It is safe to say that Broadcom and its shareholders have had a terrific week.

After reporting its fiscal Q4 and FY24 results roughly one week ago, Broadcom shares are up a whopping 22%, after initially gaining as much as 38% in the span of a few days, adding over $200 billion to its market cap and now making it a $1 trillion business.

Yes, you read that correctly. Broadcom is now one of the few companies globally (nine, to be exact) with a market cap above $1 trillion, which is incredible, especially considering it wasn’t even worth half that at the start of 2024.

Indeed, Broadcom shares are now up about 98% YTD, or over $500 billion in market value, and not without reason.

Apart from being one of the highest-quality and best-managed businesses you’ll find, Broadcom has become one of the biggest beneficiaries and key enablers of the AI revolution. With its industry-leading networking semiconductors, Broadcom has positioned itself as a critical player in enabling next-generation AI and supplying essential components to several cloud giants, leading to rapid growth for Broadcom.

In straightforward terms, Broadcom’s best-in-class networking products enable fast and efficient communication within data centers and between Nvidia GPUs, allowing large amounts of data to be processed quickly and accurately. In reality, without these top-performance networking solutions, AI models with billions of parameters would not be able to work.

So, as AI requires more advanced networking solutions to process larger amounts of data faster, and big tech spends hundreds of billions of Capex to grow its computing capacity and speeds to stay ahead of the curve, you can see how this has been benefiting Broadcom and will continue to benefit it well into the future, as AI infrastructure spending is only expected to continue growing exponentially.

Broadcom is benefitting directly from this Capex growth and is doing so today. AI is very much materializing for Broadcom already, and this has helped the company deliver excellent Q4 and fiscal FY24 results over a week ago, beating the already bullish consensus estimates. However, more importantly, it allowed management to issue incredibly bullish AI-related revenue guidance for fiscal FY26, way above what anyone expected, indicating incredible demand and sending investors and analysts into a frenzy.

However, I will also argue that Broadcom is more than just an AI play.

Today, Broadcom is a global powerhouse under the lead of a superstar CEO, Hock Tan, who has transformed a small niche semiconductor business into one of the nine largest businesses globally, with an industry-leading semiconductor unit fully benefitting from the AI revolution and a well-renowned enterprise software unit. Oh, yes, on top of all that, Broadcom is also one of the most impressive cash flow machines, consistently turning 50% of its sales into FCF and now generating almost $20 billion in FCF annually.

Absolutely mind-blowing. This business has much more going for it than just exposure to the AI revolution.

Anyway, that is just the tip of the Broadcom iceberg, and there is much more to discuss. I think it is time to examine this business, its fundamentals, financials, and outlook very closely.

Therefore, in today’s article, I want to introduce you to the business and its operations to give you a good overview before reviewing its financials, recent performance, and growth expectations.

In other words, this is a Broadcom Deep Dive.

Let’s delve right in!

Broadcom, Inc. – A Technology Conglomerate

Broadcom might be one of the most unique companies out there, not only due to its combination of enterprise software and semiconductors but also because the company is a serial acquirer with probably the best track record out there.

You see, whereas the company’s roots date back all the way to 1961, when it was part of Hewlett-Packard Enterprise, the company as we know it today only came into existence in 2005. In that year, private equity firms acquired Agilent's semiconductor operations, and the company became known as Avago Technologies, led by CEO Hock Tan.

Only in 2016 did the company acquire Broadcom Corporation, a major player in communications chips, in a landmark $37 billion deal. The merged entity adopted the Broadcom name to reflect its expanded vision and capabilities. In the years that followed, Hock Tan kept acquiring businesses to strategically grow, mostly focusing on enterprise software to diversify its revenue stream away from the cyclical semiconductor industry. This includes the purchases of Brocade Communications Systems, CA Technologies, Symantec’s enterprise security business, and finally, the mega $64 billion acquisition of enterprise software leader VMware, which about doubled its enterprise software revenue in 2024.

Below, you can find an overview of these acquisitions.

Whereas in most instances, I would call this strategy of using acquisitions to fuel growth a red flag, Broadcom is an exception to the rule.

You see, the most impressive aspect of this strategy and execution is the speed with which Broadcom has acquired businesses across multiple industries and flawlessly integrated them within the Broadcom group, consistently. Over the years, Tan’s ability to identify opportunities, negotiate advantageous terms, and seamlessly integrate acquired businesses in no time has been absolutely ridiculous.

Hock Tan has proved many critics wrong over the years, who doubted his ability to integrate any of these businesses into the Broadcom ecosystem and turn them into cash flow machines. Yet, he did, time after time. This is really as good as a serial acquirer gets.

