ASML Holding N.V. – Here is my take after the Q3 earnings and a 20%+ sell-off

Looking through near-term headwinds and skepticism to reap the long-term rewards has never been more important.

There is no way around it: Certain parts of ASML’s Q3 earnings report and guidance released last week were massively disappointing.

Most importantly, 2025 guidance and the Q3 order intake came in well short of expectations, resulting in a negative reset of near-term financial projections as, clearly, the recovery of the semiconductor industry and a return of demand for ASML equipment is more gradual than expected and the impact of Chinese export restrictions will be felt.

This most certainly was quite a negative surprise for investors, and considering the negative sales reset required for 2025, the sell-off that occurred last week is understandable, although also massively overdone.

After an 11% sell-off following the Q2 results in June, this time out, in response to the poor Q3 earnings report, ASML shares have shed around 20% of their value, losing some €50 billion in market value. Last Tuesday’s 16% sell-off marked the largest single-day drop for ASML shares in multiple decades.

Meanwhile, while everyone enters panic mode and ASML shares sell-off, hitting a 2024 low, I would argue now is the perfect time to aggressively pick up ASML shares. I can tell you I have done so, growing my number of shares by over 25% this week alone.

While the order intake and management’s 2025 guidance definitely disappoint and require me to lower my 2025 estimates, in terms of fundamentals and long-term prospects, nothing has really changed here. ASML remains poised for impressive growth through the end of the decade and remains a prime beneficiary of the next upcycle in the semiconductor industry with its EUV monopoly.

The fact that the industry and demand recovery (after a shallow cyclical dip in recent quarters) will be more gradual and pushed out into 2026 and 2027 doesn’t hurt the long-term thesis at all. Revenue will not be lost but rather pushed out.

You see, looking at the numbers alone doesn’t tell you the whole story—not even close. It is crucial to consider the underlying narrative and put the results and guidance into perspective, taking into consideration industry dynamics. You’ll quickly see that investors have nothing to worry about fundamentally and long-term, and, crucially, current disappointing numbers can be explained by temporary outside factors.

While in the near term, everything might look a bit grim, in the long term, there is still a lot to like here, and ASML remains one of the best investments out there, in my opinion.

Looking through near-term headwinds and skepticism to reap the long-term rewards has never been more important.

In the end, the semiconductor industry, in part thanks to secular growth drivers like the rise of AI, electrification, digitalization, and edge computing, will continue to keep compounding at a double-digit rate well into the next decade, with Fortune Business Insights pointing to a 15% CAGR.

With semiconductor demand growing this quickly, significant global expansion of manufacturing capacity is nearly certain. Thanks to its EUV monopoly, ASML is a key enabler of next-gen semiconductor technology. Without it, there would simply be no next-gen technologies like AI or data centers. It is the most obvious beneficiary here and bound for significant growth well into the next decade.

And for those wondering, don’t worry; its moat won’t be broken anytime soon, thanks to the insane complexity of the machines and the decades of headstart in research and development ASML has over any competition. Its technology is unequaled. In the words of Chris Miller, assistant professor at the Fletcher School at Tufts University:

“The machines that they produce, each one of them is among the most complicated devices ever made.”

Furthermore, it has an insanely complex and unequaled supply chain, which is impossible to replicate. Just consider the following:

“Each of these machines costs up to €300 million and consists of thousands of components derived from nearly 800 specialized suppliers, some of which ASML owns or has a minority position in to gain greater control of its supply chain and ensure it.

ASML manufactures the different modules in 60 different locations and then ships these to Veldhoven for assembly and testing. After that, it disassembles the device again and uses a whopping 20 trucks and three fully loaded Boeing 747s to ship a single device to the customer.”

Indeed, its long-term outlook is sublime, even as it faces near-term headwinds. As a result, last week’s sell-off is nothing short of an opportunity to pick up shares in one of the world’s most pristine businesses at a considerable discount.

Let me take you through the Q3 results, the company’s fundamentals and potential, and valuation, put management’s guidance into perspective, and update my medium-term estimates.

Let’s dive in!

The actual Q3 results were mostly perfect!

