Market Review – Brace Yourself For A 5-10% Correction

Market performance review

“A new day, a new all-time high.” This is pretty much the line with which we could have started each and every post so far this year. From stocks to bitcoin, asset classes across the board have been hitting uncharted territories as optimism ruled on Wall Street in the first two months, even in the face of significant headwinds and uncertainties. Honestly, after making some terrific gains last year, I never expected to start this year with portfolio gains exceeding 10% again.

However, markets have lost some momentum over the last two weeks. Markets are down so far this month, although only marginally. Over the last two weeks, the S&P 500 is down by 0.35%, followed by the Dow Jones, down 0.8%, and the Nasdaq, declining the most with a 1.62% pullback so far this month.

Of course, ultimately, these are no significant declines in any way. It seems to be a period in which investors take a breather and take some gains here and there, reallocating capital after great gains since October. I have been doing the exact same.

This reallocation is highlighted by the fact that while inflows were solid for a seventh consecutive week last week, with $91 billion worth of inflows, technology funds faced the largest outflow ever in a single week, $4.4 billion, as some investors are taking profits in overvalued technology stocks, those that have run the hottest since October or pretty much over the last 1.5 years.

According to Scott Wren, Senior Global Market strategist, what we are seeing now is no more than investors “taking a little money off the table.” He believes we could see more of these outflows in the coming weeks, leading to a potential market correction of 5-10%, which would help markets cool down and give you and me some prime opportunities.

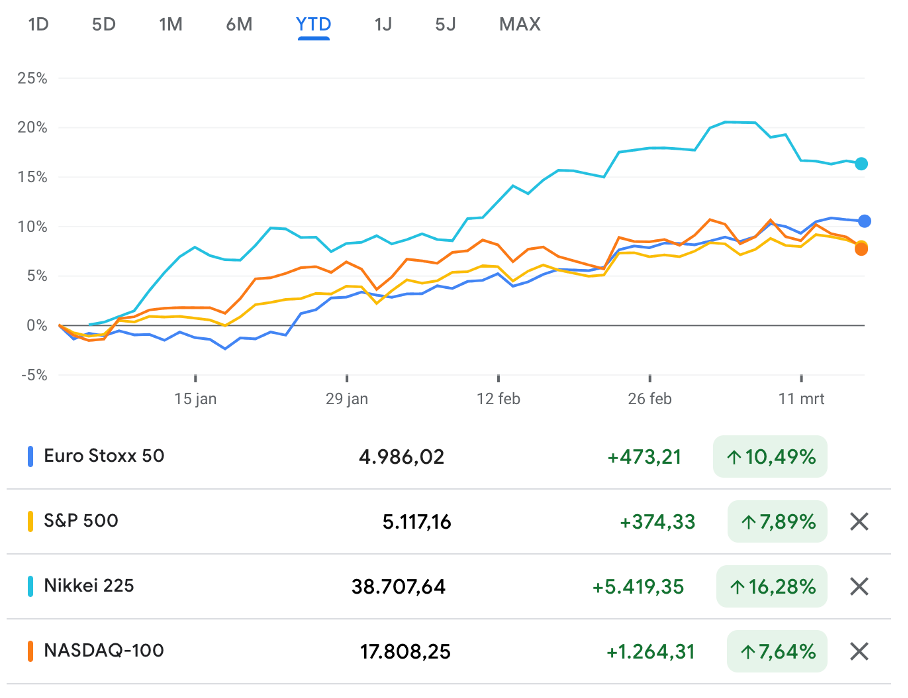

Overall, with gains of over 7% for the S&P 500 and Nasdaq, investors can only be satisfied with their performance this year. Also, what is remarkable is that large European indices continue to outperform their U.S. counterparts so far this year, something that occurs very seldom. So far this year, the Euro Stoxx 50 is up 10.5%, while the French CAC 40 and Dutch AEX also outperform U.S. benchmarks with gains of over 8%.

