Booking Holdings Inc. – Now a terrific dividend growth investment

Booking is one of our favorite stocks and has been so for years. The company is consistently underestimated by the market and remains an excellent growth stock and industry leader.

Booking Holdings BKNG 0.00%↑ has been performing exceptionally well since the COVID-19 crisis, during which its revenue and earnings took a significant hit. Thanks to a remarkable recovery, financials have quickly reached new highs.

In fact, the COVID-19 pandemic didn’t hurt the company a single bit. Looking at its 2023 numbers and fundamental developments, the company today is a meaningfully larger and faster-growing business compared to 2019.

Arguably, Booking nowadays is a stronger and better-positioned company than ever before, and this was highlighted in its Q4/FY23 earnings report and call, as the company delivered another exceptional year in terms of financials, outperforming each and every one of its peers, despite its larger size and industry-leading position. This even allowed it to introduce a dividend alongside its terrific share buyback program, bringing investor returns to the next level.

Therefore, now is an excellent time to take a closer look at the company. Booking has long been, and in our view remains, an underappreciated stock on Wall Street. The company consistently trades at an undeserved discount, which does not reflect its leading market position and impressive growth outlook. The undervaluation compared to much-(over)hyped Airbnb says a lot.

Meanwhile, the company's revenues have grown at an impressive 12% CAGR over the last decade, which is even more remarkable considering it had to withstand the COVID-19 crisis and has grown earnings at an even faster pace. We have had Booking in our portfolio for quite a while already, resulting in terrific returns. Shares are up close to 40% over the last year, close to 100% over five years, and closer to 200% over the last decade, consistently outperforming the S&P 500.

We believe it is about time the company gets the recognition it deserves, and its recent financials and the introduction of a dividend could get it a long way. In our view, the brilliant capital allocation strategy, combined with an exceptional growth outlook, makes Booking one of the most exciting investment opportunities in the market today, even after shares rallied 40% over the last 12 months. And yet, shares still trade quite cheaply as investors keep underestimating this industry leader.

What is Booking Holdings?

Let’s start by quickly introducing the company for those unfamiliar with it, although I highly doubt there are many. Booking Holdings is a leading global online travel company offering an extensive array of services that cater to travelers' diverse needs and preferences worldwide.

Through its diverse portfolio of brands, including flagship platforms like Booking.com, Priceline, Agoda, Rentalcars.com, and OpenTable, it caters to distinct facets of the travel journey. From accommodations and flights to car rentals and restaurant reservations, Booking Holdings provides convenient solutions for travelers worldwide.

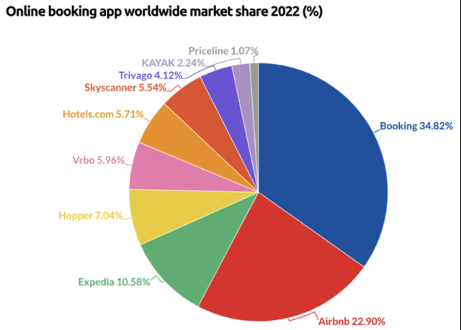

The company holds a demanding leadership position in the global online travel market through this exquisite collection of travel brands and platforms. As the graph below shows, it is significantly larger than its closest peers in terms of revenue and gross bookings.

When combining all its platforms, the company holds a demanding global market share of around 40% in the online travel market, far ahead of its closest peers - Airbnb and Expedia.

Yet, despite its incredible market share, which has grown steadily in recent years, many still believe the company has a weak moat due to its platform's limited differentiation from alternatives like Expedia. This opens it up to disruption, particularly from Airbnb, which has been a massive grower in recent years.

For many years now, this perception of a weak moat has been the leading factor in a discounted valuation, and unrightfully so. Yes, we can see where these fears are coming from. The industry is highly competitive, and many platforms offer similar services, making it hard to stand out.

From a top-down view, many believe that Google or Microsoft could easily penetrate this market if they actively chose to do so. However, this isn’t quite so.

Just consider that after many years of these fears, which have kept many out of the shares, Booking still is the undisputed leader in the OTA market and is even outgrowing its peers, including Airbnb, in terms of gross bookings, revenue, and trips despite its larger size. Booking has simply continued to gain share during a time when many expected Airbnb to disrupt its business.

Nothing is less true, and the newcomer hasn’t disrupted Booking in any way as its hotel business remains incredibly popular, and even its alternative accommodations business, where it competes much more closely with Airbnb, is flourishing.

