Universal Music Group – A Deep Dive into one of Bill Ackman’s favorite stocks

Universal Music Group dominates the music industry. Let me show you exactly why Bill Ackman loves this business and why it is one of the best buy-and-hold stocks out there.

Ever heard of UMG or Universal Music Group? I bet most of you never have, which is not surprising, considering this company mostly operates behind the screens of the music industry. Yet, this company has a €42 billion market cap, is the undisputed leader in the music industry, is a brilliant long-term compounder with incredible longevity, and one of the largest shareholders here is activist and super investor Bill Ackman, who has called it one of his favorite long-term investments on many occasions.

However, UMG shares got a massive beating after reporting quarterly results in July, dropping 25% in the span of a few days. This entirely erased all the YTD gains, and even as shares have regained some of their value since, these are still down 8.5% YTD, significantly underperforming compared to the S&P’s 20% gain.

Meanwhile, UMG has a strong track record of growth over longer periods, having grown its revenues over the last decade at a very steady 8.5% CAGR. This growth has been even more impressive over the last five years as growth accelerated to a 13% CAGR, which is top growth.

However, this tremendous growth isn’t reflected in the share price performance since the 2021 IPO, as the company has seen its valuation trend down over the years. In fact, after the July sell-off, shares hit their lowest valuation level… ever.

On a TTM basis, shares trade at 27x earnings, compared to a 2-year average of 44x. As a result, shares have returned only 1% since their IPO, even as revenue has grown by 31%(!).

So, yes, there are plenty of reasons to pay some attention to this hidden gem today.

This is Universal Music Group (UMG)!

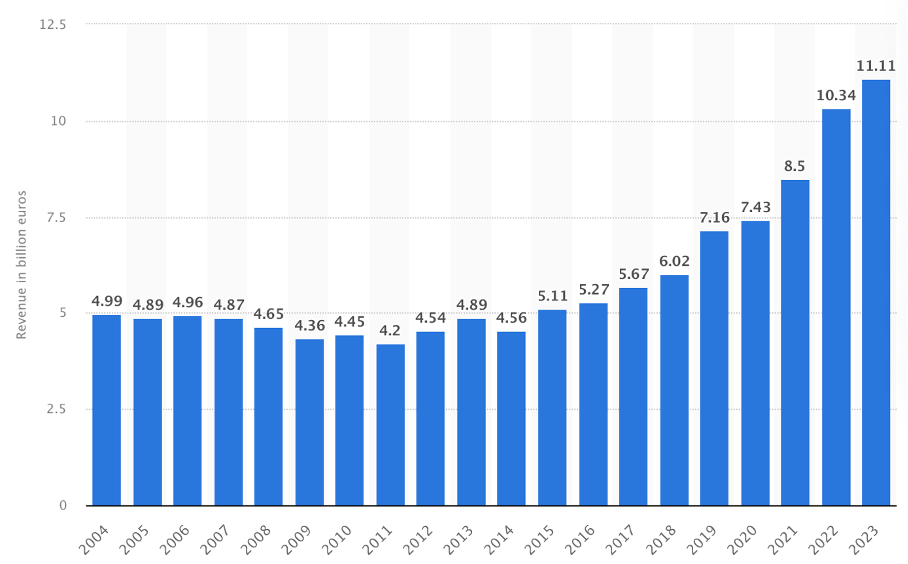

So, what is Universal Music Group or UMG? Like I said, I bet most of you, maybe besides those working in the music industry, have never heard of this company trading on the Amsterdam Stock Exchange. And yet, this company is a giant in the music industry, being the world’s largest independent record label and music publisher with a €42 billion market cap and annual revenue of around the €10 billion mark, growing steadily.

Starting with the basics, Universal Music Group (UMG) is a global music corporation that is one of the "Big Three" record labels in the music industry, alongside Sony Music and Warner Music Group. Notably, the company hasn’t long been trading as a separate entity; it used to be part of French media conglomerate Vivendi before the 2021 spin-off, from which point it started trading on the AEX.

Since the 2021 spin-off, we can safely say the company has been performing tremendously well, growing revenues at a 14% CAGR.

The company operates a broad array of businesses, all engaged in the music industry, which includes recorded music, music publishing, merchandising, and audiovisual content.

At the center of UMG sits its recorded music segment, which is the core of its business model. This includes activities related to licensing and distribution of music, artist royalties, and revenue from physical and digital sales. This includes revenue from music streaming from its artists, music licensing for various media (movies, TV, commercials, video games) and public performances, and the revenue from artist-related merchandise, sponsorships, and other brand partnerships.

Any time you hear a song from a UMG artist, anywhere, I can assure you it brings in cash for UMG. The same goes for that Taylor Swift or Guns N’ Roses shirt you buy online. UMG benefits through many different ways from the success of its artists – the company is more than just a record label and owner of recorded music and rights, as it has many different nicely growing revenue streams.

