Micron Technology is a Potential Multi-Bagger by 2030 – I am Buying (A Deep Dive)

Structural technology tailwinds and industry shifts could make Micron a multi-bagger by the end of the decade under the right conditions. Micron is underappreciated by investors!

Micron is one of the more prominent names in the semiconductor space, regularly making headlines as one of the three giants in the memory chip market. Yet, it is everything but an investor favorite.

Why? Well, at the center of this problem are Micron's business model and the nature of the market it operates in. Unlike companies that design custom chips or focus on higher-margin, differentiated semiconductors, Micron is primarily a commodity producer, which isn’t quite what most investors tend to look for.

The company makes DRAM and NAND memory chips, which are essential to a wide range of devices but are largely undifferentiated. The result? Micron is more exposed to the cyclical booms and busts of the memory market than many of its semiconductor peers that focus on more lucrative verticals. When demand spikes—often due to macroeconomic shifts, new tech product launches, or supply shortages—Micron can do exceptionally well. However, when the cycle inevitably turns, pricing collapses and profitability vanishes just as quickly.

A number of quarters where revenue goes -30% to -50% YoY in a downcycle is nothing out of the ordinary here. Unsurprisingly, this isn’t something many long-term oriented investors like to see. This is why, until it finds a way to consistently escape the trap of commoditization—or until the market decides to revalue memory as a long-term growth asset (which it arguably should amid technological shifts)—Micron may continue to sit on the sidelines of many investor portfolios, visible but under-owned.

Micron is truly an investment for those with the stomach to withstand this kind of cyclicality. Honestly, that's why I have never seriously considered the company before – it just never quite seemed like a good long-term holding.

But… I might be very wrong.

While many skipped past this company due to its high cyclicality, Micron is a very high-quality business, with a strong market position and excellent long-term prospects, being at the core of some of the most powerful and durable technology trends shaping the future—particularly artificial intelligence, data center expansion, and intelligent edge computing. Meanwhile, the company is executing at a really high level and is fundamentally better positioned than ever before, whether technologically, operationally, or financially.

Therefore, I believe Micron is definitely worth a deeper look, as it might just be an underappreciated giant.

In this post, I will take you through all that a (potential) investor needs to know about this company.

This is my Micron deep dive. Let’s delve in!

This is Micron Technology!

Business model and fundamentals

Founded in 1978 and headquartered in Boise, Idaho, Micron Technology, Inc. is a leading American semiconductor company that designs and manufactures memory and storage solutions. Over recent decades, it has grown into one of the world’s largest memory manufacturers, competing closely with companies such as Samsung and SK Hynix.

Micron plays a crucial role in the global technology supply chain by producing DRAM (accounting for 70% of revenue) and NAND flash memory (accounting for 30% of revenue), which are utilized in a wide range of applications. These products power everything from personal computers and mobile devices to data centers, automotive systems, and artificial intelligence infrastructure.

In very simple terms, memory semiconductors are chips that store data. DRAM, or Dynamic Random Access Memory, is the type of memory your computer or smartphone uses while it's running—it's fast but temporary, meaning it loses all data when the power is off. NAND flash, on the other hand, is used for long-term storage, such as in SSDs or USB drives—it retains data even when the device is turned off. DRAM helps with quick access to data while you're using a program, and NAND stores your files, apps, and photos for long-term storage.

DRAM and NAND are essential to modern computing and become increasingly critical as digitalization accelerates, with the rise of more data, devices, and AI applications. DRAM keeps systems running smoothly by quickly feeding data to processors, making everything from web browsing to gaming feel fast. NAND is what allows your phone, laptop, and data centers to store huge amounts of information reliably. Without them, fast performance and high-capacity storage in today's devices wouldn't be possible.

Micron’s innovation on this front has helped drive the advancement of high-performance computing, enabling faster data processing and more efficient storage. Through ongoing investment in R&D, it is at the forefront of next-generation memory technologies, including high-bandwidth memory (HBM) and 3D NAND. As a result, the company has strategically positioned itself to benefit from long-term trends in cloud computing, AI, and edge computing, which are expected to sustain strong demand for advanced memory and storage products.

Furthermore, after decades of research and development and significant investments, Micron has grown into a top-tier player and one of the leaders in the memory market, operating as an oligopoly alongside its larger peers, Samsung and SK Hynix. The company is a solid third in DRAM, competing in the top four for NAND, and aggressively expanding in the high-value HBM segment.