Now, there are a number of factors that allow Booking to keep outgrowing competitors and solidify its moat, which is often overlooked or underestimated. For starters, the company can set itself apart by its number of established travel brands, which are trusted by tens of millions of travelers.

Ultimately, the brand name and the trust it has gained over decades are stronger than anything else. I mean, many people still have trouble trusting their Airbnb’s due to several spying incidents and this trust is hard to regain.

On top of this, we should remember that people are lazy and want to book a trip in as few clicks as possible. Positively, Booking’s tech stack is the best one out there, and through the Booking.com platform, travelers can book accommodation, flights, rental cars, and experiences in a few clicks within a single app.

Booking has proven to have an amazing tech stack, which it continues to develop, improving the customer experience and convenience. This leads to impressive customer retention and loyalty. I can speak from personal experience that Booking has never disappointed, and I adore the convenience and overall user experience. As a result, I most often use Booking without checking any other platform. This is the power of trust, brand, and a good prior experience. So yes, this is quite a strong moat.

Finally, we can also add that Booking has the best loyalty/rewards program out there and is able to offer the best prices most often, supported by its long-standing relationships with hotels and other accommodations and chains.

While Airbnb is most often mentioned for its great pricing, I have found that in each of my recent trips in the U.S. and Europe, a similar quality stay is now often cheaper on Booking.com, partially supported by its rapidly growing offering.

Ultimately, I believe we shouldn’t underestimate the hidden moat of this business. While it certainly isn’t as powerful as many others in other industries like Google in search, Microsoft in cloud computing, or Coca-Cola in beverages, Booking has proven that it knows how to retain customers and outgrow peers as a result. I see no reason for this to change going forward, and I expect Booking to keep gaining market share, especially considering the company’s long-term vision and recent developments, which I will highlight later in this post.

But before we get into the recent developments and financial results, it is worth highlighting that the company’s underlying market supports incredible long-term growth as well.

The OTA market and travel outlook support impressive long-term growth for Booking

This strong moat discussed above also makes Booking a prime beneficiary of the growth in the OTA and travel markets. If it continues outperforming peers and taking more market share, we believe Booking is well positioned to outgrow the underlying market.

The company's most important market is the online travel agency (OTA) market, which is projected to grow at an impressive 13% CAGR from 2024 through 2030.

This growth is driven by several factors. The most important ones are the growing middle class and the rising disposable income of consumers worldwide. According to Verified Market Reports, “The number of middle-class households is increasing in many countries all over the world, and with it, disposable incomes are also rising. This has increased the purchasing power of many households and has led to increased demand for travel services, causing a boost to the global OTA market.”

Add to this the rising internet penetration and adoption of mobile devices, and we can safely assume the majority of this market is moving to online solutions and platforms, like those of Booking. According to Verified Market Reports, “The proliferation of the internet and mobile devices over the last couple of decades has allowed for an unprecedented level of access and connectivity to travel services. OTA’s have been able to take advantage of this to make their services more accessible and convenient to travelers, leading to an increase in demand for their services.”

Also worth mentioning is that travel is becoming increasingly popular, especially among younger generations. For reference, a recent survey showed that 65% of Gen Z prioritize experiencing the world over investing in more traditional life moments such as buying a house or saving for a wedding. This is a tremendous long-term growth driver for this industry, including Booking.

Travel experiences came out on top in five out of seven choices for spending priorities, topping material possessions such as clothes and fashion or tech and gadgets, which is unsurprising after COVID-19 and incredibly motivating for the industry.

Considering these factors, a 13% growth CAGR certainly does not seem so far-fetched. Meanwhile, the entire online travel market, to which Booking is also increasingly exposed, is projected to keep growing at a 9% CAGR through 2030. Growth can again be attributed to increasing disposable income but also to shifting consumer behavior (highlighted above for Gen-Z), the growing influence of social media, and a rising inclination toward adventure travel globally. Simply put, the travel industry is a tremendous place to park your money.

Ultimately, Booking's underlying market looks very solid, and we should see decent growth over the remainder of the decade. Of course, we should consider that this is a highly cyclical market sensitive to consumer sentiment, disposable income levels, and economic growth, but still, this looks promising for Booking, regardless of how you look at it.

Booking’s FY23 results were just excellent

Finally, now is the time to look closely at Booking's most recent financial results, which were terrific, even as shares dipped slightly after the results.

