Salesforce Looks Cheap Again: 14% CAGR Potential from a Blue-Chip Compounder

Despite slower AI adoption and macro concerns, this CRM leader may be one of the best-value plays in enterprise software right now, + my thoughts on the Informatica acquisition.

Last Wednesday, Salesforce released its fiscal FY26 Q1 results, which drew an adverse reaction from Wall Street, resulting in a 6% lower opening for the subsequent trading session on Thursday, even though the Salesforce report actually looked pretty good. The enterprise software and CRM leader delivered a top and bottom-line beat, although it only beat by a very slim margin. Additionally, the company raised its full-year guidance, reflecting confidence in the remainder of the year, despite macro headwinds.

In other words, Salesforce seems to have ticked all the boxes with its Q1 results. Yet, there are two minor points to note. For one, Salesforce’s good results in Q1 and the outlook raises are almost solely driven by currency tailwinds. Second, the company’s AI traction, despite being promising, remains slower than expected, which has diminished some of the earlier enthusiasm for the stock, especially amid near-term macroeconomic headwinds.

As a result, while Salesforce management was almost euphoric during the earnings call, once again singing its own praises and turning more positive on 2025, I, like the market, do not quite see it the same way amid near-term headwinds and a slow AI ramp-up. A much-needed and anticipated growth acceleration back to the double digits (which should justify its premium multiple) is unlikely in 2025 or 2026.

Additionally, Salesforce recently announced its acquisition of Informatica for $8 billion in cash, diverting from its commitment to shareholders to focus on organic growth, which has led to a mixed reaction, not adding to positive sentiment. On this front, I don’t entirely share this sentiment, even though I can see where the negativity comes from.

All things considered, the 6% share price drop post-earnings didn’t come out of nowhere. At the same time, on a positive note, this means Salesforce shares now trade 9% lower than when I last covered Salesforce back in March, dropping below my targeted buying range of $270 per share.

Additionally, in the long term, I view Salesforce as a promising business, thanks to its strong position in the CRM and broader enterprise software markets, and primarily due to the company’s impressive and innovative AI offerings, which could very well drive a new leg of growth well into the next decade.

Today, I want to take a close look at Salesforce’s Q1 report, discuss the details of the Informatica acquisition, and re-evaluate its long-term prospects and my financial projections.

Are Salesforce shares a good buy today at $265 per share, or should you aim for lower prices and a better margin of safety? Let’s find out!

The Informatica acquisition – A return to old habits?

Last week, Salesforce officially announced the acquisition of Informatica ($INFA), and I have to say I was negatively surprised by the news. Initially, as a shareholder, I was not too pleased. Let me explain!

While the deal makes a lot more sense compared to Salesforce’s past acquisitions, especially at the price point (which I’ll get to in a bit), Salesforce had earlier made a promise to investors to move away from its M&A fueled strategy and focus on organic growth and significantly improving its margin profile.

You see, over the past decade, Salesforce became known for its aggressive acquisition strategy—buying companies like Tableau, MuleSoft, and Slack for tens of billions of dollars. While some of these acquisitions added strategic value, they also came with high costs and integration challenges, and in many instances, massively diluted shareholders' interests. Also, the frequent large-scale acquisitions created distraction and complexity, making it harder for Salesforce to operate efficiently and realize the full value of what it already owned.

Investors started questioning whether Salesforce was spending too much on growth through acquisitions rather than improving its core business operations, which is why management promised to move away from this strategy in early 2023.

Yet, here is another $8 billion acquisition announced, just two years later. Despite its incredible bullish stance on AgentForce, which should drive a new leg of growth, does Salesforce feel the need to fuel growth and strengthen its offering through acquisitions?

Honestly, I feel like Salesforce’s strong core operations already looked good, especially in the AI agrents market. Spending another $8 billion on an acquisition, therefore, didn’t feel like the right direction.

However, after delving a bit deeper into the details of the acquisition and Informatica itself, I have turned more positive on the deal.

Getting into the details, Salesforce is acquiring the technology company for $25 per share, or approximately $8 billion, representing a roughly 30% price premium. The deal will be paid fully in cash, financed by the company’s existing cash reserves and new debt, thereby avoiding shareholder dilution.

So, just some first takeaways from these details. First, I must say that the deal value appears to be quite favorable. The deal was first rumored over a year ago, when a price of $11 billion to $12 billion was mentioned. Today, Salesforce is acquiring the company for $8 billion, at a 30% premium to the pre-deal share price, which isn’t bad at all. For once, Salesforce doesn’t seem to overpay, after not rushing into a deal.

Additionally, as a shareholder myself, I appreciate that management avoids diluting its shareholders. The company maintains a healthy balance sheet with a substantial cash position and manageable debt. Especially with the company generating over $12 billion in FCF a year, the price tag here should not be an issue at all. Management also sees no need to disrupt its capital return strategy (share repurchases program and dividend).