Starting with DRAM, Micron’s largest market, the company currently captures a commanding market share of approximately 25%, according to Q1 2025 data from Counterpoint Research, trailing industry leaders SK Hynix and Samsung, which both capture mid-30s market shares.

Crucially, Micron is performing exceptionally well in the DRAM market, gaining significant market share. Its share was in the low teens at the start of the previous decade, grew to the low 20s in early 2024, and increased to the mid-20s in the most recent quarter, showing healthy market share gains, mainly at the expense of Samsung.

Fueling these DRAM market share gains are a number of factors:

Micron was among the first to commercialize DDR5 and LPDDR5X, which are crucial and advanced technologies for AI, PC, and mobile applications. These high-performance, low-power chips positioned it well with hyperscalers and mobile OEMs, which are increasingly important markets, growing as a share of the total DRAM market.

Node leadership: Micron was the first to mass-produce 1αnm DRAM (2021) and first to volume-produce 1βnm DRAM (2023), ahead of Samsung and SK Hynix. Through 1αnm and 1βnm process nodes, Micron has aggressively reduced cost-per-bit, making it highly competitive with Samsung and SK Hynix.

Micron has been highly focused on several high-margin and fast-growing markets, where it holds a substantially higher market share. These include AI servers, automotive (LPDDR for ADAS), and industrial/edge computing—less cyclical markets than consumer PCs or smartphones. As these markets outgrow the broader DRAM market, so does Micron’s market share.

Finally, Micron is often on par with—or even ahead of—SK Hynix and Samsung in process technology, making it highly competitive.

In other words, Micron’s technological edge has helped it gain market share in DRAM, and it continues to do so.

Meanwhile, in NAND, the company is not doing as well. The most recent data indicates that Micron holds a low-double-digit market share (11-12%), which is significantly lower than its peers, Samsung (high thirties) and SK Hynix (low twenties), and also lags behind Kioxia (mid teens). Furthermore, this is down from a mid-teens market share in 2019, indicating Micron is losing some grip on this market.

Again, there are a number of factors that contribute:

Samsung, SK Hynix, and Kioxia have aggressively cut NAND prices during downturns in recent years. Micron, focused more on margin discipline, didn't chase volume at the same pace, sacrificing some share.

Samsung dominates NAND with massive capacity and deep customer ties. Micron, while technologically competitive, lacks the same level of vertical integration or ecosystem reach.

Much of NAND demand growth has been driven by mobile and China-related areas, where Micron has less scale or political leverage (e.g., limited ties to Chinese handset makers compared to Samsung or YMTC).

3D NAND layer count: While Micron is advancing its 232-layer NAND, Samsung is already pushing 236 layers and working toward 290 layers or more. Samsung and SK Hynix also have superior controller integration and storage solutions (e.g., for smartphones and data centers). So, it’s also trailing technologically.

These factors have complicated the market for Micron, and it doesn’t seem to be improving anytime soon, as Micron continues to trail due to several fundamental factors that are difficult to overcome.

However, we are yet to come to its most promising product vertical, HBM, or High Bandwidth Memory.

For reference, HBM is a special type of memory designed to move data much faster than traditional DRAM. It’s stacked vertically and placed very close to the processor, which shortens the distance data has to travel and allows for much higher speeds with lower power use. This makes it ideal for demanding tasks such as AI, graphics rendering, and data center workloads, where massive amounts of data need to be moved quickly. As computing gets more complex and data-intensive, HBM is becoming more important for powering high-performance systems efficiently.

Yes, HBM is practically the memory backbone of AI. Without it, chips like NVIDIA's H100 or AMD's MI300 wouldn’t be able to process data fast enough.

Obviously, this makes it an extremely promising market, given the growing need for advanced computing and the rise of AI.

Interestingly, Micron was somewhat late to the HBM market compared to SK Hynix and Samsung. While those companies had years of HBM2/HBM2E production experience (serving AMD, NVIDIA, etc.), Micron only ramped HBM seriously in 2023 with HBM3 and, more recently, HBM3E and HBM4. It chose to do so for a number of reasons.

First of all, unlike SK Hynix and Samsung, which had early investments and customer pipelines in place, Micron made a calculated decision to prioritize other product segments—particularly standard DRAM and NAND—before aggressively shifting into HBM once the AI boom took off.