Looking at the Q3 results, one thing that stands out right away is that the actual numbers aren’t even that bad. In fact, Q3 revenue came in above the high end of management’s guidance and Wall Street estimates, which was surprisingly strong, even as ASML has a track record of over-delivering.

ASML reported net sales/revenue of €7.5 billion, up 12% YoY and showing a clear demand and growth improvement from previous quarters, as expected, though better than anticipated.

Last quarter's outperformance was driven by strong DUV demand and higher-than-expected installed base management revenues, which are basically service revenues derived from maintaining the installed base.

As a result, growth turned positive rather quickly again after a couple of quarters of negative growth amid lackluster demand and short-term delays in fab completion in response to a cyclical downturn in the semiconductor industry. In simple terms, ASML had seen slow demand for its equipment and deliveries being pushed out due to cyclical headwinds, which are now slowly easing, as shown by accelerating top-line growth in line with expectations.

Moving to the bottom line, the gross margin in Q3 was 50.8%, sitting at the high end of management’s guided range. Again, it is a pretty decent performance, even though it reflects a 110 bps YoY decline. Positively, the margin decline can be explained by still some top-line weakness and rapidly growing costs as ASML is aggressively investing in its supply chain and manufacturing capacity to fully benefit from the expected upcycle in the years ahead.

Therefore, this shouldn’t be any sort of concern.

Moving further down the line, the operating margin came in at 32.7%, flat YoY. Net income was €2.1 billion last quarter, up 10.5% YoY. This shows that bottom-line growth was slightly less impressive than top-line growth, again due to expenses still outgrowing top-line growth for the time being. Positively, a 27.8% net income margin was solid, and although down 60 bps YoY, it did come in roughly in line with my expectations and that of Wall Street.

As a result, EPS grew 10% YoY to €5.28, exceeding my own estimates. Again, most of the Q3 numbers were ahead of expectations and quite impressive, only to be overshadowed by other factors.

I think you can start to see why the 20%(!) sell-off was rather ridiculous.

Finally, regarding the bottom line performance, ASML reported Q3 FCF of €534 million, down 14% YoY. Once again, the drop in FCF can be easily explained as the disappointing order intake led to lower down payments and cash flows, while ASML kept up manufacturing.

You see, whenever a customer orders a DUV or an EUV machine, a down payment is made which ASML realizes as a pre-payment cash flow. However, with these orders down, it misses quite a bit of these cash flows, impacting FCF so far this year.

Meanwhile, ASML is not slowing manufacturing, which has translated into higher inventories as deliveries are postponed and demand is down, again impacting FCF.

Once demand returns and growth accelerates, these inventories should trend down quickly, with normalized demand still outpacing ASML’s manufacturing capacity. As a result, FCF should also improve rapidly once the top line does and the order intake improves again.

Positively, ASML does maintain a healthy balance sheet with €5 billion in cash and €4.7 billion in debt. It receives an A+ credit rating from Fitch and has absolutely no trouble covering its 1% dividend yield, which management intends to keep growing strongly in the years ahead.

Ultimately, ASML’s business and performance are healthy and above expectations – simple as that.

Before we move on, just a quick word…

Rijnberk InvestInsights is a reader-supported publication. We appreciate you being here! Want to support our work a little bit more and show your appreciation? Consider upgrading to paid (only $5 monthly).

This allows me to push out even more content and gets you premium access to even more content, including my full insight into my personal portfolio!

The big Q3 disappointment: The order intake

However, that also brings me to the big disappointment, which is the order intake. Whereas most expected ASML to once again report a solid order intake as demand was expected to improve dramatically, in reality, ASML saw its order intake weaken considerably from the previous quarter as demand simply wasn’t as big as expected, and the recovery will be more gradual.

ASML only managed to report net bookings of €2.6 billion, which is well short of the €5.6 billion anticipated by Wall Street analysts and reported by the company in Q2.

Obviously, this is quite poor and a very clear indication that demand for its equipment isn’t improving as rapidly as hoped/expected.

However, the poor order intake isn’t a complete disaster, despite everyone making it seem like such. As I have done in previous quarters, I would argue this isn’t a reason to panic at all, mainly because the poor bookings can be easily explained and are simply the result of outside factors and industry cyclicality to which ASML isn’t entirely immune. The graph below shows that even ASML, throughout its history, has always been exposed to the industry’s cyclicality, as has its order intake.