For reference, physical revenue has been growing at an 11% CAGR in the last three years, merchandise revenue at a 39% CAGR, and license revenue at a 14% CAGR. So, indeed, there has been pretty great growth across the board.

Back to the heart of this business, the company owns and operates a diverse array of labels, including Capitol Records, Def Jam Recordings, Interscope Geffen A&M Records, Island Records, Republic Records, and Universal Music Latin Entertainment. Each label under UMG’s umbrella manages a roster of iconic and emerging artists, covering an eclectic mix of genres from pop and rock to hip-hop, classical, and Latin music.

Through this diverse array of labels, the company has built up a pretty insane collection of songs and albums, as well as a terrific portfolio of artists.

Now, there is no way I can name all the big names under the UMG umbrella right here. Still, for reference, it includes the likes of Taylor Swift, The Weeknd, Ariana Grande, Sabrina Carpenter, Post Malone, Drake, Justin Bieber, J Balvin, U2, Coldplay, Neil Diamond, ABBA, and Guns N’ Roses.

Check out the two images below to better understand the songs and artists within the UMG universe. And this isn’t anywhere close to everything, of course.

I just hope this gives you a sense of its portfolio. And if the names above don’t speak for themselves, just consider that UMG accounted for at least 7 of the top 10 most streamed artists in each of the last five years.

In fact, with a roster of artists that ranges from the Beatles and Elton John to Taylor Swift and Drake, including some of the most enduring songs and albums and hottest artists today, you can safely assume that in any given week, the company is typically responsible for about 8 of the 10 top songs streamed worldwide.

Indeed… Insane! How is that for dominance, right?

In the end, UMG today holds a 38.2% overall market share in the music label market, putting it comfortably ahead of Sony Music and Warner Music, according to Billboard.

Also, in terms of the music catalog, UMG is comfortably ahead of its peers, holding an impressive 40% market share, after making some gains over the last year. Across both categories, digital and physical music products, UMG has been expanding its market share over recent years.

So, yes, UMG is a real giant and force in the music industry.

Now, I can hear you wondering: Why do these artists all stick with UMG, and what stops them from going anywhere else or solo? Crucially, is there a real moat here?

While it might seem that UMG can be easily replaced—like an artist can easily switch music labels or even start independently—this isn’t quite true. There are multiple reasons why artists need UMG, both at the start of their careers and in the later stages, and why UMG has little to fear from its competition.

First of all, thanks to its massive and unprecedented presence in the industry, UMG has incredible bargaining power. Any streaming service or social media platform that wants to feature all its artists and music needs an agreement with UMG, and UMG generally gets the best terms compared to competitors as a result.

In addition, with operations in more than 60 countries, UMG has an unparalleled international presence. This extensive network allows the company to promote its artists on a global scale, tapping into diverse markets and audiences. For artists, this means greater exposure and the opportunity to connect with fans worldwide, which is particularly important in the era of streaming and digital music consumption, which is unparalleled.

Thanks to these factors and UMG’s influential brand and reputation in the industry, it is a sought-after partner for both established and emerging artists. The prestige associated with being signed to a UMG label can significantly boost an artist’s profile and career prospects. This strong brand identity, built over decades, instills trust and attracts top-tier talent seeking the best possible platform for their music.

As an emerging artist, a record label such as UMG and all its subsidiaries is your key to a larger market, big money, and global success. In most instances, their network, promotion, and reach are about the strongest of moats for these music labels, and UMG reigns.

This is why UMG has no trouble expanding its market share and presence. This business is a true force poised for long-term success.

One notable investor who acknowledges this is Bill Ackman! Let me tell you why UMG is one of his favorite stocks and why UMG is one of the best long-term investments out there!

Before we move on, just a quick word…

Rijnberk InvestInsights is a reader-supported publication. We appreciate you being here! Want to support our work a little bit more and show your appreciation? Consider upgrading to paid (only $5 monthly).

This allows me to push out even more content and gets you premium access to even more content, including my full insight into my personal portfolio!

Bill Ackman owns 10% of UMG, and this is why!

Since UMG’s 2021 IPO, legendary activist and super investor Bill Ackman has been among its largest shareholders. He currently owns just over 10% of the company, valued at roughly €4.5 billion.

In fact, it is one of his absolute favorite long-term investments, and in an interview with Lex Fridman earlier this year, he clearly laid out exactly why.

You see, Bill Ackman, one of the best and most well-known investors out there. He has a brilliant track record of outperformance and a very clear strategy for picking the right stocks.

With his Pershing Square fund, Bill Ackman is heavily focused on picking up shares in businesses for which he can predict with a high level of confidence what its cash flows are going to look like in, let’s say, the decade ahead – the long-term. This is why he prefers to invest in industries he knows very well and businesses with solid moats, like the restaurant industry and Chipotle – one of his most well-known investments.

