ASML Holding N.V. – Current fear-driven weakness is a gift to investors

In this post, I will cover the ASML Q4 earnings and its most recent investor day, updating the investment thesis.

Looking to do your own stock analysis? Consider using StocksGuide, my go-to stock and business analysis tool. Check it out! Most of its features are free.

Surprise! (not) ASML is still a top-notch business with a brilliant outlook, and all this recent share price pressure is entirely unwarranted.

ASML really silenced the critics and took away all investor concerns last Wednesday with its Q4 earnings report and guidance, which was an absolute home run on all fronts.

The company’s Q4 earnings, order numbers, and outlook for Q1 and FY25 blew past the consensus. Furthermore, the company remains extremely optimistic about its outlook through 2030, thanks to its massive moat, monopoly, and the upcoming upcycle in the semiconductor industry driven by the rise of AI.

Finally, as a cherry on top, management isn’t at all worried about a potential impact from Deepseek. In fact, it believes it will positively impact its business, making the 13% sell-off earlier this week completely unnecessary.

Yet, despite all this, ASML shares gained only a meager 5% during Wednesday’s trading session, giving up some of the earlier gains that day (+10%). Investors remain cautious about these AI-driven names after the Deepseek scare and subsequent uncertainty over the AI growth trajectory, offering up great opportunities for us retail investors.

The result? ASML’s massively impressive Q4 and guidance are nowhere near priced in. Despite all this good news, ASML shares ended the week flat, even though management claims Deepseek won’t negatively impact them.

In simple terms, lower AI costs mean higher AI usage, which means higher demand for chips, which means higher demand for ASML equipment, thanks to the expansion of production capacity.

As a result, despite the company remaining one of the best businesses you’ll find for the next decade, its shares are down 11% over the last twelve months, and you can still pick up shares at bargain prices, which we have only seen a handful of times over the last five or so years.

I mean, picking up shares in such a pristine business with a powerful moat and monopoly position, a mighty outlook pointing to at least high-teens EPS growth, and probably well into the next decade at just a 28x earnings multiple is an opportunity I am not passing on.

In this article, I will explain why ASML remains a top buy at current prices. I will also discuss the Q4 numbers, details, and management commentary, as well as the details and insights from ASML’s recent investor day.

Let’s delve in!

Not familiar with ASML? Here is a quick explanation

For those who are new here and don’t know, ASML is one of my largest positions at roughly 9% of my portfolio, behind only Uber Technologies, and one of my highest conviction long-term picks.

The reason is simple: ASML is one of the best-positioned companies for the decade ahead, thanks to its crucial position in the rapidly growing semiconductor industry, impenetrable moat, and monopoly.

For those unfamiliar with the company, let me give you a quick explanation.

ASML Holding N.V. is a Dutch company focused on building the most advanced chip manufacturing equipment, EUV Lithography equipment. These machines are the only ones capable of creating the most advanced chips used in all our advanced technologies today, such as smartphones and data centers, including AI.

Crucially, ASML is the only company capable of producing extreme ultraviolet (EUV) lithography machines, meaning the company operates a pure monopoly with no competition. Indeed, without ASML, we wouldn’t be talking about AI right now.

ASML’s monopoly in EUV technology is a result of decades of research, engineering breakthroughs, and strategic partnerships with key players in the semiconductor industry. EUV lithography allows chipmakers to etch circuits at an extraordinarily small scale, enabling the continuation of Moore’s Law by packing more transistors onto a single chip.

The company’s EUV machines, which cost upwards of $200 million each, are crucial to the most advanced chip manufacturers, including TSMC, Samsung, and Intel. Given the complexity of EUV technology, which involves high-powered lasers, nanometer-scale precision, and highly specialized components sourced from a network of global suppliers, no competitor has been able to replicate ASML’s capabilities or even come close.

Indeed, the company operates a monopoly and has an impenetrable technological moat. Demand for advanced semiconductors is expected to grow rapidly well into the next decade, and so is demand for ASML’s equipment. Its customers are eager to expand its advanced node capacity to keep up with this demand.

In other words, ASML has a brilliant outlook and, despite its long history, a long runway of growth ahead of it.

On that note, let’s delve into the Q4 earnings report!

