KLA Corporation – One for on your watchlist, but don't pull the trigger yet (Earnings Review)

In this post, we review semiconductor gem KLA's recently released fiscal Q3 earnings report, which shows a bullish narrative for the semiconductor industry.

I last covered KLA KLAC 0.00%↑ at the end of January, following its fiscal Q2 earnings, rating the shares a hold at $599 per share. Notably, the hold rating was only the result of the company trading at quite a premium, but in the long term, it definitely stayed on our watchlist.

We can safely say the company has performed rather well since my last coverage. In just three months, it returned 15%, easily outperforming the benchmarks by quite some margin.

KLA is a tremendous company in the semiconductor industry with significant long-term growth potential thanks to its focus on several crucial semiconductor manufacturing processes, for which it develops high-end equipment. For those unfamiliar with the company, this is the description I used last time out:

“To put it more understandably and without going too much into detail (which most investors won’t care about), it provides a range of products and services to help semiconductor manufacturers monitor and control various aspects of the semiconductor manufacturing process to improve yield and efficiency by giving them tight control of their processes and by identifying issues in time. This means KLA’s products contribute to the precision, quality, and efficiency of semiconductor manufacturing by providing tools for accurate measurement, defect detection, and process control. These capabilities are essential for producing high-performance and reliable semiconductor products, and these are growing in importance.”

Obviously, this focus and these operations make it a prime beneficiary of the projected growth for the semiconductor industry and equipment market. For reference, the semiconductor equipment market, one of my absolute favorite industries, is projected to grow at a steady 10.4% CAGR through the end of the decade, according to Markets and Markets.

However, with this same industry suffering from a cyclical downturn in recent years, KLA has also been struggling a bit, which is reflected in its latest quarterly results, although it also shows the first signs of a recovery.

KLA released its fiscal Q3 earnings report last week, which was well received by the market. Shares ended the week up 12%, helped by overall good sentiment toward semiconductor stocks. This means shares are now up over 21% YTD and close to 100% over the last 12 months.

KLA reported revenue of $2.36 billion, down 3% YoY but beating the consensus marginally and performing pretty much in line with our projection of $2.35 billion. This also sat above the midpoint of management’s guidance.

This also included the impact of the U.S. restrictions regarding the export of products to China, which led to the company losing 1% in global market share, though on top of impressive gains in 2023. Still, KLA indicated that it lost access to 10% of its Chinese business, but it should have no further long-term significant effect.

Now, while revenue is still down YoY, the graph above shows a strong flattening of the trend after a rapid growth deceleration in fiscal 2023. As reflected in the Q3 results, management indicates that conditions in the industry have stabilized and expects it to recover steadily throughout 2024.

As a result, management is confident that the last quarter marked the bottom of the cycle for KLA, meaning growth is likely to return as early as next quarter, making the slump for the company considerably less deep and shorter compared to many peers.

An important factor in this is the significant revenue contribution from services, accounting for 25% of revenue. Services were once more the highlight of the earnings report, delivering 4% sequential growth and 12% YoY growth, highlighting their anti-cyclical nature.

KLA’s services segment mainly consists of servicing the company's equipment in customer factories to ensure optimal operation and equipment durability. As this type of equipment becomes more complicated to support smaller nodes and more advanced technologies, demand for the company’s services grows rapidly.

Positively, these services are contract-based and incredibly anti-cyclical. Ultimately, even as the industry goes through a downturn and customers aren’t looking to buy new KLA equipment, the existing machines still need to be serviced.

As a result, KLA’s services segment provides it with a reliable and anti-cyclical revenue stream. It also tends to outgrow its equipment business due to the growing number of active equipment globally, making the company as a whole less cyclical. This makes the segment incredibly important to the investment thesis here and has limited the revenue decline in recent quarters.

Moving to the bottom line, EPS came in at $5.26, beating the consensus by $0.20 or about 4% but missing our expectations by $0.43. While this might seem like a significant miss, this includes a $0.40 impact from excess and obsolete inventory related to the company's strategic decision to exit the flat panel display business, which was announced in March and, therefore, included in Wall Street’s projection but not in ours. Excluding this impact, the company pretty much performed as expected.

On the margin front, this one-off had an impact across the board. The gross margin came in at 59.8% but would have been 62.8%, which is roughly flat sequentially. Furthermore, the operating margin contracted by 200 bps YoY to 36.8% but would have been up YoY if it weren’t for the one-off. Therefore, on the margin front, the company definitely performed exceptionally well.

Operating expenses were down YoY thanks to a 2% decline in R&D costs. This led to a net income of $715 million, reflecting a net income margin of 30.3%, down 100bps YoY and resulting in the earlier mentioned EPS.

Finally, FCF came in at $838 million last quarter, bringing the TTM total to $3.1 billion, representing an industry-leading FCF margin of 32%, which is especially impressive considering the headwinds the business has faced in recent years.