Don’t get me wrong: the order intake last quarter was pretty disappointing, no doubt about it. However, understanding the underlying dynamics here, there is no reason for a sell-off.

Most importantly, it’s not like these orders ASML has missed out on have gone lost. These are simply postponed and pushed out into future quarters as large customers like Intel and Samsung, which aren’t benefiting from the AI boom as much as TSMC, are showing cautious buying behavior.

For example, Reuters reported yesterday that Samsung has postponed taking deliveries of ASML's chipmaking machines, including high-end EUV equipment, for its upcoming facility in Texas as it has yet to get any major customers for the project. In other words, for Samsung, the current demand environment doesn’t justify these investments, and with ASML only realizing revenue after delivery, you can see what is happening here.

Meanwhile, ASML and the industry as a whole continue to see strong demand for AI and the semiconductors enabling it. In other market segments, like personal electronics and automotive, a recovery is turning out to be less aggressive and more gradual, translating into some customer caution for ASML, as visible in the order intake. ASML customers are simply not yet prepared to invest more heavily in fab expansion or new technologies as long as semiconductor demand remains somewhat lackluster.

For ASML, this translates into a lower current order intake as orders are pushed out and equipment deliveries are delayed. However, crucially, this revenue and these orders haven’t gone lost but will be realized at a later date, so the long-term thesis isn’t hurt at all. Yes, FY25 estimates will have to go down due to prolonged weakness, but this will drive up FY26 and FY27 estimates, meaning not that much changes for long-term investors.

Oh, yes, we should also remember that ASML still has a current backlog of over €36 billion, or roughly 1.2x annual earnings. While it might not be able to realize this revenue today due to fab construction delays, most of this backlog is non-cancellable due to down payments, so it will be realized once demand returns.

Finally, the long-term growth drivers for ASML remain in place. This is what management said during the earnings call:

“The secular growth drivers are clear, and they are strong. I think if you look at AI, very, very strong, very clear and undisputed. Taking an increasing share in the business of our customers. So I think that is going very strongly. Also, if you look at energy transition, electrification, et cetera, those secular trends are very, very much intact. It expands the application space for both advanced and mature nodes. That also means that we will continue to prepare for new fab openings that are planned by customers. And yes, there might be some delays here and there. But still, if you look at the planned fab openings in the next couple of years, it is pretty significant, and as you know, it really is across the globe.”

Outlook & Valuation

Even though the order intake was poor, the biggest negative in the ASML press release last week was management’s 2025 guidance, which indicated revenue would come in at the lower end of the guided range due to prolonged weakness and a more gradual recovery.

Starting with the Q4 guidance, ASML guides for further growth acceleration, pointing to YoY growth of 25% at the midpoint of the guided range of €8.8 billion to €9.2 billion. Notably, this is well ahead of my earlier expectations and those of Wall Street, as ASML is, in fact, still seeing a clear uptick in demand, which is reason for optimism.

In fact, based on this guidance, FY24 revenue should come in around €28 billion, which is some €700 million above my prior projections and easily ahead of the Wall Street consensus. So, from this perspective, ASML is performing really well, doing everything right and outperforming.

As for the bottom line guidance, ASML now points to a gross margin expectation of 49-50%, which is still down quite a bit from previous quarters and down at least 140 bps compared to Q4 last year.

Positively, this drawdown can be explained by the realization of revenue from two High NA systems, which has a 350 bps negative impact on the gross margin, so adjusting for that, the gross margin would be up some 150 bps YoY, reflecting some margin gains coming from an accelerating top line and a higher portion of revenue coming from higher margin service revenues.

However, this is where the good news ends. While the recovery is visible and so far ahead of expectations, the problem here is that ASML management, at the same time, indicates that the demand recovery going forward is looking less steep and more gradual than previously anticipated, which urges some more conservatism for 2025, with this demand being pushed forward to 2026 and 2027, most likely.

In other words, the big jump in demand and revenue growth expected for 2025 will be less pronounced, with a piece of this coming in the years after. Driven by all the factors discussed so far, ASML now guides for revenue of between €30 billion and €35 billion compared to €30-40 billion previously.

