Earnings Reviews – Applied Materials & Airbnb

Here's all you need to know about two of last week's most anticipated Q4 earnings reports.

We are still in the midst of the fourth quarter earnings season, with plenty of developments and earnings reports to discuss and look into.

In this post, I aim to give you a thorough understanding of the quarterly numbers, developments, outlook, and valuation within 5-10 minutes read per business. This should give you guys a good sense of how the results impact an investment case and how the business is doing.

Sound good? Let’s delve in. For this week’s edition, I will dive into two of the most anticipated results from last week – those from Airbnb, which saw its share price pop nicely, and Applied Materials, which didn’t quite see a good reaction to its earnings report.

Plenty to go over, so let’s delve right in!

Applied Materials, Inc. ($AMAT) – Getting hit by export restrictions

On Thursday, February 14, Applied Materials (AMAT) released its fiscal Q1 earnings report. In past weeks, many AMAT WFE peers, like ASML, KLA, and Lam, already reported earnings, which impressed and were well received. Shares of each of these jumped post earnings amid low expectations.

However, the same cannot be said for AMAT, whose share price dipped by 8.2% during Friday’s trading session, mostly due to the Q2 outlook coming in short of expectations due to a considerable impact from Chinese export restrictions, which is expected to be felt most heavily next quarter.

Nevertheless, as a result of last week’s sell-off, AMAT shares are now down 9% over the last twelve months, sitting near a 12-month low and performing well short of a 24% return from the SMH semiconductor ETF. Furthermore, AMAT shares now trade at just 18x this year’s earnings, which is nowhere near the 25x sector median or the multiples awarded to its peers.

Have AMAT shares now been oversold, presenting a compelling opportunity to investors, or is the drop justified?

Let’s delve into the earnings report and find out!

Q4 and FY24 results + highlights

Fiscal Q1 revenue was $7.2 billion, up 7% YoY and roughly in line with the consensus.

System revenue was $5.36 billion, up 9% YoY.

AGS revenue (services) was $1.59 billion, up 8% YoY and accounting for 22% of total revenue.

This was another quarter of record-high revenues for AMAT, which is continuing to recover from a cyclical dip in 2023 and early 2024. However, AMAT was nowhere near impacted as heavily as many of its peers, with YoY revenue growth barely turning negative.

These results were mostly in line with expectations for both management and Wall Street, not showing a similar outperformance as we have seen from AMAT peers.

Crucially, AMAT was much more significantly impacted by U.S.-imposed Chinese export restrictions than its peers. In the systems segment, a 20% growth in foundry logic was offset by a decline in DRAM sales, mostly because prior-year sales to customers in China did not repeat due to these newly imposed restrictions in late 2024.

In addition, these restrictions hindered growth in service revenues, as AMAT lost a significant portion of its service business to Chinese customers.

This headwind will likely persist in 2025 due to a tough comparison to 2024, but it shouldn’t be a long-term issue. Revenue from China is now declining rapidly, lowering dependence. Therefore, I would say not to assign too much value to this headwind.

On another positive note, AMAT did outpace the broader market in 2024, registering another year of market share gains in leading-edge foundry logic, DRAM, and advanced packaging. Particularly in the latter, AMAT is doing really well, capturing half of the packaging equipment market in 2024 and remaining on track to double packaging revenues in the next several years.

AMAT’s broad product portfolio enables these market share gains. This portfolio allows AMAT to build strong customer relationships, maximize opportunities to sell systems, and rapidly grow recurring service revenues.

Through these relationships, a large portion of these service revenues come from multi-year subscriptions, which is brilliant because it makes these revenues anti-cyclical. Even amid current trade restrictions, management remains very bullish on this segment, pointing to a low double-digit growth CAGR over the long term.

This makes AMAT less and less cyclical, which will be favored by investors. This could earn it a higher multiple over time.

On that note, here are the bottom-line numbers.

The Q1 gross margin was 48.9%, up 100 bps YoY and reaching the highest level since 2000.

Q1 operating costs were $1.31 billion, up 7% YoY.

The Q1 operating margin was 30.6%, reaching the highest level since Q2 2022 and expanding 210 bps YoY.

Q1 EPS was $2.38, up 12% YoY and beating the consensus by $0.08 (a 3.5% beat).

Driven by a top-line recovery, several quarterly benefits, and tight cost control, AMAT delivered several all-time highs on its bottom line.

As for the gross margin, this YoY gain was driven by a very favorable mix and growth in the adoption of leading-edge, higher-margin technologies. Meanwhile, management also kept its costs well under control thanks to value-based pricing initiatives and cost reductions, limiting operating cost growth despite significant R&D investments.

For reference, R&D expenses grew 14% year over year, as AMAT remains fully focused on investing in technology to maintain its competitive edge and further increase its market share. As visible below, through the recent cycle, AMAT has not slowed investments into R&D for these exact reasons.