So far, so good.

So, what is Informatica?

Informatica is a leading data management company that specializes in enterprise data integration, data quality, data governance, master data management (MDM), and cloud data management. Its tools help organizations collect, clean, catalog, govern, and unify data across hybrid environments (on-premise, multi-cloud, SaaS).

Therefore, through the acquisition, Salesforce, which is already an Informatica customer itself, should gain deeper control over the entire data lifecycle, making its AI and analytics capabilities more powerful and accurate. With Salesforce heavily focused on its AI agent offering, higher-quality data, which Informatica specializes in, could be a game-changer.

Additionally, many enterprises use multiple cloud platforms and on-prem systems. Informatica's broad connectivity and hybrid cloud support help bring this fragmented data into Salesforce’s ecosystem, so Informatica's specialties do look like a good match for Salesforce’s massive collection of customer data and big AI push.

On some final notes, Salesforce expects the deal to close in early fiscal FY27, so in about a year’s time. Management expects the deal to achieve accretion in operating margin, EPS, and FCF by year 2 after closing, which is a positive outlook.

All in all, I believe the deal for Salesforce holds a lot of promise. While the acquisition goes against Salesforce's recent promises to limit M&A, strategically it enhances the core platform, especially in a world where “AI is only as good as your data.”

Most importantly, with this deal, Salesforce is not diluting shareholders or overpaying. It appears to be a relatively good deal overall and one that could significantly enhance Salesforce’s AI capabilities.

This deal is a net positive for shareholders, in my view, adding to Salesforce’s long-term AI prospects while not hurting shareholder value or the company’s balance sheet considerably in the near term.

However, I will add that I am not in favor of another acquisition spree by Salesforce management. This should remain a one-off.

Salesforce delivered a decent but unsurprising Q1 report

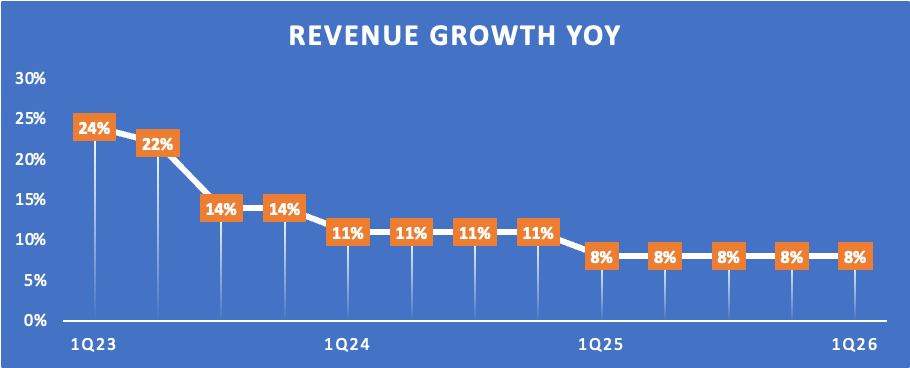

As I pointed out before, Salesforce delivered a good top and bottom line beat with its Q1 earnings report. The company reported quarterly revenue of $9.83 billion, up 8% YoY, which includes a one percentage point headwind from the leap year in 2024. As visible below, this is stable compared to recent quarters, with growth not slowing down further and remaining in the high single digits.

During the quarter, Salesforce saw strong growth in its small and medium market business, registering double-digit bookings growth, somewhat to management’s surprise. This was offset by slower growth in the enterprise customer base, as these customers seemed to show more caution. However, the demand dynamic is fluid, so I wouldn’t read into it too much.

More impressive were Salesforce’s RPO numbers. RPO hit $60.9 billion by the end of Q1, up 13% YoY, still outpacing revenue growth and showing healthy demand. Despite a somewhat cautious spending dynamic, Salesforce is still able to close large deals, driving RPO growth. This is also helped by a strong renewal rate, which led to 12% growth in cRPO.

These are still healthy numbers, largely driven by Salesforce’s multi-cloud strategy, particularly strong growth in its data cloud and AI applications, while its Sales and Service cloud continues to be the basis of Salesforce’s offering and appeal. Last quarter, 6 out of Salesforce’s top 10 deals included six clouds or more, while 80% of deals included both the Service and Sales cloud. While these legacy clouds no longer grow at a mighty rate due to the rule of large numbers, they continue to form the foundation of Salesforce’s enterprise IT offering, and with great customer satisfaction.

However, the real highlight remains its data cloud. Data cloud usage was up 175% YoY and was included in 60% of the top 100 deals, showing incredible adoption for the company’s data management and AI offering. This resulted in Data Cloud ARR growth of over 120% in Q1, tipping over the $1 billion threshold. To date, this is Salesforce’s fastest-growing product ever.