You see, Broadcom is highly selective in identifying targets, focusing on businesses with predictable cash flows, strong margins, and leading market positions. This rigorous financial discipline ensures that each acquisition is accretive to earnings and delivers substantial returns on investment.

In addition to its strict selection criteria, a key factor in Broadcom's success is its ability to optimize operations and reduce costs after acquiring a company. Broadcom excels at streamlining redundancies and improving cost structures very quickly after acquiring, most often achieving higher margins than the companies had as standalone entities.

Acquisition after acquisition, Broadcom’s cash flows have always excelled, and the time required to optimize its latest acquisition has always been minimal.

As a result of all these moves and their incredible success and integration by Hock Tan & Co., the company now derives 41% of its revenues from enterprise software and 59% from the semiconductor industry. Broadcom has positioned itself not only as a leader in semiconductors for networking, broadband, and wireless communication but also as a key provider of enterprise software and cybersecurity solutions.

For example, the company is by far the top supplier of networking semiconductors today, making it a top beneficiary of the AI boom as demand for those products is growing rapidly, and through VMware, the company now controls almost half of the highly lucrative virtualization platform market, expected to keep compounding at a CAGR of 21%.

Ultimately, this has made Broadcom exactly what its superstar CEO and pro-acquirer, Hock Tan, envisioned: a well-diversified giant, much like a technology conglomerate, with leading market positions in multiple industries, predictable cash flows, and strong margins across the board.

For the record, the company today still remains under the lead of founder Hock Tan (I know he is not the founder, but let’s be honest, he kinda is). Even as the man is in his early 70’s, I sincerely hope we’ll continue enjoying his tremendous leadership and ability to execute for many more years. This is as good as CEOs get – the track record proves it all.

All of this has led to incredible revenue and FCF growth for Broadcom over the last decade. Revenue has grown at a CAGR of 28% (including acquisitions), and FCF at an even more impressive 38% CAGR, hitting a whopping $19 billion in the most recent fiscal year (reflecting a 38% FCF margin, down a bit due to the VMware acquisition)

Furthermore, the company now generates over $50 billion in annual revenue, leads in 26 categories in the semiconductor and enterprise software industry, consistently delivers industry-leading margins, spends over $9 billion on R&D annually, and holds over 21,000 patents.

Subsequently, investors have been reaping the rewards, with Broadcom shares returning a staggering 2400% over the last decade, 670% over the last 5 years, and 99% over the last 12 months, reaching a market cap of over $1 trillion.

Pretty sweet, to say the least.

So, now that we know Broadcom a little better in terms of structure and operations, let’s review its fiscal Q4 and FY24 results to delve into its financials and recent performance!

Broadcom delivers a really good Q4 report

Broadcom released its fiscal Q4 and FY24 results on Thursday, December 12, and managed to report another solid quarter, with headline numbers roughly in line with the consensus as the company continues to report solid growth, expanding margins, and successful integration of VMWare and an impressive ramp up in AI-related revenue.

Ultimately, Broadcom delivered another quarter that excited investors and analysts alike without delivering mind-blowing results.

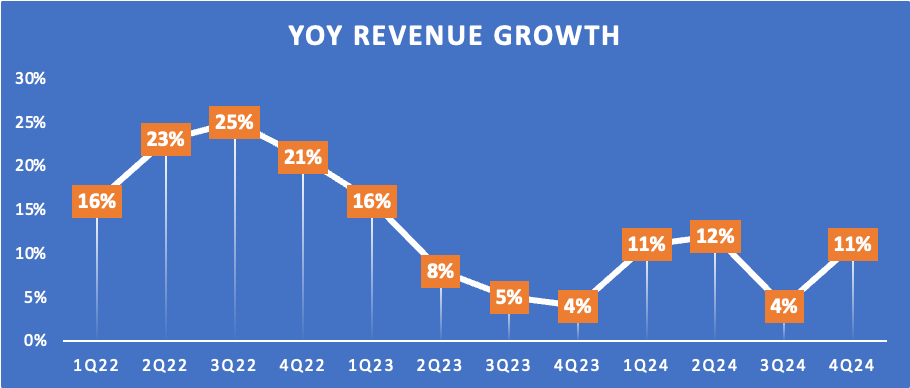

Starting with the top line performance, Broadcom reported net revenue of $14.1 billion for its fourth fiscal quarter, in line with the consensus and up 51% on a reported basis. Adjusting for the VMWare acquisition, which was completed in early 2024, Broadcom reported organic revenue growth of 11%.