The company released the earnings report on February 22 and beat the Q4 consensus on the top and bottom lines, although by a small margin. Room nights booked on the company’s platforms grew by slightly over 9%, driven by strength in Europe and Asia, where nights booked grew by double digits against flat numbers in the U.S. Another driver of growth here was success in alternative accommodations, which saw room night growth of 19% YoY.

This led to gross bookings of $31.7 billion, up 16% YoY and outpacing the 15% and 6% growth reported by Airbnb and Expedia, respectively, in a completely normalized operating environment.

This difference in growth between room night growth and gross bookings resulted from higher accommodation prices and a positive impact from FX and flight bookings, with the latter also growing strong in Q4, reporting a YoY growth of 46%.

This led to revenue of $4.8 billion, up 18% YoY, exceeding expectations and guidance. The revenue take rate came in at 15.1%, which is in line with expectations.

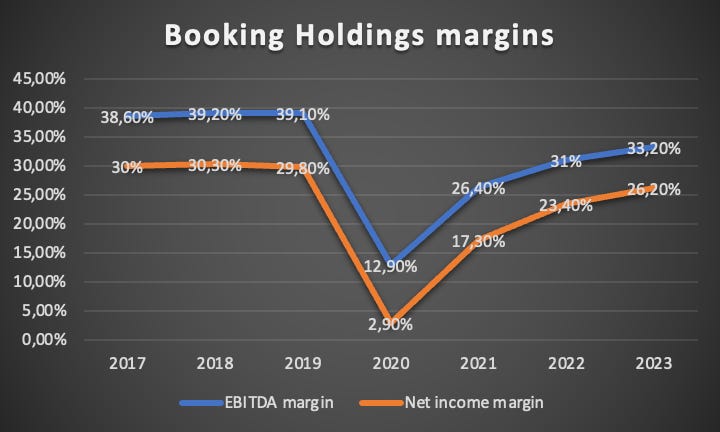

On the bottom line, Q4 was also solid. Marketing expenses, Booking’s largest expense, only grew 9% YoY, far below the top-line growth, driving up margins. EBITDA came in at a quarterly high of $1.5 billion, up 18% YoY and ahead of expectations (up 22% in constant currency). This represented an EBITDA margin of 31.3%, up 200 bps YoY.

This allowed EPS to grow by an impressive 29% YoY to $32. This was also significantly helped by a 9% lower share count than one year ago, thanks to significant share repurchases. Yes, Booking retired 9% of its shares in 12 months.

Moving to the full-year results, we are just as impressed. The company managed to report total room nights booked of a whopping 1 billion, up 17% YoY, reaching new highs. This allowed the company to report gross bookings of $151 billion, up 24% YoY, resulting in record revenue of $21.4 billion, up 25% YoY. This reflects a slight revenue take rate YoY increase from 14.1% to 14.2%.

Again, similar to Q4, marketing expenses grew slower than the top line, which led to marketing and merchandising now accounting for only 5.6% of gross bookings, down 30 bps YoY.

This allowed EBITDA to outgrow revenue and the margin to expand rapidly. Booking reported an adjusted EBITDA margin of 33.2% in 2023, up 220 bps YoY, leading to EBITDA growth of 34% (37% in constant currency) to $7.1 billion.

Finally, EPS was up an impressive 52% YoY or 58% on constant currency to $152, driven by a solid top line, margin expansion, and significant share repurchases.

Across the board, these are just superb numbers reported by Booking with few negatives. The company continues to rapidly grow its top line despite challenging comparable quarters and a somewhat challenging operating environment in which consumers are less willing to spend.

On top of this, it continues to expand its EBITDA margin at a solid clip, and while this is not quite back to 2019 levels, higher revenue allows it to report higher EBITDA dollars. Moreover, this also highlights the company still has plenty of room for margin expansion, fueling the bull case.

Booking is focusing on all the right things

However, not just the incredible financials have impressed us and made Booking one of our top picks. The company is also developing its platform and operations in all the right directions by focusing on customer satisfaction, improving its tech stack, and growing its TAM.

Booking continues to report solid underlying developments in its business that solidify its long-term growth potential and moat. Management focuses on several factors that will allow it to keep growing long-term and strengthen its market position. These include its connected trip vision, the integration of AI technologies into its platforms, the growth of its alternative accommodations offering, and the building of direct relationships with travelers.

The connected trip vision

Management’s main effort to support long-term growth and gain market share in the travel industry is through its connected trip vision. This vision focuses on connecting all the aspects of a trip and the booking process on a single platform, ranging from accommodation and flights to rental cars and experiences.