Notably, 50% of new Data Cloud deals came from existing customers, showing strong demand for these new features. At the same time, the adoption of Agentforce, the company’s flagship AI product, is still slightly slower than initially hoped, due to the technology and launch being in a very early phase, having been launched in late 2024. Also contributing to slower adoption is an evolving pricing strategy, which keeps some customers on the sidelines, and macroeconomic conditions that do not allow for even pricier IT investments at this time. Somewhat cautious IT budgets are slowing down adoption.

For reference, here is what I wrote about Agentforce back in March:

“In straightforward terms, Salesforce’s Agentforce is a more advanced version of the Copilot versions launched recently by Microsoft and Salesforce. Unlike traditional chatbots or copilots, these agents can operate independently, retrieving relevant data on demand, creating action plans for any task, and executing tasks without constant human intervention. In other words, it gets pretty close to a kind of digital employee to manage certain tasks, all driven by data.

Salesforce’s Agentforce allows customers to create a digital workforce. It can mimic human decision-making and cognitive abilities, making it a big step forward in terms of automated tasks.”

Positively, the Agentforce product continues to show great promise. Salesforce’s own sales agent in Slack has simplified everyday sales activity through automation, leading to 44,000 hours saved annually in manual effort. Additionally, lead routing has dropped from 20 minutes to 19 seconds. And finally, thanks to Agentforce handling 750,000 internal cases in customer support, Salesforce cut its case volume by 7% YoY. These reductions across departments have reduced Salesforce’s hiring needs, already realizing $50 million in annual savings through personnel reallocations alone.

Ultimately, even though the real ramp in adoption and growth might take a little longer, the promise of Agentforce remains considerable. I continue to believe in Agentforce as the driver of the next leg of growth for Salesforce, likely well into the next decade, as the AI use case really picks up. For me, this remains the primary driver of any Salesforce bull thesis.

Meanwhile, Salesforce also continues to deliver healthy margin improvements alongside this steady growth. In Q1, Salesforce reported an operating margin of 32.3%, up 20 bps YoY, resulting in an operating cash flow of $6.5 billion.

Since shifting its focus from growth to profitability in early 2023, under pressure from activist shareholders, Salesforce has delivered excellent margin expansion, which appears to be stabilizing in the low 30 percent range currently, due to higher investments into data cloud and AI offsetting tight cost management.

However, while the flattening isn’t ideal, I am glad to see margins hold up well, even expanding slowly amid a heightened investment cycle. Further down the line, this resulted in an EPS growth of only 4% year-over-year, although it still beat the consensus by $0.03.

Finally, although not entirely representative on a quarterly basis, Salesforce delivered very strong free cash flow (FCF) in Q1 of $6.3 billion, easily covering the $3 billion returned to shareholders in the quarter through repurchases and dividends.

This also allowed it to strengthen its balance sheet, now holding $17.5 billion in cash and short-term investments against $11 billion in debt, leaving Salesforce in excellent financial health with great liquidity.

All in all, I would say that Salesforce delivered a good quarterly report, which was roughly in line with expectations, showing few surprises. The company is managing to maintain stable revenue growth in the high single digits, thanks to the strong traction it sees in data cloud and AI demand. In a cautious spending environment, that is probably the best we can hope for.

Yes, we’d like to see and hear a bit more numbers on Agentforce, but we know it will take some time to ramp up and become more meaningful. Some patience and conviction are required from shareholders for now.

Meanwhile, the company continues to steadily improve its margins and deliver healthy cash flows, enabling it to maintain excellent financial health.

Not really anything to complain about so far, in my opinion.

Before we move on, just a quick word…

Want more out of your subscription?

InvestInsights PRO - $7.50/month ($70/annually)

An additional 2-6x/month premium stock analysis.

Full insight into my own portfolio (15% return CAGR since 2022).

Monthly portfolio updates + Instant transaction alerts (Fully transparent)

A complete overview of all my target prices and ratings (Excel file).

2x/month The Watchlist Report

Instant access to earlier premium analysis on, for example, Adobe, Thermo Fisher, Spotify, and The Trade Desk.

Outlook & Valuation

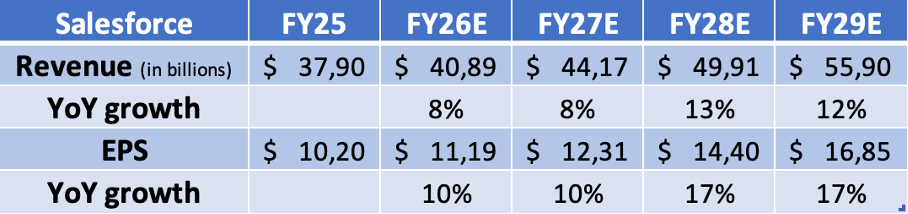

Following a better-than-expected Q1 result and a strong FX tailwind so far this fiscal year, Salesforce is confidently raising its FY26 guidance by $400 million to $41 billion - $41.3 billion, reflecting YoY growth of 8-9%. This reflects the expectation for stable growth throughout 2025.

