Lowe’s Stock Analysis: Is This Dividend King a Buy in 2025?

This isn’t the time to chase hype. It’s the time to buy high-quality compounders at reasonable prices.

Last week, on May 21, Lowe’s Companies, the second-largest home improvement retailer in the U.S., released its fiscal Q1 earnings report, which eventually failed to impress Wall Street, with shares losing about 2% in the following session and 1% over the past week.

On the one hand, Lowe’s did impress by reaffirming its FY25 guidance, just days after its larger peer Home Depot did the exact same, despite high uncertainty and a challenging operating environment amid cautious consumer spending. Yet, on the other hand, its Q1 results, although in line with guidance and expectations, continue to reflect consumer spending weakness, which investors fear might persist well into 2026, especially with the U.S. economy shrinking and on the brink of a potential, albeit shallow, recession.

One thing is certain: such an economic slowdown or at least prolonged economic weakness isn’t great for a home improvement retailer like Lowe’s, which is heavily dependent on the health and discretionary spending habits of the U.S. consumer.

So, unsurprisingly, investors are cautious, and after Lowe’s shares had already gained following a solid report from Home Depot a few days prior, Lowe’s didn’t offer enough in its Q1 report to impress and convince shareholders, leaving shares practically flat over the last 12 months.

At the same time, there is also room for positives, especially when examining Lowe’s from a fundamental standpoint and looking past its near-term weakness, which will ultimately be most valuable to investors in the long run.

You see, under the hood, despite temporary headwinds, Lowe’s management is steadily and surely improving the business, fueling long-term growth by better positioning the company to compete. For example, for years, the company has been investing heavily in the “Pro” market, which has historically been dominated by Home Depot, but Lowe’s is making significant strides with an aggressive approach, leading to some market share gains in a very compelling market vertical. Additionally, Lowe’s significant investments in its tech stack and online platform are also paying off in a big way, boosting sales growth.

In other words, Lowe’s continues to invest in the right areas and is showing strong results that should drive long-term sales growth in a healthy underlying market. The underlying narrative is straightforward: Lowe’s is gaining market share and outpacing the market. Under this management team, I am confident that the company can maintain this momentum, likely enabling it to outpace the underlying market.

Yes, I am still bullish on Lowe’s. The company is really nailing it; the results just don’t show it due to external temporary pressures.

As for the home improvement market, I still believe it is quite compelling, despite its cyclical nature. While the industry is highly sensitive to shifting mortgage rates, disposable income levels, the health of the housing market, and the state of the economy in general, there are also factors that can offset these effects.

Take the growing numbers of investments by homeowners in their properties, whether through renovations, upgrades, or essential repairs, which is slowly turning into a secular trend, driven by a combination of rising home values, the desire for personalization, and the need to adapt living spaces to changing lifestyles, such as the shift toward remote work in recent years. Additionally, considering that more than 50 percent of the homes in the U.S. were built before 1980, homeowners are likely to continue investing in making these homes to their liking and making them livable.

As a result of tailwinds like these and many others, the industry is still expected to grow at a 5.2% CAGR through 2032, which is quite impressive. Additionally, in terms of longevity, investors also haven’t got anything to worry about. I bet people will still be building, renovating, or improving houses in 100 years’ time. And with its mighty moat and big market share, Lowe’s is poised to benefit.

So, yes, I remain quite bullish in the long run. Yet, of course, this doesn’t make Lowe’s a buy at any price. Especially amid the currently elevated uncertainty and risk of prolonged economic weakness, we should be cautious not to overpay.

So, after last week’s results and management’s commentary, are shares worth buying?

External headwinds cloud a solid report

As I said, Lowe’s Q1 report continued to show broad-based weakness, driven by external factors. The company sees ongoing challenges in the housing market amid high rates, which put pressure on borrowing, keeping home improvements to a minimum. Unsurprisingly, this wasn’t helped by Trump’s announced reciprocal tariffs, which only put consumer spending under additional pressure, while also ensuring rates will remain higher for longer.

This definitely isn’t a great backdrop.

This weakness and the subsequent macro uncertainty are also reflected strongly in consumer spending trends, with Lowe’s facing ongoing pressure in DIY discretionary demand. Especially bigger ticket projects remain under pressure in interior categories like flooring, kitchens, and baths, with consumers choosing to delay such larger purchases.

Add to this some exceptionally unfavorable weather across much of the country in February and a slower start to spring compared to last year, and the company delivered a Q1 report that shows broad-based weakness.