ASML delivers a sublime quarter

ASML released its earnings last Wednesday, pre-market, and immediately impressed with its initial headline numbers, which were well ahead of consensus estimates. Demand for the company’s equipment from Western customers is finally picking up again.

As a result, ASML delivered record-high quarterly revenue of €9.3 billion, ahead of the high end of its own guidance and €300 million above the Wall Street consensus, a solid 3% beat.

Furthermore, this represents 29% YoY growth, an impressive top-line acceleration from 12% growth last quarter and a negative 21% at the very start of the year. Again, this shows that ASML finally sees near-term headwinds disappear. Issues at key customers Intel and Samsung regarding fab completions are easing, and demand for its machines is picking up as the semiconductor industry finally returns to growth after a cyclical dip. This translates into higher Capex budgets for ASML customers and, subsequently, growth for ASML.

This performance was helped by two more shipments of the company’s latest and most advanced high-NA systems, which have higher margins and higher prices, helping top-line growth. This resulted in system sales of €7.1 billion, consisting of €2.9 billion in EUV sales and €4.2 billion from non-EUV sales.

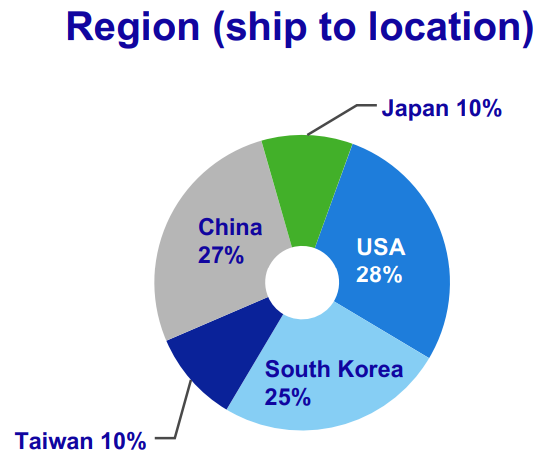

Crucially, the regional revenue split shows that revenue derived from China has been normalizing rapidly, as expected. It declined from 47% in Q3 to just 27% in Q4, consisting of only non-EUV revenue, as ASML isn’t allowed to ship EUV equipment to China.

Positively, revenue lost from China due to restrictions was easily offset by other regions, with the USA and South Korea, in particular, growing from previous quarters. This lower China dependence is great when it comes to risks and exposure to more restrictions. This number is expected to decline further in 2026 after being very elevated in 2024 due to ASML rushing through its Chinese order backlog ahead of restrictions.

Meanwhile, the biggest contributor to last quarter’s outperformance was the company’s Installed Base segment, better known as its service revenues. These grew roughly 35% year over year to €2.1 billion, well ahead of management and Wall Street's expectations. The growth was helped by a growing installed base but mostly by customer upgrades.

For reference, these service revenues are recurring and most often based on multi-year contracts, making them highly reliable. The average ASML machine has a lifespan of up to 20 years, meaning that every machine sold by ASML earns not only the initial selling price but also decades of recurring service revenues, which is pretty brilliant. Therefore, the fact that this is growing this quickly is a positive! I am pleased with this development.

For the full year, ASML delivered total sales of €28.3 billion, which is also ahead of expectations and reflects a 3% year-over-year increase, whereas none was expected. This consists of 44 shipped EUV systems amounting to €8.3 billion, down 9% YoY. This decline was somewhat offset by a 4% growth in DUV system revenue at €12.8 billion.

However, this still left system sales revenue down year over year, offset by 16% growth in service revenues (thanks to their recurring nature, which is not impacted by cyclical pressures). These revenues now total €6.5 billion and account for 23% of revenue.

So far, so good.

Yet, the real highlight of the earnings report is yet to be mentioned—the impressive order intake.

ASML reported a net order intake of an impressive €7.1 billion, comprised of €3 billion in EUV orders and another €4.1 billion in non-EUV orders. This sits far ahead of the Wall Street consensus of €4 billion and brings ASML’s backlog to €36 billion, meaning the company has now fully secured the high-end of its 2025 revenue guidance in existing orders. Pretty sweet.

However, I don’t get too optimistic about these numbers, as they have proven quite lumpy from quarter to quarter in the past. For this reason, ASML will not report these numbers after 2025 and will only report its backlog from then on.