However, while the guidance raise is great, it is worth pointing out that this is almost entirely driven by a foreign exchange tailwind of $400 million compared to the previous guidance, so the guidance hike does not actually reflect an improvement in demand, although I also hadn’t anticipated any, considering the significant macro headwinds and global uncertainty.

More importantly, management reaffirmed its subscription and support revenue growth guidance of 9% YoY in constant currency, driven by momentum in Data Cloud and some minor contributions from Agentforce. This does show some confidence, though I bet Wall Street may have hoped for some more.

All of these numbers assume a consistent demand environment, not incorporating any further weakening in demand later this year from a further economic growth slowdown or tariffs, which I am actually counting on.

As for the bottom line, management reaffirmed its earlier guidance for a FY26 operating margin of 34%. This should enable operating cash flow growth of 10-11% and free cash flow (FCF) growth of 9-10%. This remains healthy and in line with expectations.

Personally, I am not as optimistic about Salesforce’s near-term prospects. I anticipate that economic weakness and macroeconomic headwinds will put pressure on near-term demand and deal completions in the second half of 2025 and potentially into the first half of 2026, but this remains highly uncertain amid the changing policies of the Trump administration. Therefore, I just don’t think assuming a stable demand environment is the way the go, especially with AI deals not ramping up as quickly as expected.

Yes, AI and Data Cloud demand should offset some of this weakening demand, but I still expect to see some broader demand weakness reflected in the numbers later this year. As for the bottom line, performance, I am not changing too much from my prior expectations.

As for the years ahead, I expect a stable ramp-up of Agentforce deals and usage to drive a new leg of growth for Salesforce and to re-accelerate this back into the double digits. However, I don’t expect to see a meaningful reflection from Agentforce in the Salesforce numbers until likely the first half of 2027, potentially in late 2026, as a bumpier macroeconomic environment will likely push back the much-anticipated explosive growth and ramp-up.

All these assumptions are reflected in the projections below. For reference, these near-term projections have remained mostly steady, while my medium-term projections have shifted slightly more positively.

With shares down 9% since I last covered these and my financial projections mostly unchanged, Salesforce shares have actually gotten a bit cheaper, while also dropping below my targeted buying range. At a current share price of approximately $265, Salesforce shares now trade at roughly 24x this year’s earnings, which is much lower than we have seen from Salesforce over the last decade. For reference, its 5-year and 10-year averages sit at around 40x and 50x, respectively.

Of course, this lower multiple makes a lot of sense considering the significant slowdown in growth. Salesforce is no longer growing by mid-to-high teens, and I honestly don’t expect it to return to this kind of growth. Therefore, a lower multiple makes a lot of sense.

Nevertheless, paying just 24x earnings for a company as strong and important to businesses of all sizes like Salesforce is not too crazy at all. Salesforce still absolutely dominates the massive CRM market, is a frontrunner in next-gen AI technology, has a very strong balance sheet, and excellent cash flows. Furthermore, it is still expected to deliver strong financial results through the end of this decade, with growth likely to return to double digits and EPS anticipated to remain impressive at a mid-teens compound annual growth rate (CAGR).

I must admit, I like paying only 24x earnings for this one.

Looking at some other multiples, Salesforce now trades at an EV/EBITDA of about 16x, which is significantly below its 5-year average of 43x and well below the sector average of 28x and the broader technology industry average of 31x. Again, Salesforce shares appear to be attractively priced in relation to its growth potential and sheer strength.

Finally, we are now looking at a growth-adjusted PEG of 1.8x, which is nicely below its 5-year average of 2.2x and in line with the sector average, despite Salesforce being one of the largest and highest-quality businesses in the sector.

Long story short, Salesforce shares seem attractively priced, regardless of the valuation method you choose, making them a good buy today.

For reference, using a 26x long-term multiple, which I believe is much deserved considering the expectations for a return to double-digit growth and its strong market position, I calculate an end-of-fiscal 2028 target price of $374 per share. From a current share price of $265, we are looking at potential annual returns of 14% (CAGR), which I believe is excellent.

In my view, this presents a solid risk-reward profile with substantial downside protection and considerable room for outperformance, given the cautious projections (below Wall Street) and de-leveraged multiple used.

In my opinion, Salesforce shares finally look like a good buy today.

Salesforce shares also appear attractively valued using other methods like a reverse DCF. Seems like a pretty good deal right now.

Much smaller, but Salesforce acquired another AI hiring company called Moonhub. Is this a sign that Salesforce is getting back to its old habit? https://techcrunch.com/2025/06/02/salesforce-buys-moonhub-a-startup-building-ai-tools-for-hiring/