This was in line with the majority of its fiscal year and continues to show steadily improving demand after a cyclical dip in fiscal FY23, driven by a recovery in its most cyclical segments, which seems to have bottomed by now, and rapidly growing demand for AI adding another growth boost.

This brought the total revenue for the full fiscal year to a record-high $51.6 billion, up 44% year over year and 9% organically. Again, this shows a recovery from a tougher 2023.

However, it is worth noting that Broadcom isn’t that cyclical compared to many of its semiconductor peers, in part because of its revenue mix. For reference, Broadcom hasn’t reported a single quarter of negative YoY growth since 2013, even as the semiconductor industry has gone through a number of downturns over the last decade, and we have gone through a COVID-19 crisis and record high inflation in recent years.

Investors have nothing to complain about in terms of growth consistency, whether driven by acquisitions, excellent execution, or a good revenue mix. Historically, Broadcom has consistently outperformed, no matter the cycle's timing or the state of the economy.

On that note, let’s delve a little deeper into the performance of both of the company’s segments, starting with enterprise software.

Last quarter, Broadcom reported software revenue of $5.8 billion, up 196% YoY and now accounting for 41% of quarterly revenue. For the fiscal year, this brought software revenue to a total of $21.5 billion, up 181% YoY.

However, do note that this includes the addition of VMware, with the acquisition closed in early 2024. Talking of VMware, Broadcom reported that its integration is already largely complete, in well under 12 months, with revenue now in an upward trajectory and the business’ operating margin reaching 70% exiting 2024.

Furthermore, management is well on track to deliver incremental adjusted EBITDA at a level that significantly exceeds the $8.5 billion management guided for when it closed the deal. For reference, this was a three-year target, now most likely met in under a year, which is just another testimony to Broadcom’s ability to integrate and derive great value from acquisitions in no time.

The company continues to drive down VMware spending, which was only $1.2 billion in Q4, down from $1.3 billion in Q3 and way down from the $2.4 billion VMware spent per quarter prior to the acquisition. This translates into an operating margin of below 30%, which is already hitting 70% under Broadcom leadership.

Those are some incredible milestones hit in under a year. Pretty insane.

Meanwhile, Broadcom’s semiconductor segment is doing even better, driven by the influence of AI.

Semiconductor revenue in Q4 was $8.2 billion, up 12% year over year and 13% sequentially. It now represents 59% of total revenue, and full fiscal year semiconductor revenue hit a record high of $30.1 billion.

However, this was absolutely not driven by the entire segment. Broadcom's weakness in multiple end markets remains challenging, although a bottom is expected to be in place. You see, Broadcom operates across several end markets, such as server storage connectivity, wireless, broadband, and networking, and quite a few of these are heavily exposed to consumer electronics.

As a result, these revenues are highly cyclical, and Broadcom has felt this in recent quarters. Positively, most of these end markets have bottomed and are on the way up again.

In Q4, Broadcom reported server storage connectivity revenue had recovered by 20% from a bottom earlier this year, and this segment is expected to keep recovering gradually. The same can be said for the wireless segment, with revenue up to $2.2 billion in Q4, up 30% sequentially and 7% YoY.

Meanwhile, the broadband segment continues to struggle, reaching a likely bottom in Q4, with revenue of $465 million, down 51% YoY.

However, while these end-market and operations have struggled in fiscal FY24 due to cyclical demand pressures, this weakness was more than offset by Broadcom’s incredible AI-related revenue growth, almost entirely coming from its networking operations.

As I explained earlier, Broadcom is a massive beneficiary of AI thanks to its best-in-class networking equipment. These products are critical in next-generation data centers because they allow for the quick and accurate processing of large amounts of data. As AI requires more advanced networking solutions to process larger amounts of data faster, and big tech spends hundreds of billions of Capex to grow its computing capacity and speeds to stay ahead of the curve, you can see how this has been benefiting Broadcom and will continue to benefit it well into the future, as AI infrastructure spending is only expected to continue growing exponentially.

For Broadcom, AI isn’t used as a promise for future revenue growth; rather, it is already materializing and is clearly reflected in its financial results.

In Q4, AI revenue grew by a whopping 158% YoY to $3.7 billion, more than offsetting the 23% decline for non-AI-related semiconductor revenue.

For fiscal FY24, this resulted in a 220% increase YoY, with AI revenue of $12.2 billion, driven by the incredible demand Broadcom sees for its AI-dedicated networking products, in particular, its custom AI accelerators or XPUs from its three hyperscale customers, including Meta and Google, which led to a doubling of AI XPU shipments in Q4. When it comes to custom silicon, Broadcom is unequaled in the industry.