Nevertheless, it is great to see ASML log this many orders, at least showing that demand is improving. Last week, we already noted that TSMC meaningfully raised its FY25 Capex to 19% above expectations, and ASML is one of the companies benefiting from this, with even more orders likely to come in during the year.

The 2025 backdrop for ASML certainly isn’t too bad.

On that note, let’s move to the bottom-line performance, which also beat expectations. ASML reported a Q4 gross margin of 51.7%, well ahead of its 49% to 50% guidance, driven by lower-than-expected costs from high-NA system installations and better-than-expected service revenues, which carry higher margins.

This resulted in a better-than-expected gross margin, up 90 bps from last quarter and 30 bps YoY.

Moving further down the line, R&D expenses aligned with guidance, while SG&A was slightly higher. This resulted in a net income of €2.7 billion, reflecting a net income margin of 29.1%, 50 bps above what I expected, and translating into an EPS of €6.85.

For the full year, this resulted in a net income of €7.6 billion at a net income margin of 26.8%, 20 bps above expectation, and an EPS of €19.25, beating my estimates by €0.20. Also, the company delivered an FY24 FCF of €9.1 billion after a really good Q4, reflecting a very healthy 32% FCF margin.

This also fully covered additional financial obligations, with shareholder returns amounting to €3 billion in 2024. For reference, ASML shares now yield 0.9%, with a 36% payout ratio and a 5-year growth CAGR of 24% (raised for 10 consecutive years).

This also allowed ASML to strengthen its balance sheet considerably. The company ended the year with €12.7 billion in cash and a total debt of only €3.5 billion, leaving it in a very healthy financial position.

Absolutely nothing to complain about here.

Before we move on, just a quick word…

Rijnberk InvestInsights is a reader-supported publication. I try to keep most of my content free for everyone, but I can’t do this without your support!

So please subscribe if you like our content! Want to receive even more of our investment insights and show even more appreciation? Please consider upgrading to our paid tier (only $7.50 monthly or just $70 annually).

In addition to all the free stuff, this also gets you access to even more premium analyses (a total of 3 per month), full access to my own (outperforming) portfolio, immediate trade alerts in the subscriber chat, and a full overview of all my price targets and rating, and even more!

Outlook & Valuation (Investor day guidance)

That brings us to the outlook, which is likely the most important portion of this post. It tells us all about potential returns and whether ASML is a compelling investment.

Though, I can already tell you… it is.

As made clear during its investor day a few months ago, few businesses are better positioned long-term than ASML.

For starters, the semiconductor industry as a whole still maintains a very promising outlook. As management said during the investor day, “Given the role of semiconductors as mission-critical enablers of multiple megatrends across society, the industry’s growth remains promising.”

ASML still estimates the industry will be worth over $1 trillion by 2030, pointing to growth of at least 9% through the end of the decade, which is a great backdrop for ASML itself. Growing demand for semiconductors is expected to lead to significant production capacity expansion at ASML customers, requiring more equipment.

Meanwhile, thanks to its close relationships with businesses across the semiconductor industry, including the largest fabs, equipment peers, and component suppliers, ASML generally has a good view of the industry's forward growth and underlying trends, making its projections quite reliable.

Adding to this already positive backdrop are the technological challenges associated with AI, which include high costs (depending on the Deepseek innovation) and, more importantly, high energy consumption. Energy consumption is currently creating a ceiling on training capability.

The way to solve this? More advanced chip technology, which allows for reduced energy usage and lower prices. Enabling these more advanced chips? Indeed, ASML’s EUV technology is expected to see a significant bump in demand in the years ahead for these exact reasons. According to ASML, EUV innovation should allow for energy usage to drop by 80% in 15 years, with room for even more innovation beyond that.