While Samsung and SK Hynix had strong relationships with companies like AMD and Nvidia, Micron didn’t have as many early design wins in these areas, making it harder to justify the massive capital needed for HBM ramp-up, especially during the early stages of the technology.

Instead, Micron waited until demand was clearly ramping—as seen in the explosive growth in AI training and inference workloads around 2022–2023—before committing to a major HBM investment.

Since then, Micron has entered the market with extreme success, claiming that its HBM3E product offers up to 50% better power efficiency and 2.5 times higher capacity per stack than any peer, which is precisely why the company has already fully sold out its 2025 production capacity. Micron currently ships the product to only a handful of high-end customers, including AMD, for whom the product is a key component in its highest-end products.

Meanwhile, Micron has also recently released its HBM4 model, which plays even better into the needs of AI workloads and growing complexity. HBM4 leverages Micron’s well-established 1-beta DRAM technology along with an internally developed and manufactured advanced CMOS logic base die to deliver bandwidth exceeding two terabytes per second per memory stack, over 60% higher performance than the previous generation. Additionally, it offers a 20% lower power consumption compared to its already industry-leading HBM3E product.

Clearly, technologically, Micron now leads the HBM market, with limited capacity being the only factor holding it back. This technological edge is enabling it to capture market share at an unprecedented rate. Today, the company still trails its close peers, SK Hynix and Samsung, but it’s rapidly gaining. As of the end of 2024, the company held a 9-10% HBM market share; however, management is confident that this will increase to 20-25% by the end of 2025, as more capacity comes online and customers are eager for Micron’s best-in-class products.

At this rate, Micron is poised to quickly become the leader in HBM, which positions it excellently for long-term growth and market share gains.

Long story short, Micron appears to be very well-positioned for the future and highly competitive in its respective markets.

In-house manufacturing and geographical exposure

A critical component in any Micron investment thesis is its in-house manufacturing capabilities. You see, within the semiconductor industry, many companies (like AMD, Nvidia, Broadcom, Apple, etc.) opt to outsource the actual manufacturing of components to external foundry partners, such as TSMC, GlobalFoundries, Samsung, or Intel. Although this creates some level of flexibility and a more capital-light business model, it also comes with a significant dependency on external technologies and capacity, which isn’t ideal.

However, Micron has a different approach, similar to that of many analog semiconductor providers, such as Texas Instruments or Infineon.

Micron manufactures virtually all of its memory and storage products in-house through its own fabrication facilities. It operates as an integrated device manufacturer (IDM), meaning it controls the entire production chain—from process development and wafer fabrication to packaging and testing—without relying on external foundries.

Its manufacturing footprint spans multiple continents, with leading-edge DRAM fabs in the United States, NAND operations in Asia, and assembly and test facilities in countries such as Malaysia and Singapore.

This in-house manufacturing is a massive competitive advantage and should be a big plus for investors. You see, this in-house model provides several strategic advantages, such as faster time-to-market for new nodes, better cost control through process optimization, tight control over its process technologies, yield management, and supply chain.

In other words, it gives it greater control over the entire process, which also allows it to tailor its products for specific customer requirements, such as high-temperature tolerance for automotive DRAM or energy efficiency for AI-centric HBM.

However, most importantly, this makes the company highly independent, with minimal reliance on external partners to sustain its manufacturing operations, which is brilliant, especially in an increasingly uncertain geopolitical landscape.

Additionally, in a time when domestic semiconductor production capacity becomes increasingly important, Micron is well-positioned, with significant production capabilities in the U.S. and minimal reliance on more unstable regions, such as China. For reference, considering the significant investments Micron is currently making in the U.S., it is anticipated to be able to manufacture 40% of its DRAM products domestically, significantly de-risking its business.

Micron recently announced plans to invest roughly $200 billion in the U.S., “which includes $150 billion in manufacturing and $50 billion in R&D over the next 20-plus years. As part of this $200 billion investment plan, Micron plans to invest an additional $30 billion beyond previously announced plans, which includes building a second leading- edge memory fab in Boise, Idaho; expanding and modernizing its existing fab in Manassas, Virginia; and bringing advanced packaging capabilities to the U.S. to support its long-term HBM growth plans after it has established sufficient DRAM wafer scale in its U.S. operations,” to quote management.

