PayPal vs Apple Pay – What Apple’s WWDC announcements mean for PayPal (It isn’t great)

PayPal shares have underperformed once more over recent weeks after Apple introduced exciting new features for its Apple Pay payment service. Let's see what this means for PayPal.

While PayPal PYPL 0.00%↑ shares gained an excellent 7.5% after it reported Q1 earnings a couple of weeks ago, shares have quickly given up those gains over the last two weeks or so, losing 12% in a relatively short time span. As a result, shares are now down 2.5% YTD, significantly underperforming the SPY, which gained 15% so far this year.

And it’s not like PayPal shareholders haven’t had enough misery over the last couple of years, either. Shares are down a whopping 50% over the last five years, making it one of the poorest performers among its large-cap technology and FinTech peers.

I covered PayPal in depth very recently—you can check that post out through the button below—and I actually rated shares a “Buy” even though I had some serious concerns about PayPal’s ability to fight off the competition.

However, there were also plenty of positives to build on, like a new promising CEO, a shift to focus on SMB customers, and several innovative payment solutions to improve user convenience and the platform’s attractiveness. This is what I wrote:

“Crucially, Chriss’ and the management team’s efforts so far have given me some confidence that they will be able to steer this business in the right direction and remain a go-to platform for both consumers and businesses in the financial sector, something I didn’t expect to say halfway through my research.

Suppose PayPal can maintain at least most of its market share and strengthen its foothold in certain business areas, such as small and medium-sized businesses. In that case, it should be a significant beneficiary of the projected growth in the underlying digital payment processing industry, which is very much looking bullish!

Based on my current, slightly conservative (as I want to leave some margin of safety here) expectations and projections, I expect PayPal to report medium-term top-line growth at a CAGR of high single to low double digits, depending on its execution success and timeline. It surely has potential.”

At a bottom valuation, there was plenty of room for positivity in my view, and even as risks remained relatively high, shares seemed pretty de-risked based on growth potential and current valuation levels. I mean, a PEG of 1.25 and P/E of 15x is very much looking compelling.

And yet, shares are down a further 4% since this post, as is my own position I initiated earlier this month. Now, don’t get me wrong here; I am in it for the long term, and I am absolutely not worried about this short-term share price pressure.

However, the cause of this share price weakness is essential to consider, as most of the recent pressure on shares comes from the new Apple Pay features introduced at the WWDC event, causing additional concerns about PayPal’s ability to fight off Apple.

Let’s dive in!

On a side note, if you haven’t done so already, also make sure to check out our post on LVMH, which we published mid-week for paid subs! It definitely is an interesting read, as this quality compounder is starting to become more attractively priced.

PayPal has no answer to the rise of Apple Pay

You see, PayPal has been struggling significantly with competition over recent years. I know it might not seem that way, considering the company still holds roughly 45% of the digital payment processing market, but there is no denying PayPal has been losing its grip on the market.

Without repeating too much from my previous post, PayPal has seen its market share trend down in recent years, especially as it has been facing significant competition in e-commerce checkout and P2P transactions, particularly from Apple’s Apple Pay, which has been taking over the digital payments industry.

With Apple Pay, Apple users can make in-store and online purchases with their iPhone, among many other smaller and upcoming features. This allows Apple to compete with PayPal, Block, and Stripe in digital payment processing and digital wallets.

However, Apple has been blowing the competition out of the water in recent years, primarily thanks to the incredible convenience and seamless integration offered by the Apple Pay platform to Apple users – Apple Pay is by far the most convenient solution for Apple users.