At the same time, marketing and SG&A expenses were down year over year, which led to operating cost growth of only 7% year over year, which was in line with revenue.

This led to solid EPS growth further down the line, driven by expanding margins and share repurchases.

In Q1, AMAT bought back $1.3 billion worth of shares (+$326 million in dividends).

It generated $544 million in FCF.

While shareholder returns far exceeded FCF last quarter, AMAT still maintains a healthy balance sheet with $0 net debt, comprised of a $6.3 billion total cash position and $6.3 billion in debt.

Financial health is no issue for AMAT.

Outlook & Valuation

Q2 revenue to be roughly $7.1 billion plus or minus $400 million, up 7% YoY at the midpoint.

Q2 EPS to be roughly $2.30, plus or minus $0.18, up 10% at the midpoint.

This isn’t the greatest of outlooks, with a further growth recovery staying out and missing the top-line consensus estimates for $7.2 billion.

However, there are a few important notes to be made here. Most importantly, this outlook includes a significant impact from export restrictions, estimated to amount to roughly $200 million in fiscal Q2 and $400 million in fiscal FY25.

Positively, this will only be a short-term headwind and not a massive longer-term drag, assuming no more significant restrictions are imposed. Once these 2024 quarters, including Chinese revenue, are lapped, growth should pick up a bit more, likely already visible in the second half of the fiscal year.

Meanwhile, Chinese revenues as a percentage of total revenue should drop below a normalized level of 30%, decreasing risk. However, they should still remain above average and higher than those of peers like ASML or Lam, which isn’t great.

Ultimately, this is another 30% at risk, something investors need to price in, especially amid a current trade war.

On a positive note, the structural tailwinds for AMAT and the semiconductor equipment industry remain strong. This is what management said during the earnings call:

“The major technology trends were shaping the global economy are made possible by advanced semiconductors underpinning long-term secular growth for the industry and especially Applied Materials.”

A big enabler of growth here will be, without a doubt, the AI revolution. Ultimately, advanced semiconductors are the key to energy and cost reductions needed to enable mainstream AI across all industries and formats.

As a result, last year alone, AI supported approximately 20% year-on-year growth of global semiconductor sales, pushing the market close to a $1 trillion value, likely to be hit well before 2030. This growth in demand for semiconductors will lead to higher demand for semiconductor manufacturing equipment by the likes of AMAT, ASML, and KLA, creating a compelling outlook for the WFE industry.

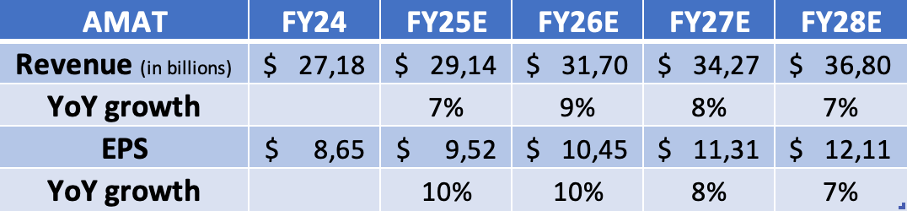

AMAT is well positioned for another decade of solid growth, as reflected in my current medium-term financial projections below.

Moving to valuation, we can see that AMAT shares now trade at 18x the current fiscal year EPS consensus. This multiple is roughly in line with AMAT’s 5-year average multiple but also a considerable discount to the peer average and a 29% discount to the semiconductor sector median.

Also, this reflects a PEG of 1.6x, which is a 5% premium to AMAT’s 5-year average and a 12% discount to the sector median.

All in all, I believe that, despite the discount to peers, AMAT shares currently trade roughly around fair value, mainly due to the consideration of a considerable China risk, which warrants a discount.

At the same time, AMAT still has a solid medium-term outlook, and thanks to the proliferation of AI and growth in demand for semiconductors, I strongly believe the outlook for the decade ahead remains solid. Therefore, I still believe AMAT deserves a slightly higher multiple, closer to 20x.

Using this and my FY27 EPS projection, I calculate a target price of $226 per share. From a current share price just below $170, this translates into potential annual returns (CAGR) of 10% or 11%, including the current 1% dividend yield.

Considering the China risk, this still isn’t enough to convince me to buy AMAT shares. Personally, I will need a bit more of a margin of safety to be interested in buying them. I am now aiming for a share price closer to $160, preferably below that.

Fundamentally, I prefer KLA, Lam, or ASML over AMAT.

For now, I am on the sidelines, waiting for some more weakness.

The remainder of this post is exclusively for paid subscribers.

Want to keep reading and receive even more of our investment insights on a monthly basis? Please consider upgrading to our paid tier (only $7.50 monthly or just $70 annually).

In addition to all the free stuff, this also gets you access to even more premium analyses (a total of 3 per month), full access to my own investment portfolio, immediate trade alerts in the subscriber chat, and a full overview of all my price targets and ratings, and even more!