However, the real outperformer is the Japanese Nikkei-225 index, which has gained a whopping 16% so far this year and 43% over the last year. This 12-month performance is in line with the technology-heavy Nasdaq-100. It is truly a great performance and one supported by fundamentals as well.

For those interested in a deeper dive into this market and its potential, this post from

is definitely worth reading. Spoiler: after reading it and taking a closer look at the country, we bought a position in a Japanese ETF.

Are gains supported by fundamentals? Opinions differ.

However, whether the rest of the market gains so far are also supported by fundamentals is a big question mark. Those who have read our previous “Weekly Insight” posts will very well know that we definitely don’t believe so, and our opinion today remains the same.

However, on Wall Street, opinions are mixed. Barclays stated just last week that it believes the bull run in the world’s biggest tech stocks, driving a significant portion of the 2023 gains, is sustainable. According to the Barclays research team, fundamentals still support the run-up in share price, and the high valuation reflects high-quality earnings growth.

In addition, Citi analysts indicated last week that their research showed the benchmark can climb as high as 5,700 in its bull case scenario, which represents another 10% upside this year.

On the other hand, Morgan Stanley indicated that it sees no reason to upgrade its S&P 500 price target. The investment bank maintains its bearish price target of 4,500, which sits far below current levels. The analyst team continues to believe that current levels are pricing in too much optimism and are not supported by fundamentals. As a result, the firm sees no reason to increase its price target and, therefore, projects a correction sometime this year.

Clearly, opinions on Wall Street are very mixed, and analysts don’t quite seem to agree. Considering some of the recent target price upgrades, the midpoint prediction now appears to be somewhere around the 5,150 mark. This is roughly today’s level, and it is within the range we predicted at the start of the year with a base case scenario of 5,000 and a more optimistic prediction of 5,200. For now, we will stick with this prediction and review it in more detail at the start of June.

Ultimately, we can safely say the markets remain in a healthy condition with solid inflows and stable returns, supported by growing corporate earnings despite inflation and geopolitical pressures. Though, at the same time, we can see the first cracks in investor sentiment starting to appear, which can be primarily attributed to a treacherous dynamic between inflationary pressures and a resilient economy.

Most of this year’s gains so far are driven by a combination of optimistic rate cut expectations, trending down inflation, the promise of AI, and the economy remaining incredibly resilient. However, the latest data gives reason for concern, and it appears traders and investors might be pricing in too optimistic scenarios for this year, although this is hard to tell right now.

The latest data shows inflation is sticky, putting early rate cuts in danger.

While inflation has been trending down strongly over the last year or so, fueling optimism on Wall Street, macroeconomic data that came out over the last week points to a reversing trend and stickier-than-expected inflation, something we have been warning about since the start of the year.

Let’s start with the wholesale prices report for February, which came in hotter than expected. The PPI jumped 0.6% on the month, far higher than the 0.3% expected and 0.3% reported for January. Even when excluding volatile food and energy prices, the core PPI, which is seen as the leading indicator for the Fed, still came in above expectations.

Furthermore, the headline number increased by 1.6% year over year, the biggest increase since September. This shows that inflation is not trending down as fast as expected and is even trending in the wrong direction, showing the most significant jump in over half a year, fueling fears that we might have to wait for the first rate cut longer than is anticipated.

In addition to this data, the CPI in February rose 3.2% Year over Year and 0.4% monthly. This monthly number matched the consensus but was still an acceleration from the 0.3% reported in January. Similarly, the YoY number was also up from the 3.1% reported in January and sat above the consensus, once more showing that disinflation is stagnating.

Furthermore, core CPI was up 0.4% YoY compared to a 0.3% consensus, and the leading reason for this miss was once again shelter prices as home prices continued to rise and rent prices only moderated slowly.

Clearly, these aren’t the numbers investors were hoping for, as inflation is no longer trending down as strongly as it used to and seems to have settled above 3%. Pretty much everything right now points to inflation being stickier than anticipated. Honestly, based on this data and the fact that the economy won’t budge, a rate cut is simply not possible and would endanger the Fed’s entire progress.