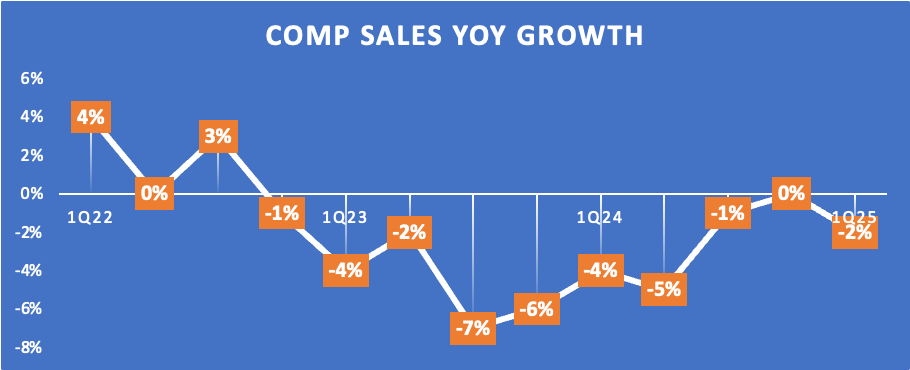

Lowe’s delivered total sales of $20.9 billion for the quarter, down 1.7% YoY on a comparable basis, which was in line with expectations and missed the Wall Street consensus by a slim margin. As shown below, this reflects a slight decline in growth compared to the two previous quarters, but this was primarily due to one-off effects, such as the later start to spring and poor weather in February.

For reference, excluding the Easter shift in April, comparable sales in March were down only 0.9% and improved further to a positive 0.2% in April.

Looking at the underlying growth numbers, we can see that the comparable average ticket was up 2.1%, driven by a continued outperformance of higher ticket categories like Pro and Appliances, offsetting weakness in small ticket categories like DIY. For reference, comparable sales for large tickets ($500+) were up 1.3% in Q1, while the smallest category (below $100) was down 3.4%. As a result, the average ticket growth of 2% was roughly stable compared to prior quarters.

Further reflecting demand weakness is a 3.8% drop in comparable transactions, which is significantly weaker than recent quarters, as shown below. Similar to sales growth, this was driven by unfavorable weather, which pressures spring traffic. Showing just how significant this impact is, February comps were down 5.4%, but quickly improved in March to a positive 1.7% growth as weather conditions improved. Therefore, this headline number below isn’t a good reflection of actual demand.

Meanwhile, despite external headwinds weakening demand, Lowe’s remains focused on its key pillars, delivering strong numbers for Pro and online sales, which continue to be its two focus points and growth drivers.

Starting with Pro sales, Lowe’s delivered healthy, positive comparable growth in the mid-single digits, driven by some mild market share gains. Ever since 2018, Lowe’s management has been laser-focused on the professional home improvement market, a market Lowe’s has historically been less dominant in due to the sheer dominance by Home Depot, whereas Lowe’s is looking much stronger in the less appealing and much more cyclical DIY market.

You see, as it has always been, the Pro market is much more interesting to these two home improvement giants, as this market vertical is considerably more resilient and much less cyclical due to the lower sensitivity to consumer discretionary spending. Whereas DIY sales can drop significantly when consumers start spending less, home builders or other professionals don’t just stop their entire business; instead, they continue to work and purchase supplies. Yes, these will also face economic headwinds, but to a much lesser degree, which is exactly why Home Depot delivered positive comparable sales and transaction growth in Q1, whereas Lowe’s saw much more weakness due to its greater exposure to the DIY market.

Positively, Lowe’s has been making great gains in the Pro market, gaining market share over recent years and seeing this grow as a percentage of revenue. This is driven by a transformed “Pro product and service offering, featuring a powerful program lineup, targeted inventory investments, and a competitive loyalty program”, as cited by management.

However, despite ongoing success, management remains aggressive in its approach, announcing the $1.3 billion acquisition of Artisan Design Group in April, which is a leading nationwide provider of design, distribution and installation services for interior surface finishes, including flooring, cabinets and countertops, to national, regional and local homebuilders and property managers.

Ultimately, Lowe’s believes this will enable it to increase its penetration of the Pro segment, thereby gaining further market share in this highly fragmented market, an idea shared by investment bank Jefferies.

I must say that I really like Lowe's aggressive approach, which should ultimately benefit the company in the long run.