Indeed, Micron is betting big on the U.S. for manufacturing, which I quite like. This geographic diversification—paired with ownership of the production infrastructure—helps reduce vulnerability to regional disruptions, export restrictions, and capacity shortages that can derail foundry-reliant businesses. It also allows Micron to align more easily with national policy goals, such as U.S. CHIPS Act incentives for domestic semiconductor production, which helps offset CapEx and improve strategic positioning.

Additionally, from a customer perspective, Micron’s in-house manufacturing provides greater quality assurance and customization capabilities.

This all gives the company a significant edge, and this is an approach I tend to favor.

Meanwhile, the company has also achieved good revenue diversification. Micron derives roughly 50% of its revenues from the U.S., followed by the Asia Pacific (excluding China) at 25%, China at 15%, and other regions, including Europe, which contribute the remaining 10%.

Once again, this excellent diversification limits regional risks, especially with limited exposure to China and a big presence in the U.S.

These are all significant positives in my book, as they limit risk and give the company an edge.

The issue of cyclicality

Yet, while diversification, in-house manufacturing, and market share gains are great, there is a significant negative to discuss: the incredible cyclicality to which Micron is exposed.

Crucially, Micron’s business is inherently cyclical, closely tied to the fluctuations of the semiconductor industry and global demand for computing power.

Micron is primarily a commodity producer. It makes DRAM and NAND memory chips, which are essential to a wide range of devices but are largely undifferentiated.

When demand spikes, Micron can do exceptionally well. However, when the cycle inevitably turns, pricing collapses and profitability vanishes just as quickly, bringing down revenues and profits at a mind-blowing rate.

Another challenge lies in the perception of pricing power—or the lack thereof. Companies like Nvidia and AMD, which produce highly specialized chips, can command premium prices and generate strong gross margins. Micron, on the other hand, operates in a fiercely competitive market where price is often the only real lever. This creates thin margins during down cycles, when demand is low, and makes the company seem like a poor long-term compounder in the eyes of many investors who prioritize consistent free cash flow and expanding returns on capital.

Micron’s strategy now is to reduce cyclicality by focusing more on:

AI-driven memory (HBM, DDR5),

Automotive and industrial over consumer electronics,

Cost leadership and disciplined Capex.

But until memory becomes more customized and less commoditized, cyclicality is baked into the business model, and this is a massive pain in the ass for plenty of us.

However, this doesn’t mean Micron isn’t a compelling long-term investment, as long as you're comfortable with volatility and take a thesis-driven view on the long-term importance of memory in the digital economy.

You see, there are positive developments that could very well moderate some of these cyclical swings. For example, investments in AI, cloud, and edge computing are far less exposed to fluctuations in consumer spending or economic health, and this is becoming an increasingly significant portion of the market. This should, therefore, reduce cyclicality, especially for Micron, which has an outsized exposure to these markets.

In relation to this, HBM demand is expected to explode due to AI workloads, which should offset demand headwinds elsewhere in the coming years. Let’s not forget: the AI revolution is not a temporary tailwind: AI inference/training workloads will continue to scale, and every GPU/TPU needs more HBM per chip. If you believe AI isn't a fad, Micron is a strategic enabler.

This presents a significantly more promising outlook compared to the last decade for the company, which has achieved only a 6% CAGR through the cycles and experienced minimal net earnings growth. Yet, the future looks better than ever.

So, before we get to the more detailed market outlook, what is the ideal Micron investor?

Have a 5–10 year horizon.

Be valuation-conscious (buy when share prices are depressed due to cyclical pressures or when the upcycle is not priced in yet)

Understand semicap and memory dynamics.

Be able to handle 30–50% drawdowns without panic selling (most important – a stomach for volatility).

If you don’t possess these abilities, this will be a hard sell, no matter what. This one definitely isn’t for everyone… This isn't a stable compounder, as I prefer them.

Organic market growth

Alright, let’s take a look at the dynamics in Micron’s underlying markets, as far as I haven’t touched on those already. Ultimately, this will give us the best sense of what kind of growth to expect from Micron through the cycles.

Starting with the DRAM market (which includes HBM), it’s the rising complexity and intensity of computing workloads, particularly in artificial intelligence, data center infrastructure, and automotive systems, that drive growth.