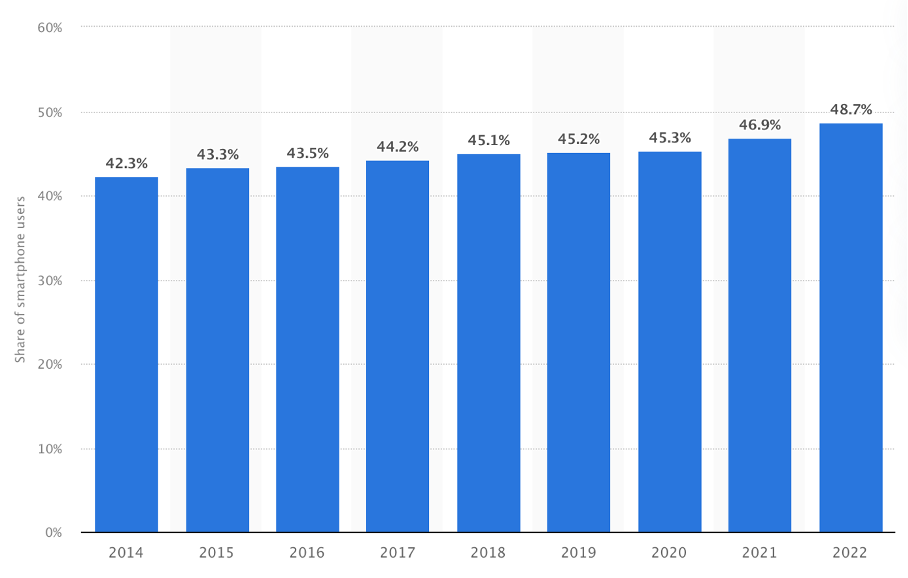

In addition, while PayPal has been dealing with consumer trust and security concerns, Apple’s dedication to privacy and security has enhanced its trustworthiness, giving it an additional edge. And with iPhone adoption still growing, now at roughly 49% in the U.S. and hitting 1.46 billion active users globally, Apple isn’t particularly targeting a small target audience.

As a result, data from investment firm Mizuho indicates that PayPal has been losing significant market share against Apple and is struggling to compete. Apple is rapidly gaining share, especially in e-commerce checkout, which has been one of PayPal’s strongest selling points.

Over recent years, Apple has taken over this industry, more than doubling its adoption rate, while PayPal has been stagnant. Apple has grown its user base to over 640 million, from 507 million in 2022. For reference, this represents a growth rate of 17%, which stands in sharp contrast with PayPal’s user losses.

In fact, 45.4 million Americans have used Apple Pay in the last month alone, and the service handles 1.8 billion transactions quarterly, which is pretty insane. Also, this number is up over 40% year over year. Compare this to user growth, and we can conclude that Apple Pay isn’t only rapidly growing its user base but is also seeing exploding growth in engagement. Let’s just say the service is firing on all cylinders and seems pretty unstoppable.

Supporting this is the staggering acceptance Apple Pay sees worldwide, which makes sense looking at user numbers—quite bluntly, merchants don’t really have a choice. As a result, more than 90% of US retailers and 60% of global retailers now accept Apple Pay. Also, 5,480 banks provided Apple Pay as of 2020, a number that also continues to grow pretty dramatically.

Obviously, this isn’t great for PayPal, especially as Apple Pay is getting increasingly more popular for online checkout, which used to be one of PayPal’s strongholds. In fact, it is and should be one of the most significant concerns for investors. PayPal’s moat is nowhere near where it used to be and far from the best payment solution out there.

As highlighted below, Apple continues to take market share rapidly.

And problems keep mounting for PayPal as it gets out-innovated by its competitors, which brings me to Apple’s WWDC event, which further raises concerns for PayPal investors as Apple is looking to strengthen its grip on the digital payments industry.

Apple introduces exciting new Pay features

At its WWDC event earlier this month, Apple announced a slew of new features for its Apple Pay payment platform, including Apple Pay Online, Tap-To-Cash, and an expansion of its BNPL offering. These features caused some slight panic among PayPal investors as they looked to challenge PayPal further.

Probably the most significant new feature, at least in my opinion, is the support of Apple Pay for online checkout in web browsers other than Safari, which significantly increases the usefulness of the service. Currently, Apple Pay for online checkout only works through Safari, but with iOS 18, iPhone users can also see an Apple Pay button in other browsers like Chrome, Firefox, or Edge.

For reference, Safari is used by only below 80% of Apple users and, in many cases, not as their primary browser. Therefore, adding Apple Pay support to other popular browsers significantly increases the availability of Apple Pay in online checkout, putting further pressure on PayPal and contributing to Apple’s takeover of this market.

Importantly, I do not view this as a reason to panic for PayPal investors, even as it does highlight Apple’s commitment to the payments industry. Innovations like these could add further pressure on PayPal’s checkout market share. In fact, they probably will have a slight impact once IOS 18 is out.

