, even amid high uncertainty today. I am quite confident.

At €214 per share right now, adidas is still a good buy.

Thanks for the article. I'm wondering how you arrive at such strong earnings growth over the next few years when revenue growth appears to be significantly lower. What exactly is expected to lift margins that much? Yeah Market Share gains, operative efficiency and pricing power can lead to better margins, but these earning forecast seem to be very optimistic, dont you think so?

Could you clarify what operational or structural changes you are expecting to drive that margin expansion in more detail?

Great post. I'd sort of forgotten about them. Thanks for the reminder.