Broadcom’s AI-specific accelerators, all launched in recent quarters, are really top in their class. For example, its Jericho3-AI chip leads the industry with the ability to connect up to 32,000 AI accelerators at 800bps each. This not only means it already sees Meta and Google as loyal customers, but the company is also close to signing new deals with Microsoft and Amazon, which is a testimony to its dominance.

And as a result of all this, Broadcom’s AI revenue growth isn’t expected to slow down either, resulting in a very impressive outlook, but more on that later. Let’s first check out the bottom-line performance.

Broadcom reported an impressive 76.9% gross margin for its fiscal Q4, up 260 bps YoY. Meanwhile, operating costs grew as well due to the acquisition and consolidation of VMware. R&D specifically has been trending down some in recent quarters after the VMware bump and, as a percentage of revenue, has now normalized in the mid-teens, which is still a very respectable percentage, allowing Broadcom to maintain its edge over the competition.

This translated into a Q4 operating income of $8.8 billion, up 53% YoY and reflecting a 63% operating margin. Furthermore, adj. EBITDA was $9.1 billion, reflecting a 64.7% EBITDA margin, having recovered remarkably quickly from the VMware acquisition and not even that far away from all-time highs.

Broadcom’s margin profile remains best-in-class.

Ultimately, this resulted in an EPS of $1.42, up 28% YoY, and an FCF of $5.5 billion. This represents an FCF margin of 39%, which is somewhat lower than we’re used to from Broadcom. However, excluding the one-off restructuring and integration costs related to VMware, FCF would be closer to $6 billion at a 43% FCF margin, which is still sublime.

For fiscal FY24, this all resulted in a 42% increase in operating profit, $31.9 billion in EBITDA, and an FCF of $19.4 billion, up 10% YoY.

These resilient and still impressive cash flows allowed Broadcom to steadily retire the debt it had taken on to finalize the VMware acquisition in early 2024. Broadcom ended the quarter with $9.3 billion in total cash and a significant $69.8 billion in debt, which isn’t ideal.

However, considering Broadcom’s ability to generate significant cash flows, with FCF now expected to be well over $20 billion in the years ahead, I view this as manageable. Last quarter, the company lowered its debt pile by $2.5 billion.

Meanwhile, the company has also not forgotten about its shareholders. It returned an all-time high of $22 billion to them in FY24, including $9.8 billion in cash dividends and $12.4 billion in share repurchases and eliminations.

Also, management raised its dividend by 11%, maintaining an impressive dividend growth track record of 14 consecutive increases and a staggering 32% CAGR since 2016.

Today, this translates into a 1.06% yield based on a safe 45% payout ratio. I believe this is a great starting yield for a business growing as quickly as Broadcom and as committed to its shareholders.

In terms of performance and financials, I like Broadcom.

But what can we expect in the years ahead? Let’s find out.

Before we move on, just a quick word…

Rijnberk InvestInsights is a reader-supported publication. I try to keep most of my content free for everyone, but I can’t do this without your support!

So please subscribe and if you like our content and if you want to show even more appreciation for our work, please consider upgrading to paid (only $5 monthly).

In addition to all the free stuff, this also gets you access to the occasional premium analyses and full insight into my personal portfolio!

Outlook & Valuation

Unsurprisingly, the AI boom results in a very bullish medium-term outlook for Broadcom.

Crucially, current projections by Wall Street and hyperscalers for data center capex remain significant, directly benefiting Broadcom. For example, Broadcom customers Meta and Oracle expect capex to double by 2025, and Wall Street points to at least a 40% increase for the four big cloud companies.

Furthermore, Morgan Stanley analysts believe hyperscaler capex will hit $300 billion in 2025 and expects a whopping $1 trillion will be spent in the next few years on data centers, semiconductors, grid upgrades, and other AI infrastructure, all of which will lead to significant growth for Broadcom.

Based on this and the demand Hock Tan sees, he now believes Broadcom is looking at a serviceable addressable market (SAM) for custom AI accelerators of $60 billion to $90 billion in fiscal FY27 alone. This truly sent Wall Street into a frenzy, pushing shares up some 38% in the span of two days.

Also, note that Broadcom is talking about its SAM here, not its TAM. This revenue opportunity considers only the customers Broadcom is already servicing. In the meantime, the company is also close to signing deals with giants Microsoft and Amazon, which would at least double this SAM, of which Broadcom expects to take a significant share.

Furthermore, Broadcom points to significant visibility due to the fact that it is a multi-year cycle, not a quarter-to-quarter situation. In other words, these investments are highly likely to happen.