AI applications are likely to be the main driver of growth in the DRAM market, as large language models and machine learning systems require vast memory bandwidth and low-latency access. This has already led to a surge in demand for high-performance DRAM, such as DDR5, GDDR6, and high-bandwidth memory (HBM), all of which support the data throughput required to train and run increasingly complex models. Because AI servers require significantly more memory per compute node than traditional workloads, the DRAM content per server is increasing rapidly, with an expected 15%+ CAGR. This structural increase in memory per unit of compute is a key driver of long-term demand for DRAM (HMB).

Probably the second-largest driver of growth for DRAM is the rise of electric vehicles and autonomous driving systems, which is fueling automotive DRAM demand. Modern cars require memory for a range of compute-intensive functions, including advanced driver-assistance systems (ADAS), in-car entertainment, real-time sensor fusion, and over-the-air updates. As cars become more software-defined, DRAM content per vehicle is expected to more than double over the next five years, with room to triple under the right demand and economic circumstances.

Additionally, the consumer electronics market also remains a growth driver, despite its maturity, driven by the incorporation of more LPDDR5X memory to support multitasking, AI camera features, and enhanced user interfaces in smartphones or creative, productivity, and edge AI workloads in PCs.

As a result, even though the total number of smartphones and PCs shipped globally may be flat or modestly declining, the average memory per device is increasing steadily, still providing the DRAM market with growth.

All these factors considered, market research firms estimate a medium-term high-single-digit CAGR for the DRAM market through 2035, incorporating very strong growth in the years ahead due to a recovering electronics market and AI-related demand and pricing.

Moving to NAND, the market outlook is very similar. This is another industry benefiting from secular trends.

Take data center growth. NAND flash storage enables the high-speed, low-latency access required for modern workloads, such as real-time analytics, AI data pipelines, and content delivery. Hyperscalers are deploying NVMe SSDs with PCIe Gen 4 and Gen 5 interfaces to handle increasing I/O demands, driving significant NAND bit growth despite volatile pricing.

Meanwhile, in mobile devices, the average amount of NAND storage per smartphone is increasing rapidly. As users generate and store higher-resolution photos, videos, and applications, flagship phones now regularly ship with 256 GB or more of NAND storage, and mid-range models are quickly catching up. Additionally, the shift to on-device AI processing—requiring large local models—adds another layer of storage demand, though this is also increasingly stored using the cloud.

As a result of an increasing number of cloud storage providers, the outlook for this market is slightly less optimistic, though still healthy. This market should see a more gradual recovery in 2025 and 2026 compared to DRAM, due to lower AI/datacenter demand, and beyond, market research firms point to a mid-single digit CAGR, though with falling margins due to pricing pressures.

Ultimately, we can say that the memory market as a whole should be able to grow at a CAGR of roughly mid-to-high-single digits through the end of the decade, with growth underpinned by long-term digital trends, including AI, cloud computing, smart devices, and the proliferation of edge intelligence. While prices fluctuate, bit demand is growing at double-digit rates in many end markets, which is an optimistic backdrop.

This presents a solid foundation for Micron to work with, especially with its outsized exposure to DRAM and HBM. Additionally, with Micron gaining market share and its favorable positioning toward these secular AI and cloud computing trends, I expect the company to be able to realize a healthy and very solid high-single-digit to low-double-digit CAGR through the cycles, which is the best outlook in the company’s history.

Secular trends are simply working in its favor. They are undeniable.

Does Micron have a moat?

Alright, before we move to the next section of this analysis, the recent performance and financials, there is one question left to answer: Does Micron have a moat/competitive advantage?

The answer is yes, but it is somewhat narrow and a real economic moat, built primarily on scale, technology leadership, and high barriers to entry—but it is not as deep or durable as moats seen in software or branded consumer businesses.

In the memory industry, competitive advantages tend to be earned through execution and capital commitment rather than regulatory protection or customer lock-in. That makes Micron’s moat situational and cyclical, but not nonexistent.

Most importantly, there is manufacturing scale. It is one of only three companies in the world—alongside Samsung and SK Hynix—that can produce DRAM and HBM at leading-edge nodes and at commercial scale. The cost, time, and expertise required to build and operate a modern memory fab are immense, often exceeding $10 billion per facility. This creates extremely high barriers to entry, especially as memory technology becomes more vertically integrated and process-intensive.

As a result, the risk of disruption is remarkably low – one can safely assume Micron is still one of the leading three in a decade or two.