According to Steven Blitz, chief U.S. economist at TS Lombard, disinflation seems to be stalling and even reversing, not supporting any thought of rate cuts any time soon.

Obviously, inflation shows no strong signs of slowing down further and remains above 3% or even trends up again over the next few months. In that case, the Fed will need to strongly reconsider its rate cut expectations. They have already communicated that the decision will be entirely data-driven and that as long as they have no confidence that inflation is nearing the 2% target, rate cuts are out of the question as long as the economy and labor market remain in excellent shape.

Further adding to these fears, retail sales were up 0.6% in February, slightly missing a 0.8% consensus but nevertheless improving from a 1.1% slump in January. Add to this a decline in unemployment claims to 209,000, below a 218,000 consensus, and we can safely say the U.S. economy remains in a good place based on recent data. This still supports the expectations for a soft landing but also further encourages the Fed to keep rates higher for longer.

However, on a slightly positive note, data from the Labor Department in the week before showed that the unemployment rate jumped and wage gains moderated, which keeps hopes for a June rate cut at least somewhat alive, in the public’s opinion.

The report showed that U.S. nonfarm payrolls climbed by 275,000 in February, above the consensus of 190,000 and up from 229,000 in January. However, we should note that these numbers are subject to a later revision, so this is hard to go by.

Positively, the unemployment rate went from 3.7% to 3.9%, and wage growth moderated to just 0.1%. This could potentially allow the Fed to keep its rate cut considerations for June alive, although this could be a long shot. In our opinion, we will need more evidence of a moderating labor market before we can confidently consider an early rate cut.

Meanwhile, the ECB, or European Central Bank, kept rates flat two weeks ago, as expected. However, the central bank did indicate that inflation is easing faster than previously thought, preparing the market for rate cuts later this year. The officials also lower revised their inflation projections for the next three years, now projecting average inflation of 2.4% in 2024, 2% in 2025, and 1.9% in 2026, which is a big positive for investors.

However, the chief economist from the ECB stated last week that while disinflation is in progress, the central bank should take its time before lowering rates again. He expects that by June, officials should have a better picture of the inflation trajectory, mainly focusing on wages in the coming months.

Meanwhile, investors now price in a total of three or four rate cuts this year to 3.25% or 3% by December, which is slightly more positive compared to an earlier expected three rate cuts. The first cut is now expected in June, which seems realistic.

Making up the balance, there might still be too much optimism priced in

Looking at the latest data from CME Group, investors now price in the first U.S. interest rate cut in June, followed by a cut in September and a final one in December. This should bring the 2024 total to 75 bps and the interest rates down to 4.50-4.75%, which is perfectly in line with the Federal Reserve's guidance and quite a bit below previous expectations.

However, while the 75 bps of rate cuts for 2024 currently priced in seem realistic(ish), we believe the most recent inflation data could suggest that this is still slightly too optimistic. Inflation remains sticky and currently seems to settle above the 3% mark, which, in combination with a resilient labor market, won’t be enough for the Fed to lower rates. Thus, the macroeconomic data will be critical to the decision-making over the next few months.

A first rate cut in June is most certainly not set in stone yet, and we could be in for a negative surprise if inflation does not trend down more strongly over the next couple of months.

For now, investors seem to want to give it another month after the missed expectations over February not being all too shocking and not resulting in significant movements in the market. However, the market is on edge, and positive sentiment is slowly fading. As a result, we won’t need a big miss in March data for the market to freak out and seriously start worrying about the rate cut trajectory, and rightfully so.

We believe we are in for a reality check, and a 5-10% correction is likely before the summer if inflation data does not significantly improve.

One thing is for sure: There is no upside to currently priced-in expectations, and we expect little positive catalysts on this front to keep pushing markets up. Rather, we expect quite a bit of volatility in the coming months and potentially a slight correction.