Even if Broadcom is able to just capture a 50% market share, at the low end of its current fiscal FY27 SAM estimate, AI revenue will at least double to $30 billion over the next two years, and that is as conservative as an estimate can be.

Do you now understand the optimism here? There is no way around it.

Alright, looking a bit more short-term, management issued solid guidance for its fiscal Q1. Management now guides for total Q1 revenue of $14.6 billion, up 22% YoY. This will consist of software revenue of $6.5 billion, up 41% YoY, and total semiconductor revenue of $8.1 billion, up 10% YoY.

Non-AI revenue has likely bottomed in fiscal FY24, and management expects a mild recovery to kick in in Q1 with mid-teens growth and a return to historical mid-single digits in the quarters that follow. Meanwhile, AI revenue is expected to grow 65% YoY to $3.8 billion. AI revenue will likely be stronger in the second half of the year, as Broadcom will start to ship its first 3nm XPUs, for which there will be high demand.

Finally, management expects the EBITDA margin to be 66% in Q1, setting a new multi-year high as VMware integration headwinds are likely to be behind the company.

All pretty great.

At the same time, in the medium term, some less positive considerations must also be made. Most important is the relative uncertainty around these data center capex budgets and their growth trajectory, especially as, so far, these insane investments have yet to pay off for the hyperscalers. Suppose the ramp-up in AI usage is less than expected, this could be impacting these budgets, which Broadcom really needs.

Especially now that AI is moving away from the cloud to on-device through Qualcomm, for example, I wonder how long these capex investments will be rewarding. I view this as a crucial uncertainty.

Also, it is no secret that Apple is actively looking to replace Broadcom’s Bluetooth and Wi-Fi chips with its own in-house product, which could risk some revenue. While this is in no way as significant as for Qualcomm, it could cost Broadcom billions in annual revenue, as Apple is one of Broadcom’s largest customers.

These are important considerations to keep in mind when working up growth projections, and all things considered, I now expect Broadcom to fully benefit from growing capex budgets in the next two fiscal years before easing a bit in fiscal FY27, as we might see somewhat of a stabilization in AI investments, at least by these hyperscalers. Meanwhile, non-AI semiconductor revenue should recover next fiscal year before returning to mid-single-digit growth, and I anticipate software revenue in the low teens.

Also, I believe Broadcom has plenty of room to improve margins in the years ahead, leading to even faster EPS growth, especially in fiscal FY25 and FY26.

Ultimately, these estimates and beliefs translate into the following growth projections.

Based on these updated projections and after last week’s big share price jump, Broadcom shares now trade at quite a demanding 34x next year’s earnings or a far from cheap 25x the current FY27 EPS estimate. This is especially a high price to pay considering it is an 70% premium compared to Broadcom’s 5-year average multiple and a 36% premium to the sector.

Of course, the impact of AI is a new factor here, and since this has led to a significant rise in financial growth expectations, a higher multiple is definitely warranted. However, I still wonder whether this AI enthusiasm has been a bit overdone.

For example, we are now looking at a PEG of 1.7, well above its historical average of 1.37. This is in line with the sector median but far from value territory. Also, current growth projections are highly dependent on hyperscaler capex budgets, which feels like quite a big uncertainty to factor in here as well, especially since this investment trajectory and the payoff are big questions for everyone.

Ultimately, while I like Broadcom and adore its superstar CEO, Hock Tan, the fundamentals make justifying the current multiple difficult. To warrant these multiples, one must assume Broadcom continues to see this kind of AI-related demand, probably through the end of the decade, something I am not convinced will happen.

Even when assuming a 30x long-term earnings multiple is fair and using my FY27 EPS estimate, I calculate a 2-year price target of $271. From current prices of around $220, this translates into potential annual returns (CAGR) of 11% or 12% including dividends.

This puts it right on the edge of buying territory, for me at least, thanks to shares giving away some of last week’s gains in recent days. This has taken the edge of a bit.

However, I am still not convinced that this risk-reward balance is favorable enough to pull the trigger right now.

Personally, I aim for a price closer to $205-$210, as this would allow me to buy shares at more favorable multiples, offer higher potential returns, and offer sufficient downside protection, even if AI investments ease off.

Therefore, after last week’s share price pop, I am staying on the sidelines, waiting for a deeper correction.

Looking to do your own stock analysis? Consider using StocksGuide, my go-to stock and business analysis tool. Check it out! Most of its features are free.

If you enjoyed this format and would like to see similar posts in the future, please hit the like button, share your comments, and be sure to subscribe.

thanks for inspiring me to try GPT-way

nice analysis, and colorful yaay (handt yet read it all!)

cant seem to find it

can you share RAW data sources (if you have them as list)