Additionally, it has a significant technological advantage in deep process technology, particularly in DRAM. It was first to market with the 1α and 1β nanometer nodes, giving it a cost-per-bit and energy efficiency advantage in critical segments like mobile, AI, and data center computing. Its entrance into HBM with a best-in-class HBM3E and HBM4 products demonstrates that it can close competitive gaps and even out-execute its peers in some high-value niches. This type of node leadership is challenging to replicate and typically requires years of sustained R&D, access to EUV lithography, and robust yield-management capabilities.

Again, high barriers to entry.

However, beyond this, there isn’t much more that gives it a considerable moat. It lacks strong brand loyalty, recurring subscription models, and network effects. Memory is still a commodity-like business in many respects. Customers can and do switch suppliers based on price, availability, or node competitiveness.

Nevertheless, I believe it has a sufficient moat to please investors. As long as it executes—and competitors do not significantly outspend or out-innovate—it can defend its economic position.

Micron is firing on all cylinders

Micron released its most recent financial results in late June, delivering surprisingly strong results that exceeded both analyst and management expectations. Driven by excellent execution, Micron delivered record quarterly revenues that exceeded the high end of management’s guidance, as did the gross margin and EPS.

After going through a very rough downcycle in fiscal 2022 and 2023, when revenues declined by as much as 57% YoY, as visible in the graph below, Micron has seen revenues recover very strongly in 2024 and so far in 2025.

This rapid recovery is fueled by rapid growth in most of Micron’s end markets. Firstly, Micron’s consumer-oriented markets, which primarily refer to consumer electronics, have experienced rapid sequential growth in recent quarters as inventories have normalized and appear healthier, and demand has improved amid healthy consumer spending trends and confidence.

Additionally, Micron is fully benefiting from incredible data center-related revenue, which is becoming a considerable growth driver for Micron. In Q3, data center revenue more than doubled YoY to record levels.

Driven by these dynamics, Micron reported fiscal Q3 revenue of $9.3 billion, up 15% sequentially and 37% YoY, well exceeding the $8.85 billion Wall Street consensus. This shows a strong continued recovery.

Splitting revenue by product category, Q3 DRAM revenue was $7.1 billion, up 51% YoY and now representing 76% of total revenue. Sequentially, DRAM revenue was up 15% YoY, driven by a 20% increase in bit shipments and a low-single-digit price decrease, which was the result of a higher consumer-oriented mix as these lower-priced markets recover.

Nevertheless, these were record-high DRAM revenues for a fourth consecutive quarter, driven by a whopping 50% sequential growth in HBM revenue. This performance was aided by several product milestones, including the first qualification sample shipments of 1-gamma based LP5 DRAM, which achieves a 30% improvement in bit density over previous generations, as well as 20% lower power consumption and a 15% increase in performance.

Thanks to these technological advancements, Micron remains the leader in HBM technology, allowing it to gain market share and report rapid growth.

Meanwhile, the NAND recovery is much slower. Q2 NAND revenue was $2.2 billion, up 4% YoY and now representing just 23% of Micron’s total revenue. Sequentially, revenue was up 16% YoY, driven by a 20% increase in bit shipments, offset by a high single-digit drop in prices.

A recovery here is proving to be much slower and gradual, in contrast to the explosive growth we see in the DRAM market, which can be mainly attributed to a higher exposure to consumer electronics and a far lower exposure to the rapid growth in data centers.

Nevertheless, Micron is gaining some market share. It has moved up to the #2 spot in the data center SSD market.

Moving to the bottom line, Micron also continues to show a rapid recovery, with rapid top-line growth amid improving demand fueling impressive margin improvement.

Starting with the gross margin, this one turned negative during 2023, reaching a low in Q2 2023, but recovered rapidly since, reaching 39% in Q3, up almost 11 percentage points YoY and surpassing management’s guidance by 250 bps. This was fueled by better-than-expected prices for both DRAM and NAND, partially offset by a higher consumer-oriented mix.