This allowed it to maintain its solid financial health while also returning cash to shareholders. In the latest quarter, the company returned the majority of its FCF ($569 million) to shareholders through its dividend and share repurchases. Nevertheless, the balance sheet remained healthy, with $4.3 billion in cash and $6.7 billion in debt.

We can safely say this management team is very much committed to its shareholders. Thanks to consistent share repurchases, the share count has been lowered by 19% over the last decade. The company has also grown its dividend at a 16% CAGR since 2006, or for 14 straight years.

For reference, shares now yield around 0.82% based on a payout ratio of just 24%, also based on somewhat depressed earnings. Therefore, we firmly believe investors are in for many more dividend increases. Looking at the company’s growth projections, another ten years of dividend growth at a double-digit CAGR is very likely, making it a prime dividend growth investment.

Outlook & Valuation

Overall, KLA performed pretty much as expected, which is exactly what you want it to do consistently. Guidance-wise, this was a similar story, with management guidance falling right in line with expectations.

As discussed earlier, conditions for the company are clearly improving and expected to steadily recover through the remainder of 2024, which gives management confidence in its next quarter. Growth is expected to return in the June quarter – the company’s fiscal Q4.

Management now guides for revenue of $2.5 billion, plus or minus $125 million, which aligns with our earlier projections and reflects growth of 6.2% YoY. This highlights a significant improvement in growth from prior quarters.

Meanwhile, the gross margin is expected to be around 61.5%, plus or minus one percentage point, depending on the product mix. This translates into an EPS guidance of $6.07, plus or minus $0.60, with the midpoint bang on in line with our estimates.

Taking this into account, management has left its outlook for the calendar year 2024 unchanged. It continues to expect WFE demand to be roughly flat to up modestly from 2023, driven by a stronger second half.

In the longer term, KLA continues to enjoy a number of tailwinds, including the significant investments made by clients in the development of advanced nodes, slowly rising capital intensity, and “the increasing complexity in advanced packaging applications for AI and other advanced technologies,” as management explained it, which drives significant demand for KLA’s machines.

In simple terms, as technology requirements grow, so does the need for KLA’s industry-leading inspection and metrology systems, which are becoming increasingly important. Notably, the company holds a demanding 56% market share in this piece of the semiconductor value chain, putting it in a prime position.

Meanwhile, the company’s advanced packaging business is also firing on all cylinders. While this one is rather small in terms of revenue at a $400 million run rate, management continues to expect this segment to continue growing meaningfully above the WFE industry.

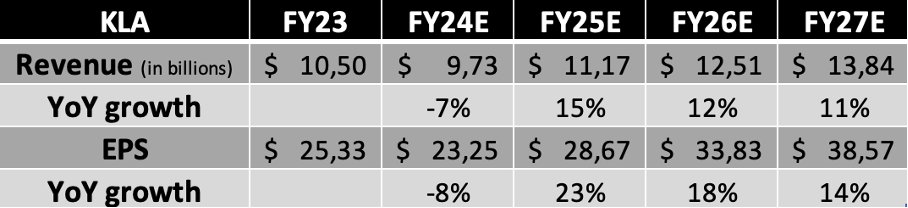

All taken into consideration, we have left our revenue projections for KLA’s fiscal Q4, ending in June, unchanged and have lowered our EPS projection in line with the Q3 miss due to a one-off.

However, in the longer term, especially looking at fiscal FY25, we have turned more bullish. We have raised our estimates for fiscal FY25 quite significantly, better reflecting the expected uptick in WFE demand heading into the second half of calendar year 2024. Furthermore, I have also meaningfully increased both revenue and EPS projections for FY25 and FY26, as the semiconductor industry is projected to experience solid growth in these years, and KLA is in a top position to benefit.

This results in the following financial projections.

Looking at the company’s favorable positioning, growing importance to clients, growing services segment (lower sensitivity to the cycles), and impressive growth outlook, I continue to believe a 25x P/E multiple is fair here, which is roughly in line with the sector median and peers.

However, while my financial projections have improved, its share price has also risen further from when I last covered these, growing by over 15%. As a result, shares remain quite expensive, already trading at 24x FY25 earnings. This makes shares pretty much fully valued.

Taking our FY26 projections and using a 24x multiple to give us some more margin of safety, I calculate a target price of $812. This leaves us with potential returns limited to 7.5% annually, which just isn’t enough to warrant a buy rating here.

Therefore, despite my bullish view of the company, I continue to rate KLA shares a hold and will look to buy shares on a dip below $655 per share, which would better position me for double-digit, market-beating returns. We saw this level as recently as one week ago, and with current market volatility, I believe we could hit these levels in the next couple of months.

Let us know your thoughts in the comments! Also, please leave a like if this post was of value to you!

Please remember that this is no financial or investment advice and is for educational and informative purposes only. We are simply sharing our views, actions, and opinions, which we hope will be insightful!

Great pos on of the best companies in the semiconductor sector👍

I’ll include the link into todays Friday Roundup, which will be shared later today😉