Would ask us about our rate cut projections; going by the most recent data, we now expect a first cut in July/September, followed by a cut in December, resulting in a total of 50-75 bps of rate cuts (we believe December could be a 50 bps cut if inflation gets close to the 2% target by year’s end)

And yet, while we are very pessimistic and believe there is barely any sustainable upside in the market left at this point, we are not moving to cash or other securities but remain fully invested in the stock market. Why? Simply because history has proven that not being invested for even as short as 30 days can result in significantly lower returns.

This happened to be pointed out by Lee Baker, a certified financial planner and founder of Apex Financial Services, saying: “Getting in and out of the market, it’s a loser’s game. Why? Pulling out during volatile periods may cause investors to miss the market’s biggest trading days — thereby sacrificing significant earnings.” “The markets not only are unpredictable, but when you have these moves, they happen very quickly,” added Baker, a member of CNBC’s Advisor Council.

Furthermore, we are long-term-oriented investors, and while we are also absolutely not making any purchases at current levels and are moving funds around, we also do not feel the need to cut on our long-term investments.

We are happy to stay put in the downswings as much as the upswings as long as our investment thesis remains intact. There is simply no reason for long-term investors to start selling right now—there are only plenty of reasons not to buy unless you find an underestimated or mispriced opportunity.

So, in our view, prepare for a correction and some downside, but don’t freak out. Stay invested in high-quality stocks with solid fundamentals.

Headlines you might have missed…

Apple faces headwinds in China, but the sell-off is called overdone

Apple has been THE underperformer among “Big Tech” so far this year, with shares down roughly 10% against significant gains for its big tech peers, potentially making shares attractive. According to Evercore analysts, the underperformance can be attributed to three factors: capital reallocation, regulatory issues, and declining Chinese sales.

According to Evercore, investors are reallocating their funds so far this year toward AI leaders like Nvidia and Microsoft, a subject in which Apple has been remarkably quiet so far. This has led to some taking funds away from Apple. On top of this, investors are also increasingly concerned about the regulatory headwinds the world’s second-largest public company is facing. Just recently, the company received a €2 billion fine from the European Union, accentuating these concerns.

Finally, and most significantly, Apple has been facing significant headwinds in China, where it seems to be losing market share. According to Counterpoint Research, the company’s sales plunged in the first six weeks in China, down a whopping 24% YoY, which is massive.

This Year-over-Year decline can be mostly attributed to Huawei's resurgence, which is seeing incredible success with its latest Mate 60 smartphone. In recent years, Huawei wasn’t in the picture due to the U.S. restrictions keeping it from using American (Qualcomm’s) 5G modems, making it tough for the company to compete. However, it has now finally released competitive 5G smartphones, which are gaining incredible attention from the Chinese consumer and hurting Apple. For reference, Huawei shipments were up 64% over the same period.

However, despite Apple's loss of market share in China, Evercore analysts called the sell-off of Apple shares overdone and maintained a $220 price target. The analysts see strong support at current levels to 10% down, potential catalysts in AI product releases, and a risk-off move from investors taking profits in hot AI stocks.

