The Bargain Radar #1 - Here are three stocks worth buying today

There are always great investing opportunities to be found in the financial markets for those able to look through the noise. Let me introduce you to three today!

Make sure to also check out the [FREE] subscriber chat, in which I post daily market updates and business news that stand out. Here, you’ll also find my own trading instant trading updates any time I sell or buy shares.

Hi everyone, and welcome to this very first edition of The InvestInsights Bargain Radar!

I am happy to introduce this new format to you in this first-ever edition. The idea is simple: In each post, I will discuss two or three stocks I deem undervalued today.

I will introduce the business briefly, explain why it is a compelling investment, and, by examining recent share price performance, developments, and current multiples/potential returns, explain why shares are undervalued right now and, in my humble opinion, a great buy.

In other words, I will discuss two or three great buying opportunities, one more in-depth than the other, depending on the situation, to put them on your radar so you can investigate them further and uncover great investment opportunities.

Starting this January, I will publish this format 2x per month, one time free for all of you, with the second one being exclusively for paid subscribers.

Sounds good, right?

Well, without further ado, let’s delve in!

Here are three of the best, most compelling opportunities out there right now!

Advanced Micro Devices, Inc. (Ticker: $AMD)

Let’s start with some key data:

Performance

TTM share price return: -27%

1-month share price return: -7% (12-month low price)

Valuation

FWD P/E: 23x (FY25 consensus)

FWD PEG: 1.0

Growth projections

Expected 4-year revenue growth CAGR: 20%

Expected 4-year EPS growth CAGR: 35%

AMD is currently one of the most obvious large-cap bargains, without a doubt.

For those unfamiliar with the business, Advanced Micro Devices (AMD) is a leading global semiconductor company that designs and produces high-performance computing, graphics, and visualization technologies. Founded in 1969 and headquartered in Santa Clara, California, AMD is known for its innovative microprocessors, GPUs, and system-on-chip (SoC) solutions, which power a wide range of devices, from personal computers and gaming consoles to data centers and embedded systems. Over the years, AMD has gained significant market share by emphasizing innovation, performance-per-dollar value, and energy efficiency.

This has made it one of the leading suppliers of PC processors today, competing with Intel but rapidly gaining market share. It is also the only real competitor to Nvidia in the data center GPU space. While taking only a very small piece of the market, the insane GPU demand is leading to rapid growth for AMD, which is able to bring products to market that can compete well. This makes it a key beneficiary of the AI boom.

Ultimately, without going too much in-depth right now (I am just here to alert you to key opportunities, not a full business overview), this is an excellent business with healthy and rapidly growing (and currently recovering) financials, terrific growth prospects thanks to market share gains in its PC processor business, a well-performing gaming segment, and a rapidly growing data center segment that manages to compete with Nvidia.

However, overly negative sentiment continues to weigh on its shares, with any negative news seemingly leading to a sell-off in AMD shares, which is completely undeserved. As shown in the data above, AMD shares have been under considerable pressure for most of 2024, delivering a negative return in 2024, even as revenue growth turned positive again after a cyclical slowdown in recent years, and EPS recovered aggressively.

Furthermore, it also considerably underperformed its peers. For reference, the SMH semiconductor ETF gained 40% over the last 12 months, and Nvidia is up a whopping 134% over this same period.

And, honestly, I have a really hard time explaining this significant underperformance. Looking at its most recent quarter, AMD shows recovering revenue, once again growing double digits (+18%), recovering margins (gross margin up 300 bps), and a blinding performance by its data center unit (revenue up 122%), which is the new bull case driver for AMD, similar to Nvidia.

In other words, the business is firing on all cylinders. While AMD's performance at last week’s CES was somewhat unexciting, there is plenty to like here. I believe it is a matter of time before investors and Wall Street recognize this again and value AMD shares accordingly.

Yes, I am an AMD bull

Outlook & Valuation

AMD has an extremely bright future thanks to its exposure to fast-growing markets and likely market share gains in the data center GPU market and continued share gains within its client (PC) segment. The company is exceptionally well-positioned for the future and, in my view, still one of the more exciting opportunities within the semiconductor sector.

This is also reflected in the medium-term Wall Street consensus. Analysts now expect AMD to further recover in FY25 before revenue normalizes in the high teens in the years after, still reflecting a 20% revenue CAGR through FY27. Meanwhile, recovering margins and additional margin gains should result in significant EPS growth at a CAGR of over 30%, as shown below.

A pretty impressive growth outlook.

Yet, despite all of this, negative sentiment has prevented this great outlook from being priced in sufficiently, with AMD shares trading at absolute bargain levels.