In addition to this compatibility update, Apple also introduced a brand new feature in Tap to Cash, which allows iPhone users to send Apple Cash to each other by simply holding their iPhones together. This makes it easy to pay someone back after dinner or buy something at a garage sale.

This marks Apple’s entry into the P2P transactions market, again competing with PayPal, particularly its Venmo payment service, once more putting pressure on it. Considering Apple’s success in entering certain parts of the payments industry, I can understand the investor panic after this announcement. Clearly, Apple has its eye on the P2P transactions market.

Positively, for now, Apple’s ability to compete with PayPal or Venmo is rather limited as it is only available for in-person payments. At the same time, Venmo allows you to complete transactions from anywhere in the U.S. Therefore, again, there is no reason to be overly worried. However, it will be important to monitor Apple’s advancements closely.

Conclusion, estimates, and valuation.

Overall, I view the recent share price decline in response to this announcement of Apple Pay innovations as overdone. While I do share the concerns as a PayPal shareholder and am far from happy with these latest moves from Apple, it doesn’t warrant the sell-off at current already de-risked levels.

Yes, I increasingly believe Apple could pose a significant threat to PayPal. I include this in my latest financial projections, which I will show in a bit, including some more online checkout market share losses—this is the most likely scenario right now. In the long term, Apple’s payment innovations increase worries over PayPal’s ability to compete.

Also, in addition to the increasing threat from Apple, two more factors weigh on PayPal’s shares that should be considered. For one, insider selling remains significant even as shares remain seemingly cheap. Notably, several large insiders have been lowering their stake by roughly 25% over the last year, which isn’t a great sign.

Second, Mastercard recently announced that by 2030, it aims for all its European card credentials to be tokenized, enhancing security for online transactions and making PayPal’s recently introduced and much-hyped Fastlane Service totally useless. While still far into the future, this has been weighing on PayPal, and it highlights how PayPal continues to struggle to differentiate itself.

My general conclusion from all this is that I have become somewhat more skeptical of PayPal, even though I covered the company as recently as one month ago. PayPal is struggling to compete and innovate sufficiently, which brings significant risks.

Therefore, I have slightly de-risked my long-term financial projections, resulting in the following.

You can see I have lowered my long-term estimates to account for some additional weakness and growing competition. Based on these estimates, PayPal shares now trade at 14.5x this year’s expected earnings and a PEG of 1.61. This puts PayPal’s PEG at a 50% premium to the sector median, though this is arguably deserved due to its higher projected growth and far higher FCF generation.

However, given current struggles, headwinds, and the chance of further market share losses, I wouldn’t be willing to pay a premium for this business. I believe a 15x earnings multiple is about fair, meaning shares aren’t far away from fair value. Based on this multiple and my FY26 estimate, I now calculate a target price of $80 per share, leaving investors with potential annual returns of just below 12%, which is sufficient to keep shares buy-rated for now, although I am not as big of a fan as I have been.

While, short-term, shares should be able to see some upside, in the long term, I am not as optimistic as PayPal could end up disappointing in the face of growing competition. From a risk-reward perspective, I am pretty neutral right now – shares remain high risk.

Though, for now, I do maintain my “Buy” rating.

I know this was a relatively short post, as we usually try to post a Deep Dive every Sunday. However, as I started a new job this week, I had limited time to write… sadly.

Positively, I am back on track now and will have a very exciting deep dive coming next week for all subscribers. Also, paid subs can expect another post mid-week.

Here are some of the companies we will cover in the coming weeks:

Celsius

First Solar

Crowdstrike

FedEx

Nike

Qualcomm

Just Eat

Also, let me give you some quick “must reads” from some of my favorite publications on Substack:

The post below is from

, who recently got featured in the Wall Street Journal. It dives into Apple’s newest AI integrations, approach, and what AI could mean for the company.- recently posted an interesting post, discussing 5 top stocks to consider today. It definitely is worth checking out as well!

Great write up Daan. I certainly share your concerns about Paypal's Moat and ability to fend off competitors. My fund holds a large position in Paypal, at least it was a large position before 2022. It is becoming increasingly difficult to look out 5-10 years and know for certain the type of moat and quality of earnings PayPal will have.

Thanks for the shoutout Daan, very kind of you.