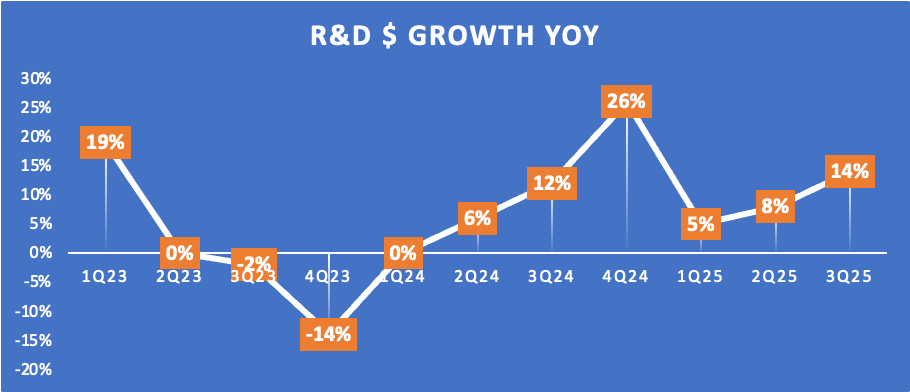

Further down the line, Q3 operating expenses were $1.34 billion, in line with guidance and up 20% YoY. This YoY increase was mainly driven by healthy growth of 14% YoY in R&D expenses, which now accounts for 54% of total operating expenses. As shown below, Micron’s R&D expenses continue to grow throughout the cycle. On the one hand, this puts additional pressure on margins during a down cycle, but it also allows Micron to continue investing in its technologies, which enables it to maintain its edge.

In this market, this is crucial – Micron management realizes this all too well and remains committed to these investments.

Nevertheless, with costs growing slower than revenue in Q3, the operating income grew strongly to $2.5 billion, reflecting an operating margin of 26.8%, up a whopping 13 percentage points YoY.

These strong margin gains also translate into rapid EPS growth of over 200% YoY and 22% sequentially to $1.91, coming in nicely ahead of guidance and blowing past a $1.61 consensus.

Turning to FCF, despite considerable investments in long-term growth, with Micron investing a whopping $2.7 billion in Capex in Q3, it still generated $1.9 billion in FCF, which is the highest quarterly amount in over six years. This is a great performance!

Furthermore, this also allowed management to further strengthen its balance sheet. As of the end of the quarter, Micron held a record $12.2 billion in cash and investments, as well as $3.5 billion under its untapped credit facility, bringing its total liquidity to $15.7 billion.

On the other side of the equation, there is also $15.5 billion in debt on the balance sheet; however, after refinancing $900 million in 2027 notes last quarter, the weighted average debt maturity is 2032.

In other words, the company remains in excellent financial health, with ample liquidity.

Alright, before moving to the outlook, let’s finally shed some light on its reinvestment numbers, which are hard to read into. Here are Micron’s ROE and ROIC numbers:

So, what should we conclude from these numbers?

First, the numbers clearly reflect Micron’s cyclicality. During boom periods, ROE and ROIC exceeded 30–40%, indicating highly efficient capital utilization and long-term investments yielding substantial returns. However, downturns in 2016 and 2023 substantially eroded returns. As a result, the numbers are difficult to interpret on a yearly or even multi-year basis.

Examining the numbers over multiple cycles and a longer-term period, I believe the most important takeaway is that Micron can generate exceptional returns during peak cycles. The recent moves—such as capex discipline, high-margin memory focus, and strengthened balance sheet—are helping to stabilize performance and rebuild return profiles in the current upcycle.

I believe these numbers are as good as can be, with ROIC most often remaining well above WACC, suggesting solid value creation.

Before we move on, just a quick word…

Want more out of your subscription? Even more content like this on a weekly basis?

InvestInsights PRO - $7.50/month ($70/annually)

An additional 2-5 premium stock analysis monthly.

Full insight into my own portfolio (15% return CAGR since 2022).

Monthly portfolio updates + Instant transaction alerts (Fully transparent)

A complete overview of all my target prices and ratings (Excel file).

Exclusive access to the PRO subscribers Discord channel

Instant access to earlier premium analysis on, for example, Adobe, Thermo Fisher, Spotify, and The Trade Desk.

Outlook & Valuation

So far, I have already touched on Micron’s outlook slightly. As pointed out before, I believe it is safe to assume that Micron will deliver a low-double-digit revenue CAGR through the cycles, driven by strong growth in the DRAM and NAND markets, as well as Micron gaining market share thanks to its favorable positioning in higher-margin and faster-growing markets.

Looking a bit more short-term, Micron management guides for a continued recovery in revenues. Management now guides for record fiscal Q4 revenue of $10.7 billion, reflecting 15% sequential growth. This growth will be primarily driven by increases in DRAM revenues, supported by effective pricing execution, a favorable product mix, and continued cost improvements, all of which also benefit gross margins, expected to hit 42% in Q4.