Meanwhile, the company’s investments in its online platform and tech stack also continue to pay off nicely. In recent years, Lowe’s has been investing heavily in its tech stack and online platform to enhance its online presence and improve customer availability and convenience.

As a result, in Q1, online sales were up 6% YoY, driven by growth in both traffic and conversion rates. These recent investments have been a significant boost to Lowe’s sales, as they make the company more accessible to customers, thereby improving sales and traffic.

As clearly visible last quarter, it’s these efforts that offset the general demand weakness and drive growth in a healthy demand environment.

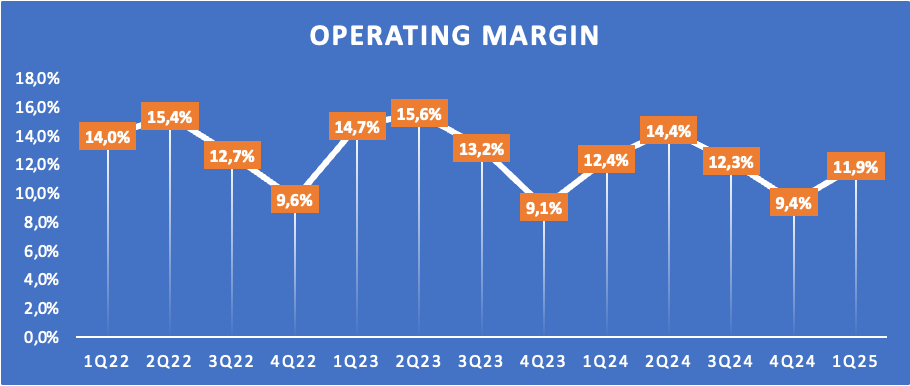

Moving to the Q1 bottom-line performance, Lowe’s continued to deliver strong and healthy margins despite top-line weakness. Lowe’s reported a gross margin of 33.4% in Q1, up 20 bps YoY, thanks to multiple PPI initiatives that offset the impact of lower revenue. As visualized below, Lowe’s gross margin has been fairly consistent over recent years, despite poor top-line growth, highlighting the company’s strong cost management and pricing power.

Further down the line, the company reported an SG&A accounting for 19.3% of revenue, up roughly 60 bps YoY due to lower sales, the wrap of incremental wage actions for frontline associates, and higher health care-related costs.

As a result, the operating margin was down 50 bps YoY to 11.9%. As shown below, Lowe’s operating margin has faced pressure in recent years, being hit harder by the decline in sales, which has coincided with continued investments in the business. This is mostly the usual cyclicality.

Ultimately, this resulted in an EPS of $2.92, which was in line with guidance and down 5% YoY, reflecting the further margin slump amid cyclical pressures. Positively, Lowe’s did continue to generate healthy cash flows, delivering an FCF of $2.9 billion, even amid heightened CapEx investments into the construction of new stores.

Q1 FCF nicely covered the $645 million Lowe’s paid out in dividends and the $750 million it repaid in debt maturities to bring its debt-to-EBITDA ratio below 3x, while the company also kept its ROIC nicely above 30%.

In addition, Lowe’s also acquired Artisan Design Group for $1.3 billion in cash, which is why Lowe’s has decided to halt share repurchases for the year to not put further pressure on its balance sheet and leave enough breathing room to comfortably repay the remaining $1.75 billion in bonds maturing in September.

Though investors still have nothing to complain about as Lowe’s has retired a whopping 47% of its outstanding shares over the last decade, significantly increasing shareholder value and fueling its strong share price returns of 216%.

Additionally, investors still receive a solid dividend now yielding 2% based on a well-supported 39% payout ratio. Even more impressively, Lowe’s has increased this dividend for 61 consecutive years (making it a true dividend king) and has grown it at a 16% compound annual growth rate (CAGR) over the last five years.

Investors still get handsomely rewarded.

Before we move on, just a quick word…

Want more out of your subscription?

InvestInsights PRO - $7.50/month ($70/annually)

An additional 2-6x/month premium stock analysis.

Full insight into my own portfolio (15% return CAGR since 2022).

Monthly portfolio updates + Instant transaction alerts (Fully transparent)

A complete overview of all my target prices and ratings (Excel file).

2x/month The Watchlist Report

Instant access to earlier premium analysis on, for example, Adobe, Thermo Fisher, Spotify, and The Trade Desk.

The remainder of this post, including the outlook, valuation, and conclusion, is for PRO subscribers only.