Over the last few years, management has expanded its offerings on key platforms like Booking.com and has allowed customers to book these new offerings along with their accommodation. By doing this, it is taking advantage of people's lazy nature and desire to book their trips with as few clicks as possible. The company wants to create a platform that allows travelers to arrange every aspect of their trip on a single platform.

Examples of its connected trip vision are its heavy focus on integrating flights into its platform offering, where it has seen great success so far. Air tickets booked have grown by 400% since 2019 and 58% YoY in 2023, mainly through the expansion of the Booking.com platform. Also, the company released Priceline experiences to enable customers to quickly search and book more than 80,000 activities in over 100 countries.

Through these efforts and developments, it wants to improve the user experience by offering a more convenient and inclusive platform, increase loyalty as users are less tempted to use other platforms when Booking has it all and increase the booking frequency as users have more options.

This all makes sense, and as a regular traveler myself, I know that this is precisely what I want from a platform like Booking. I am convinced this strategy will further strengthen Booking’s moat.

Furthermore, besides these benefits, Booking also sees these new product verticals, like experiences and flight tickets, bringing in new customers on its platforms. These customers then use the company's other products, growing its user base. Through this strategy, the company should be able to leverage its user base and brand to expand successfully.

Booking management strongly believes this strategy will further differentiate its offering from the competition. This will lead to improved loyalty, increased direct bookings, and higher booking frequency, eventually leading to market share gains. Really, this is a very solid strategy and one we cheer for.

Alternative accommodations

In addition, the company is still expanding its accommodation offering, adding supply choices for users. It is looking to disrupt Airbnb’s and Expedia’s VRBO business in alternative accommodations and grow its TAM.

Alternative accommodations now account for 33% of Booking.com’s room nights booked as of 2023, which was 3 percentage points higher than the previous year, growing strongly. This has allowed the company to grow total listings to 7.4 million, up 12% YoY. This is another strong growth driver for the company while further strengthening the Booking.com platform.

Building direct relationships with travelers

Another way Booking is looking to strengthen its position in the industry and drive growth is by creating more direct relationships with travelers through a personalized experience and valuable rewards program and by attracting people to its direct channels, like the app.

Why is this app usage important? Simply put, having travelers book through the company’s direct channels avoids exposing them to other options, allows the company more opportunities to engage directly with its users, and can drive higher loyalty and frequency. Once people have downloaded the app, they are more likely to use Booking again and more regularly than on the web. This is why this is a focus area for Booking.

The company has seen direct bookings through its app grow steadily and strongly in recent years, with it now accounting for 49% of nights booked in 2023, up 5 percentage points YoY. Furthermore, in Q4, this percentage even grew to 53%, again around 5 percentage points higher YoY. These excellent numbers show that management’s efforts are working, creating increased retention. In 2023, the booking.com app was once more the most downloaded travel app worldwide.

According to Seaport Research, this strong organic traffic is what makes the company a “clear leader in global online accommodations with particular strength in Europe and Asia.”

Again, the goal is to improve the experience, which leads to increased loyalty and frequency. Another way for management to improve this experience is by leveraging recent AI developments, which it believes can create a more personalized experience. This includes an AI trip planner, which is already live for customers in the U.S. This is what management said regarding this during the Q4 earnings call:

“We see the AI trip planner is getting better answering customers’ inquiries and we are excited to start testing other verticals out of accommodations.”

Besides improving the customer experience, management also believes it can leverage AI to lower service contacts, making the business more efficient, although this is still mostly dreaming out load.

However, ultimately, we are very encouraged by the developments and plans management has in place across the board, ranging from its connected trip vision to the integration of AI technologies. Booking looks exceptionally well positioned to keep gaining market share through these efforts, making us more confident in its growth outlook.

The balance sheet is in excellent shape, allowing it to introduce a dividend

Let's quickly review its financial health before getting into the valuation and outlook. Booking ended the year with a total cash position of $12.1 billion, down slightly from Q3 due to $2.4 billion of repurchases in the quarter, partially offset by $1.3 billion of free cash flow generated in the fourth quarter and $7 billion generated in 2023.

Meanwhile, debt stands at $12.2 billion, which is pretty good and manageable. Overall, the company is in a very healthy financial position and below its previously stated gross leverage target of 2x. Furthermore, management remains committed to lowering this to 1x over time as FCF grows further and share repurchases ease somewhat after 2026.