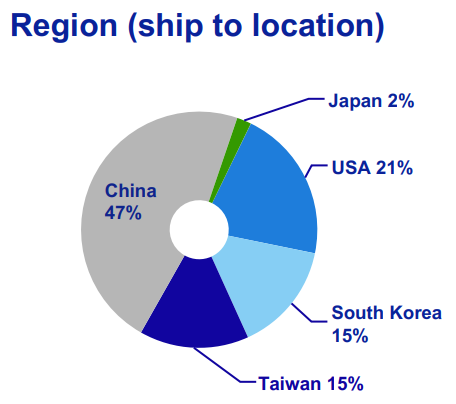

This also includes the expectation that China’s share of ASML revenue will trend down to historically normal percentages after a few quarters of elevated levels, as Chinese customers were massively ordering ASML equipment ahead of the latest export restrictions imposed by the U.S. and Dutch governments. However, this pulled-forward demand is now dropping rapidly, in part due to these new restrictions, potentially resulting in a 30% drop in Chinese revenues in 2025, according to UBS analysts.

As a result, whereas China accounted for a percentage of 40-50% of ASML revenue in recent quarters, this should drop back to around 20% in 2025 and is expected to remain around the 20% mark. Obviously, this, in combination with continued weakness in other regions, is pressuring demand and near-term results.

ASML has also been tempering expectations regarding the 2025 margins. Whereas it previously guided for a gross margin of 54-56%, this has now been revised lower to 51-53%, mainly due to fewer EUV deliveries expected and fewer high-margin revenues coming from China.

Finally, OpEx, comprised of R&D and SG&A costs, is expected to come in at the upper end of the earlier discussed bandwidth at €6.1 billion for 2025, representing a YoY increase of 13%.

Ultimately, the near-term outlook is mixed. On the one hand, recent results and guidance allowed me to meaningfully revise my FY24 estimates positively. I now expect revenue growth to remain positive and the EPS decline to be more shallow.

However, with the recovery less steep, I have had to significantly lower my FY25 estimates on both top and bottom lines, similar to Wall Street estimates.

As a result, I now expect the following financial results in the medium term.

Following the guidance cut and lowered expectations, Wall Street has been collectively cutting its price targets, and rightfully so. In the end, short—to medium-term estimates have come down.

However, even when considering this, last week’s 20% sell-off is nowhere near justified and massively overdone. Now, shares have bounced back a bit in recent trading days, taking back some 5% from last week’s bottom, but these still trade at just 25.5x next year’s earnings, which for ASML standards is not too expensive and quite a bit lower compared to the 28.5x these traded on back in June

Furthermore, better considering forward growth, shares trade at a PEG of just 1.5x, which is a discount of roughly 19% to its own 5-year average and that of the semiconductor sector, even though ASML is one of the most sublime businesses out there, operating a pristine monopoly.

In the end, ASML’s long-term outlook and thesis remain very much intact, and for long-term investors, nothing has really changed with these latest results, as clearly laid out. In fact, across most metrics, the company is performing really well and navigating cyclical headwinds pretty well, in my opinion.

As a result, last week’s massive sell-off is nothing short of a perfect opportunity to pick up shares at a rare discount, and I am actively doing so! I have grown my number of ASML shares by over 25% this last week alone at prices below €630 per share.

Ignore the short-term noise and focus on the long-term story in order to find real value.

At a share price of €665 today, I continue to view shares as very attractively priced, with good downside protection and a high probability of outperformance based on conservative estimates. Below €700 per share, I am happy to keep adding to my position.

My updated end-of-2026 conservative target price = €902

Potential returns from today’s price of €722 = 14.5% annually or 15.5% inc. dividends (CAGR)

Looking to do your own stock analysis? Consider using StocksGuide, my go-to stock and business analysis tool. Check it out! Many of its features are free. (Note: this is an affiliate link)

If you enjoyed this format and would like to see similar posts in the future, please hit the like button, share your comments, and be sure to subscribe.

Thanks, sounds really interesting. Any idea of catalysts coming up. Can certainly sew how it recovers from lows, but is it all eyes on samsung, etc capex as the next clue?

Completely agree with you, I picked up shares as well! Great post! 👌