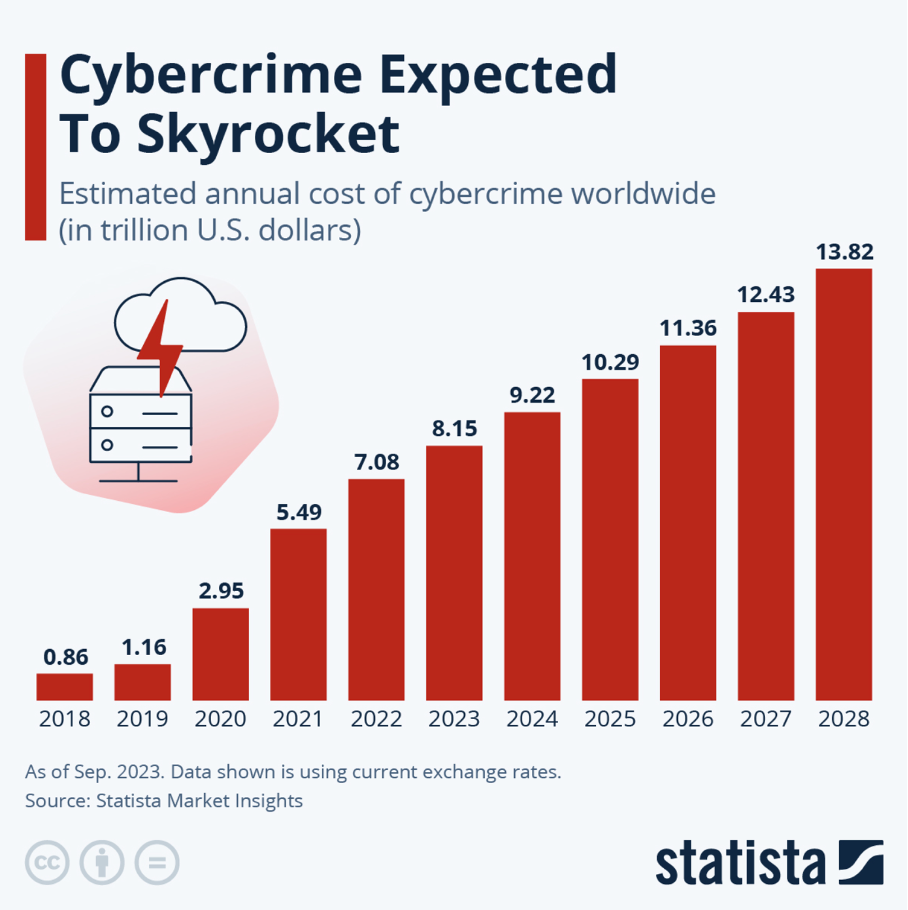

The future of cybersecurity and criminality is AI

That cybersecurity is becoming a more important theme globally is nothing new. Just check out the growth in cyber attacks below and consider the market’s growth outlook, pointing to growth at a CAGR of 12.3%.

According to Crowdstrike CEO Kurtz, the number of cyber criminals is growing as these “increasingly have access to advanced generative artificial intelligence and can carry out attacks even if they themselves are less skilled.” This means that AI not only makes cyber attacks more advanced but also makes them more recurring due to lower bars.

Furthermore, according to the CEO, AI will significantly shift the cybersecurity landscape. Legacy technologies simply can’t keep up with the advancements made in cyber attacks, making companies globally shift to more advanced technologies like those offered by Crowdstrike, Palo Alto, and Zscaler, which leverage generative AI to improve their software. According to Kurtz, “It’s going to be the battle of AI in the future.”

This shift is causing some companies to grow frustrated with their legacy technologies, allowing Crowdstrike to make massive customer wins and grow rapidly. Obviously, cybersecurity is not only a rapidly growing but also a fast-evolving market, where the most advanced players appear to be the long-term winners.

Is Walmart the latest understated beneficiary of AI, and is it threatening Alphabet?

In its recent investor call, Walmart introduced the idea of some incredibly exciting features with regard to AI. Particularly, the company aims to disrupt Alphabet’s (Google) business by allowing consumers to search for what they need in its app or on its website, using generative AI.

This way, consumers won’t need to search on Google for all the things they need to host a Super Bowl party or Valentine’s Day celebration, but they could use Walmart’s internal search engine as a one-stop shop.

Interested in the how and when? Make sure to check out this article on CNBC. It is a great read, perfectly explaining what this means for Alphabet (Google) and the “search” industry as a whole.

Boeing can’t seem to get a break

YTD, Boeing shares are down a whopping 30% now as the company does not seem to be able to get a break with its planes experiencing incident after incident. After the Alaska Airlines incident at the start of the year, a number of other incidents were reported over the last two weeks alone.