Currently, AMD shares trade at just 23x the FY25 EPS consensus, which is absolutely ridiculous for a business with such a brilliant outlook and of such high quality. For reference, this is just short of the sector median and well short of AMD’s 5-year average multiple of 42x.

Accentuating its clear value even more is the current PEG multiple of around 1x. For perspective, a PEG prices in forward growth and a multiple below 1 points to bargain territory. In other words, AMD’s forward growth seems nowhere near priced in, with its PEG well below the sector median of 1.8 and its 5-year average of 1.3.

Ultimately, I feel like it’s safe to say AMD shares are completely mispriced and offer considerable upside from current levels. Whatever valuation method I use, a DCF or multiples, even under conservative assumptions, I end up with an average end-of-2026 target price of $208, representing potential annual returns in excess of 30% (CAGR), which is nothing short of sublime.

At these levels, around $120 per share, AMD is one of the most compelling long-term opportunities you’ll find, with a very favorable risk-reward profile.

I am a happy buyer at these levels.

PepsiCo, Inc. (Ticker: $PEP)

Let’s start with some key performance and valuation data:

Performance

TTM share price return: -13%

1-month share price return: -8%

Valuation

FWD P/E: 17x (FY25 consensus – 28% discount to the 5-year average)

FWD PEG: 3.0 (11% discount to the 5-year average)

Growth projections

Expected 4-year revenue growth CAGR: 3%

Expected 4-year EPS growth CAGR: 6%

Dividend

Current yield: 3.75% (31% above the 5-year average)

Payout ratio: 66%

Growth: 7% CAGR – 52 consecutive years

Consumer staples giant PepsiCo’s share price has been under pressure for most of 2024 as investors shifted their focus to higher growth and more exciting stocks. In addition, the snacks and beverage sector faced pressure from outside risks like deglobalization and the rise of GLP-1 drugs, which put pressure on the likes of PepsiCo and Mondelez.

As a result, PepsiCo shares have lost 25% of their value since setting an all-time high in mid-2023, 13% over the last 12 months, and experienced significant pressure over the last month as well. This recent weakness has pushed shares to their lowest level since mid-2021, even as revenue is currently more than 15% higher.

Subsequently, PepsiCo shares have seen their valuation multiples drop considerably to their lowest levels since the early 2020 COVID-19 sell-off. Indeed, PepsiCo shares are straight-up cheap right now. While I can see why the company doesn’t quite earn its historical multiple amid long-term pressures and decelerating growth projections, the sell-off seems well overdone to me. This overly negative sentiment has pushed PepsiCo into bargain territory right now, with potentially market-beating returns from an extremely defensive investment.

This makes PepsiCo one of the more attractive opportunities out there, in my opinion.

Now, PepsiCo probably only needs very little introduction, but let me give you a short one, nevertheless.

PepsiCo is a leading global food and beverage company renowned for its diverse portfolio of iconic brands. Headquartered in Purchase, New York, the company operates in more than 200 countries and territories, offering a wide array of products that cater to various tastes and preferences. PepsiCo's product lineup includes well-known beverages such as Pepsi, Mountain Dew, and Gatorade, alongside snack brands like Lay’s, Doritos, and Cheetos. The company also produces healthier options through its Quaker and Tropicana lines, aligning with evolving consumer demands.

Driven by consistent price increases in line with inflation, strong execution, global expansion, and strategic acquisitions, PepsiCo has consistently grown its top and bottom lines at a decent rate, and this trend is expected to persist.

Of course, PepsiCo is not an exciting growth stock but rather a defensive cornerstone one can count on during tougher times. Thanks to its resilient business and inflation-resistant nature, PepsiCo is an interesting investment despite its relatively slow growth.

Outlook & Valuation

Looking ahead, Wall Street analysts expect PepsiCo's growth to remain mostly in line with what we have gotten used to: low single-digit revenue growth just ahead of inflation and EPS growth in the mid-to-high single digits driven by steady margin expansion.

Here is what analysts now project:

This still reflects pretty solid growth, or as much as one can expect from a mature business like PepsiCo.

Interestingly, with the share price down considerably over recent years and months, PepsiCo’s multiples have gone down significantly to their lowest levels since early 2020 during the COVID-19 sell-off, as pointed out before, which is just completely ridiculous, in my opinion.

Alright, yes, the situation has gotten complicated as the company has struggled with growing input costs and subsequent higher prices, leading to declining volumes. Also, the threat of GLP-1 drugs is becoming more real by the day. Recent research is increasingly pointing to the drug's use impacting consumer spending on groceries and snacks in particular, which could hurt PepsiCo’s business as drug adoption grows.

Now, this is still largely speculation, and there is too little substantial research available to draw real conclusions. However, I agree that this risk has reached the point where it needs to be priced in.