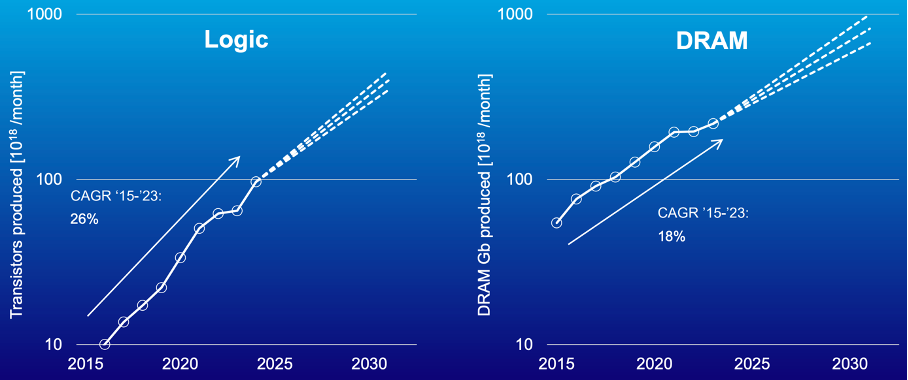

These factors drive up growth expectations for EUV sales in the remainder of the decade, simply because demand for advanced chips is expected to grow rapidly and growth as a percentage of total production. Currently, ASML estimates that EUV spending will grow at a 12-22% CAGR through 2030, which is significant and a great outlook for the company.

Meanwhile, DUV is also expected to continue growing steadily at a high-teens percentage across all markets. For what it is worth, ASML also dominates this market, accounting for 92% of added capacity over the last four years.

Finally, installed base revenues should also continue to compound as ASML brings more machines online worldwide. According to management, these revenues should grow at a 13% CAGR through 2030, reaching an annual revenue of €11-13 billion.

Ultimately, this all paints an incredibly compelling long-term outlook. The story remains the same as it has been for years: ASML has a great growth outlook driven by secular drivers in the underlying markets. With its dominance and monopoly position in both EUV and DUV technologies, it is poised to benefit massively.

So, to rank up all the numbers, let’s start with the short-term guidance.

Management now guides for Q1 revenue of between €7.5 billion euros and €8.0 billion, well ahead of a €7.1 billion consensus. Furthermore, management anticipates a gross margin of between 52% and 53%, which is a solid improvement sequentially and YoY, thanks to High NA revenue realization.

For the full year, management leaves its guidance unchanged. It points to FY25 revenue between €30 billion and €35 billion with a gross margin between 51% and 53%, which is pretty good but also feels a bit conservative.

This wide range is explained by the uncertainty surrounding AI demand and its effect on ASML customers. If current trends hold up, management anticipates revenue should be at the high end of the range. However, if capacity additions at Intel and Samsung remain slow, this could pressure revenue, even with a backlog of €36 billion.

Still, I think management is being conservative, as is the current Wall Street consensus pointing to revenue of only €32.1 billion.

Furthermore, management also reaffirmed its 2030 guidance, pointing to revenue of between €44 billion and €60 billion, with a gross margin of between 56% and 60%, pointing to significant upside through the end of the decade.

All things considered, here are my updated financial projections.

Moving to the valuation part, there is even more to like. As I said before, last week’s positives are nowhere near priced in yet. ASML shares are flat for the week and trading at around €720 per share. After last week's Deepseek upset, this presents investors with an excellent opportunity to pick up some shares at a discount. The recovery after the home run Q4 results did not even offset these losses, even as ASML management explained that any concerns are invalid.

As a result, shares still trade at just 28x my FY25 earnings estimate, a 27% discount to the 5-year average multiple and only a 13% premium to the sector median. Furthermore, this translates into a PEG of only 1.2, which is a 33% discount to the sector median, even though ASML truly is one of the highest-quality and lowest-risk businesses in the semiconductor sector, with a significant runway of growth ahead and a massive and impenetrable moat, suggesting growth is, indeed, not priced in.

I mean, picking up shares in such a pristine business with a powerful moat and monopoly position, a mighty outlook pointing to at least high-teens EPS growth, and probably well into the next decade at just a 28x earnings multiple is an opportunity I am not passing on.

For reference, using various valuation models and methods and cautious estimates, I have come up with a conservative end-of-2027 target price of €1050 per share, reflecting potential annual returns (CAGR) of 15%, including dividends. This is plenty to beat global benchmarks at a great risk-reward balance.

Therefore, at these prices, I am a happy buyer of ASML shares. At any price below €780 per share, based on current estimates, I believe ASML shares are worth buying. This company still has a very bright future and fundamentally remains one of the best businesses in the world.

Current fear-driven weakness is a gift to investors.

We also made a deep dive into this incredible company! :)

Clear write up! Thanks! This is one of rare companies that can provide guidance for the next 10 years (maybe the only one?). That already says quality!