Meanwhile, cost growth should remain controlled, which should allow for great operating and profit margin expansion, with management guiding for a Q4 EPS of $2.50 at the midpoint, reflecting a YoY increase of over 100%. Management expects to use these improved cash flows to invest heavily in HBM capacity, pointing to roughly $14 billion in fiscal 2025 capex, though FCF should remain quite strong.

In other words, management anticipates a strong recovery in the quarters ahead, driven by unprecedented demand for data centers and AI, as well as a rebound in consumer electronics. This should result in high-teens YoY growth in the DRAM industry in calendar year 2025 and low-double-digit growth in NAND. Furthermore, management anticipates mid-teens bit growth for both DRAM and NAND in the medium-term, which is a promising outlook.

Meanwhile, management also indicates that customer inventories are healthy across all end markets, and these continue to signal a constructive demand environment for the remainder of this calendar year, which is a very positive backdrop for Micron.

Ultimately, considering all factors and management’s Q4 guidance, I expect Micron to deliver 48% revenue growth in fiscal year 2025 and an EPS of $7.90, which is slightly ahead of management’s current guidance, as I deem this estimate slightly conservative given the underlying dynamics.

Beyond that, I expect Micron’s revenue and EPS growth numbers to moderate but remain very strong amid a gradually recovering consumer market and incredible AI-related demand for DRAM and HBM products, where I expect Micron to fully benefit. Considering the current dynamics, we are well-positioned for a strong upcycle as a result.

Considering the company’s prospects even further in the long term, as I mentioned, I anticipate a low-double-digit revenue CAGR and roughly similar EPS growth.

Here are my full medium-term projections.

Moving to valuation, critically, Micron’s turnaround and great medium-term prospects haven’t gone unnoticed. Micron shares are up 48% YTD and have rallied by almost 100% since they set a 12-month low in April amid peak tariff uncertainty. Yet, at the same time, shares are still down 5% over the last 12 months.

More importantly, the valuation still appears somewhat moderate, with shares trading at 16 times this year’s earnings and 10 times next fiscal year’s earnings, which appears far from expensive considering its great outlook. Yet, for Micron, this is a bit more complicated due to its cyclical dependence.

With Micron shares’ fair multiples fluctuating heavily depending on the cycle timing, what is actually a fair multiple?

At cyclical troughs, when memory prices are depressed and the earnings outlook is weak, the forward P/E multiple can collapse to around 5–6x. For instance, in mid-2017 and early 2018, forward P/E dipped to roughly 5x. During the 2022–2023 downturn, similar levels resurfaced before the company returned to profitability. At the same time, during cycle peaks, such as the 2021 memory boom, Micron's forward P/E has widened considerably, occasionally reaching 12–15 times or even the high teens.

Crucially, since it appears we are still very early in a strong upcycle, considering the likely impact from AI and a push for advanced computing, Micron definitely deserves to trade at the higher end of its historical multiple range. Arguably, the company’s medium-to-long-term future had never looked better.

For reference, we are looking at a 3-year PEG of 0.4x, which is very hard to make sense of.

Therefore, I don’t mind paying a mid-teens earnings multiple at all, and I consider a low-double-digit earnings multiple or a 0.4x PEG based on the next fiscal year to be relatively cheap. This appears to be excellent value to me, considering the company is poised for rapid growth in the medium term and is executing at a very high level.

For reference, even if we assume a conservative 12x medium-term earnings multiple, which still reflects very low and conservative growth expectations and sits well below its 10-year average of 19x, I calculate an end-of-fiscal FY27 target price of $189. From a current share price of $125, this reflects annualized returns of 16%(!), which is nothing short of great.

And, once again, this is based on a very conservative multiple assumption. In reality, I believe that assuming a 15-16x multiple is still more than fair, which would balloon annualized returns to 28%, representing brilliant returns.

After conducting 6,000 words of research, is Micron a good buy today for long-term investors?

My answer is yes, for those who can stomach the potential volatility. However, beyond the high level of cyclicality, Micron looks brilliantly positioned for the future – I really like its long-term prospects.

And with shares still far from expensive, with forward growth still not fully priced in, even as the share price has doubled from their April lows, I believe now is still a good time to pick up some shares and build a position.

Considering its structural tailwinds, I believe Micron, at current levels, could be a multi-bagger by the end of the decade under the right conditions, but it also requires the right investor…