Nevertheless, I think this has been overdone by now. PepsiCo shares represent excellent value at current levels below $150 per share, even amid these risks. PepsiCo shares now trade at just 17x next year’s earnings, a whopping 28% discount to their 5-year average, which doesn’t at all reflect the quality, reliability, and expected growth of this business.

You see, while growth might not be mind-blowing, this is a stable compounder adding a piece of reliability to your portfolio.

For reference, using DCF and calculations based on multiples, I calculate an average end-of-2026 price target of $184, reflecting potential annual returns of over 11% (CAGR) based on conservative estimates, which alone should be able to beat most global benchmarks, and that with a highly defensive investment. Meanwhile, you’ll also now receive a very sweet and well-covered 3.75% dividend, bringing potential annual returns to a total of 15%, which is terrific.

This represents a very favorable risk-reward balance, with significant potential for outperformance, which is why I am compelled to pick up PepsiCo shares at these levels.

Ultimately, I strongly believe PepsiCo is an absolute bargain right now.

Before we move to the third bargain, just a quick word…

Rijnberk InvestInsights is a reader-supported publication. I try to keep most of my content free for everyone, but I can’t do this without your support!

So please subscribe if you like our content! Want to receive even more of our investment insights and show even more appreciation? Please consider upgrading to our paid tier (only $7.50 monthly or just $70 annually).

In addition to all the free stuff, this also gets you access to even more premium analyses (a total of 3 per month), full access to my own (outperforming) portfolio, immediate trade alerts in the subscriber chat, and a full overview of all my price targets and rating, and even more!

Want to try our paid tier for free? Simply get three of your friends and family to join Rijnberk InvestInsights and receive one free month!

Adobe, Inc. (Ticker: $ADBE)

Let’s start with some key performance and valuation data:

Performance

TTM share price return: -31%

1-month share price return: -12%

Valuation

FWD P/E: 20x (FY25 consensus – 42% discount to the 5-year average)

FWD PEG: 1.8 (17% discount to the 5-year average)

Growth projections

Expected 4-year revenue growth CAGR: 10%

Expected 4-year EPS growth CAGR: 11%

Adobe is probably one of the highest-quality businesses you’ll find. It has a massive moat, a very healthy balance sheet, and an unequaled market position in a steadily compounding industry, fueling consistent double-digit growth on both top and bottom lines.

For a comprehensive analysis of the business, check out my November post on Adobe, where I dissect its financials and fundamentals. You’ll find it below!

However, while Adobe is undoubtedly a terrific business, its shares have come under considerable pressure over recent years, currently trading 40% below their late 2021 all-time high. This is mostly due to three factors: a post-COVID revenue growth slowdown, which has scared off investors, growing competition, and, above all, the threat from GenAI.

Each of these is a fair concern. Growth has indeed slowed considerably and has settled in the low teens, whereas investors had gotten used to consistent growth in the low twenties or high teens. Meanwhile, competition from Canva, for example, has led to some concerns over Adobe’s moat and its ability to fight off free or lower-priced competition. And finally, it is not hard to imagine how AI could eventually replace Adobe’s digital design business.

However, the problem is that Mr. Market tends to overreact, leading to overselling. This is exactly what is happening here. Again, while each of these concerns is fair, the subsequent reaction is well overdone and has pushed Adobe shares into value territory and to extremely attractive levels for long-term investors.

Let me divide this final analysis into several parts to make it easier to understand. Then, let me show you the value!

This is Adobe

For those who are not familiar with Adobe, it is a global leader in digital media and creative software solutions. It is known for its innovative products, which allow individuals and businesses to create, edit, and share content. Founded in 1982, Adobe has revolutionized industries such as graphic design, video editing, photography, and web development with its software suite, including popular tools like Photoshop, Illustrator, Premiere Pro, and Acrobat.

The company's cloud-based platform, Adobe Creative Cloud, offers a comprehensive range of applications for creatives, marketers, and professionals. These applications enable seamless collaboration and workflow management. Also, this subscription-based offering means Adobe has a very high-quality recurring revenue stream, which is brilliant!

Today, its products are widely used by professionals in various industries, from advertising and filmmaking to publishing and education. The company’s software has become the go-to for graphic designers and digital marketers. In fact, graphic designers are taught the craft in school using Adobe software. By now, many of its software tools have become verbs, like “photoshopping,” and tools like Adobe Acrobat and file formats like ‘PDFs’ have become industry standards.

As a result, today, the company holds a commanding market share of over 80% in the graphic design industry—that's absolutely whopping! Through its years of product development and reliable brand, the company has built a massive moat, ranking its brand as the 14th most valuable globally at $35 billion, according to Interbrand.