Meanwhile, during 2023 alone, management returned $10 billion to shareholders through share buybacks, which FCF didn’t cover entirely, but the company could afford it. Management still has $14 billion remaining under its current authorization and remains committed to completing this before the end of 2026. Positively, the introduction of a dividend has not changed these plans.

The company introduced a dividend of $8.75 per share. While this only represents a yield of 0.25%, this is incredibly exciting news. Given its growth potential, it makes Booking one of the most interesting dividend growth stocks available. The current payout ratio is right around 27%, which means it’s well covered and has plenty of room to grow.

Going by its growth outlook, which we lay out below, we believe this dividend should grow by mid-teens for the foreseeable future, which is terrific, especially as it sits beside significant share buybacks. Few companies return as much cash relative to the market cap to shareholders as Booking, further adding to a very compelling investment case.

Outlook & Valuation

So far in 2024, Booking has continued to see resiliency in global leisure travel demand, and looking at the year ahead, Booking is seeing very healthy booking demand. Positively, current bookings for the summer indicate another record year and bookings so far in January are above management’s expectations.

Based on these solid demand trends, management expects Q1 room night growth of 4-6%, with the ongoing war in the Middle East weighing negatively on the business, as well as a strong start in 2023. Still, while this shows a further slowdown in growth, this should still result in gross bookings growth of 5-7% and revenue growth of 11-13% to $4.26 billion at the midpoint, which, considering the 40% growth in Q1 last year, is still great, although helped partially by the Easter shift from Q2 last year to Q1 this year.

This should lead to Q1 EBITDA of between $680 million and $720 million, which is up 19% at the midpoint and reflects a 100 bps increase in the EBITDA margin.

For the full year 2024, management now guides for gross bookings growth of just 7%, including the negative impact from the Middle East. Revenue is expected to grow at a similar rate of around 7% to approximately $22.9 billion, which seems rather conservative but also reflects economic headwinds and a strong prior year.

On the bottom line, management now expects EBITDA to continue outgrowing top-line growth as the EBITDA margin is projected to expand by around 100 bps for FY24, which, based on the top-line projections, should lead to an FY24 EBITDA of around $7.8 billion. However, EPS is projected to grow much faster thanks to continued share repurchases, leading to EPS guidance for growth of over 14%, which is excellent.

Finally, management remains committed to its previously communicated long-term target of growing faster than it did prior to the COVID-19 crisis in a normalized market environment. It points to over 8% growth for its top-line metrics and EPS growth of around 15%, which really is just incredible.

We believe the company should be able to outgrow at least the entire travel industry. Still, being conservative and considering management’s guidance, we will assume revenue growth of 8-11% in the medium term, also leaving some room for economic weakness in upcoming years.

Meanwhile, EPS growth should remain impressive over the next few years as Booking has plenty of margin improvement ahead, even when taking into account lower margin operations like flights growing rapidly. Add to this the continued buybacks and EPS growth of over 15% is very much likely. This results in the following financial projections through 2027.

Based on these estimates, Booking shares now trade at an earnings multiple of just over 20x, which, considering the underestimated strength of this business and its growth outlook, is relatively cheap, in our view.

For perspective, Airbnb, which has a similar growth outlook, is valued at over 30x earnings for both this year and the next fiscal year and trades at a PEG of 2.5, far ahead of Booking’s discounted PEG of 1.12, which is just ridiculous and a 27% discount to the sector median.

In other words, Booking shares are still getting massively discounted and underestimated. Considering everything discussed so far, we are convinced this high-quality business deserves a 22x earnings multiple, at the very least.

Using our FY24 EPS projection and a 22x multiple, we calculate a target price of $3888, leaving an upside of 7.5% this fiscal year. However, if we use a 22x multiple on the FY26 EPS projections, we end up with annual returns of over 14% from current price levels of just over $3600, which should easily beat global benchmarks.

As a result, we continue to view Booking shares as a great investment at current price points, which is why we recently added shares to our existing position and rate shares. “Buy.”

We are very confident in the company’s future, and the recent introduction of a dividend with incredible growth potential only makes these shares more attractive. We are very bullish!

Let us know your thoughts in the comments! Also, please leave a like if this post was of value to you!

Please remember that this is no financial or investment advice and is for educational and informative purposes only. We are simply sharing our views, actions, and opinions, which I hope will be insightful!

Disclosure: I/we do have a beneficial long position in the shares of BKNG, either through stock ownership, options, or other derivatives. This article expresses my own opinions, and we are not receiving any sort of compensation for it.

No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment decisions.

Very solid explainer on a really cool company!