For starters, last week, a Boeing 787 Dreamliner from LatAm Airlines took a nose dive approximately halfway through the flight, leading to several injuries among the 50 passengers, though nothing too serious. According to the latest insights from the Wall Street Journal, the nosedive was caused by a mishap in the cockpit as “a flight attendant serving a meal hit a switch on the pilot’s seat, pushing the pilot into the controls.” In other words, the issue does not seem to be Boeing-related, but shares did lose an additional 3% on the news.

In addition, a Boeing 777 was forced to make an emergency landing at Los Angeles International Airport due to a mechanical issue, which is unclear at this time.

On top of this, a United Airlines Boeing 777 also experienced a serious issue and was forced to make an emergency landing as a tire just fell off the plane shortly after take-off. According to the latest reports, the plane experienced hydraulic issues.

It is unclear whether these incidents are more examples of Boeing’s reliability issues, and it is, therefore, way too early to blame Boeing for them. However, they do add to the company’s damaged reputation as problems and incidents continue to mount.

These problems are leading to problems for its customers. The Alaska Airlines incident at the start of the year, which can be 100% attributed to Boeing reliability issues, is having significant long-term consequences for the company, as customers are now experiencing significant delays in the delivery of Boeing planes – the company is having trouble with snowballing quality control issues, a slow ramp-up of production, and scrutiny in the certification of new aircraft which is now running years behind schedule.

In response to these issues, United Airlines has asked Boeing to stop building 737 Max 10 jets as the company is weighing off its options and has placed orders with rival Airbus. “It’s impossible to say when Max 10 is going to get certified,” according to Scott Kirby, chief executive of United, which is why the company sees no other option than to move to Airbus to support its growth plans.

Obviously, this looks very bad for Boeing, as it is now practically losing customers. There is no way to diminish this. And yet, Boeing is not at too much risk. As U.S. Federal Trade Commission Chair Lina Khan explained, the company is just “too big to fail.” According to the U.S. official, the company has too much power and is too essential globally and to the U.S. government. As a result, the company can count on the U.S. government to bail it out if things really take a turn for the worse by awarding it billions in orders.

Still, whether it is worth your investment money is totally up to you. You can view this significant dip as a buying opportunity or recent developments as a huge red flag – we are still very much rating the company an “avoid.”

Is an equal-weight S&P500 ETF now superior?

That the S&P 500 is no longer one of the best-diversified options out there is no news. Most S&P 500 ETFs now have the majority of their allocation in technology stocks, with big tech taking up a massive part. Take the most popular ETF - Vanguard’s VOO – which has the top 4 stocks now accounting for over 21% of its allocation and the top 10 for over 30%. Obviously, this is far from well-diversified…

Considering this, it is no surprise that the equal-weight S&P500 ETF is starting to outperform more regularly. The ETF already outperformed in the second half of 2022 and has done so once more this year, by 2.3 percentage points. For reference, this is the most significant outperformance in a rolling year… in history.

According to this post on Seeking Alpha, this can be attributed to two reasons: “One is the concentration of big tech in the market cap-weighted S&P. The other issue is that sector returns have been more concentrated in larger names over the last year.”

Clearly, if you are looking for a well-diversified ETF, the standard VOO or SPY might no longer be the best option.

Some other (similar) publications to check out

In closing of this post, we would like to give you all a couple of suggestions for Substack publications publishing similar content to ours, which we read regularly. Make sure to check these out!

Capitalist Letters - by

Thank you for reading this newsletter. Please remember that this is no financial or investment advice and is for educational and informative purposes only. We are simply sharing our views, actions, and opinions, which we hope will be insightful!

Please make sure to like, restack, and share this post to increase our reach and support our work. Thank you!

Disclosure: No recommendation or advice is being given as to whether any investment is suitable for a particular investor. The information provided in this analysis is for educational and informational purposes only. It is not intended as and should not be considered investment advice or a recommendation to buy or sell any security.

Investing in stocks and securities involves risks, and past performance is not indicative of future results. Readers are advised to conduct their own research before making any investment decisions.

These articles just keep getting better and better!

Appreciate the shout out man!