Meanwhile, the underlying digital design and marketing industry is expected to grow at a 10% CAGR through the end of the decade, and management points to its TAM growing at a 12% CAGR. Thus, there is no lack of growth potential here, either. The growth runway for Adobe, while lesser than we have gotten used to, remains significant, and with its dominant market position, the company is expected to fully benefit from this underlying growth.

What to make of the AI threat

However, there is a big elephant in the room here, and that’s the rise of AI and what it means for Adobe, which I believe is massively overblown. In short (for a longer explanation, I recommend you check out my Adobe Deep Dive linked to before), AI is both an opportunity and a risk for Adobe.

On the one hand, AI is an opportunity for Adobe as it allows it to improve its product offering with easy-to-use AI features in graphic design and photo editing, which should improve the user experience and the value of its products, while maintaining its creative freedom.

Though, at the same time, image generators are already getting quite advanced, and if such a program can generate the image you need for free or at least low cost at the same quality, then why pay hundreds per year per user for the Adobe software stack?

Yes, that is a problem, but not as big as many make it seem. Yes, among amateurs looking for a quick picture, AI might be a great, cheap, and easy solution. AI-driven design tools can generate graphics, edit images, or even produce video content with minimal human input, diminishing the reliance on Adobe's products for simple pictures.

However, for the professionals out there, these upcoming AI tools are unlikely to fully replace Adobe’s software suite, as AI tools offer nowhere near the capabilities and creative freedom Adobe’s expansive products do – the freedom and capabilities professionals require for complex projects. Each of these professionals can confirm AI won’t replace this anytime soon.

Moreover, Adobe's suite is deeply integrated across various creative disciplines, enabling seamless workflows for professionals who may be working on projects that span multiple media types. This level of integration and flexibility is difficult for standalone AI tools to replicate.

So, while I do anticipate Adobe to suffer some market share losses as amateurs and potentially small businesses start using free AI programs instead of expensive Adobe software, I continue to view Adobe’s moat as powerful and its business as resilient. I only expect a minimal impact in the long run and for Adobe to keep growing its top and bottom line strongly, helped by the addition of AI features.

No need to panic.

As a result, growth expectations through the end of the decade remain solid, making current price and valuation levels very much appealing amid these overreactions. Long-term, this business remains sound.

Outlook & Valuation

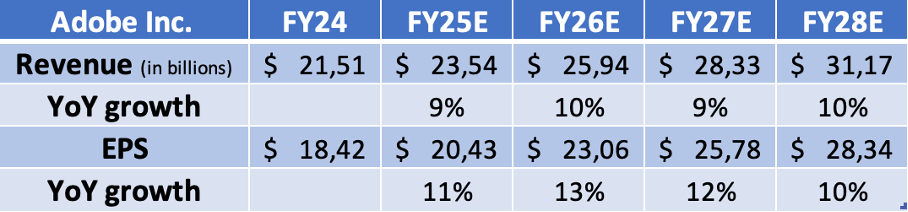

So, what kind of growth can we expect?

As shown below, the current Wall Street consensus remains solid, pointing to revenue growth in the high-single digits to low-teens and EPS growth in the low-teens, which is still pretty excellent, especially considering we are looking at a business with a massive moat and deriving the majority of its revenues from subscription-based contracts.

As I said, this remains a sound business with great prospects.

However, the street doesn’t value it as such. After last month’s additional 10% share price drop, Adobe shares now trade at just 20x the current fiscal year’s earnings consensus, a whopping 42% discount to the 5-year average multiple.

This can only be partly explained by the slowdown in growth. Adjusting for forward growth, we are looking at a PEG of 1.8, which is still a 17% discount to the company’s 5-year average and roughly in line with the sector median, even though Adobe is by far the highest-quality pick in the sector.

In other words, unless AI completely disrupts Adobe in the years ahead, the current valuation makes no sense, and current price levels reflect excellent long-term value.

For reference, using both DFC and multiples-based calculations, I end up with an end-of-fiscal FY27 target price of $593, reflecting a long-term PEG of 2.1 and P/E of 23x and pointing to potential annual returns in excess of 12% (CAGR), which should be well enough to beat global benchmarks at a favorable risk-reward balance.

Therefore, I conclude that at current levels of around $420 per share, Adobe is another bargain!

Looking to do your own stock analysis? Consider using StocksGuide, my go-to stock and business analysis tool. Check it out! Most of its features are free.

Your writing is both informative and relatable. It’s clear you put a lot of thought into each piece, and it shows. I subbed

Why is the picture saying “Bargain rarar” instead of “Bargain radar”?