While future cash flow projections are always tricky due to thousands of factors that can impact these performances, investing in the right industries and businesses can limit this risk significantly. Obviously, despite all the things that might occur, analyst projections for McDonald’s are far more reliable than for any given startup.

In other words, Bill Ackman looks for nondisruptive businesses, which will almost certainly be worth more in ten years without you having to worry due to their moat and predictability.

A company that perfectly matches this is Universal Music Group. First of all, as explained thoroughly before, UMG has a pretty significant moat and is by far the largest player in the industry while still growing its market share. It is a terrific business.

However, even more important is the health, longevity, and durability of the underlying industry.

As said beautifully during the latest UMG Capital Markets Day, “Music is fundamental to the human experience.”

Music is forever, thousands of years old, and likely to still be here in another thousand, in theory. This alone already makes it a compelling industry to consider investing in.

In terms of long-term growth, there is plenty to like in this industry. While it has gone through numerous changes over the decades, from LPs and CDs to streaming, it has always been a compelling growth industry with a bright future.

Going forward, this isn’t expected to change. Remarkably enough, global spend on music today is still sitting at only half of its 1999 peak, leaving plenty of room for growth as the industry grows and music is becoming more accessible!

Interestingly, since the 1999 high, global recorded music revenue dropped 41% to a 2014 low as the industry shifted from the CD era to the digital download era, which didn’t really work out for music publishers.

Positively, streaming gave the industry a massive boost as music became way more accessible and more affordable, propelling demand. Since then, the industry has more than doubled, reaching a new high in 2023, with streaming now accounting for the majority of revenue.

Yet, there is still a lot of room to run. While global paid music subscriber numbers have already skyrocketed in recent years, global penetration is still relatively low, especially in less developed markets. While in the U.S., penetration is decent at 42% (though with plenty of room to run), in markets like Brazil or China, this is still at a very low 13%, with India, another massive growth market, only seeing 1% penetration.

Furthermore, there is still a lot of room for players like Spotify or Apple Music to further monetize their offerings. So, yes, clearly, there is still a lot of room to run for the streaming revolution.

As a result, UMG expects paid subscription revenue to continue growing strongly at an 8-10% CAGR through 2028, and it will benefit as the largest owner of music rights.

Besides this, the further proliferation of social media is also a massive tailwind for the industry and UMG. Music is becoming a more prominent role in social media, especially on platforms like TikTok and Instagram. As these platforms grow and gather more users and usage, ad-supported revenues for the music industry balloon as well.

Today, these ad-supported revenues already account for a large portion of total music streaming revenue, but there is a lot of room to run with a continued shift of advertisement spend from analog to digital, significant ad-supported user growth, and increasing monetization.

Ultimately, this represents a pretty compelling long-term outlook for the industry. The music industry as a whole is projected to grow at a CAGR of 8% through the end of the decade. Meanwhile, streaming subscribers are expected to increase at a double-digit growth rate over the next few years. Just as important, paid streaming revenue is projected to grow at a 10% CAGR through 2030.

While UMG might not be in the fastest-growing parts of the market compared to the likes of Spotify or Apple Music, this industry growth will remain a significant tailwind for UMG, most likely allowing it to grow its top line by at least high-single digits for many more years thanks to its dominance, insane portfolio, and solid moat.

Meanwhile, with the rise of streaming, the industry has also become a lot more predictable than ever before, and the same goes for UMG’s cash flows. You see, selling records, CDs, and vinyl is all about one-time purchases when an artist is hot and trending or through a new release. Meanwhile, with streaming, a lot of these revenues and purchases are now subscription-based, meaning they are recurring and far more stable than ever before.

Of course, UMG is still exposed to the advertising cycle and the hype around merchandise, but this has still improved a lot compared to the previous decade.

Add to this the growth in digitalization and smartphone penetration, and it is not too hard to create a reliable growth model for the music industry and UMG. In other words, its cash flows and potential growth are getting quite predictable today, matching Bill Ackman’s model.

And then, finally, is AI a threat to UMG? Many fear so. I mean, with the capabilities of AI today, it isn’t hard to imagine AI writing and composing music. Yet, Bill Ackman doesn’t see it as a threat to UMG in the long haul, nor do I.

UMG has in the past proven to be very open to adopting new technologies and industry transformations; whether it’s the move from CDs to streaming or the addition of AI today, UMG tends to be a frontrunner when it comes to adapting and incorporating these new technologies, being a leading innovator.

While there are always risks for any business, the degree of risk here is minimal, thanks to UMG’s approach and incredible portfolio. Whatever the distribution format or platform used, UMG is there to benefit.

Furthermore, in the words of Bill Ackman himself, “Nobody falls in love with a computer-generated track.”

Music is just as much about the artist behind it and the story being told, as well as a physical presence and live performances. From this perspective, it will be hard for AI to really replace artists and musicians.

According to Bill Ackman, AI will likely be a tool for making music and taking it to the next level instead of a replacement.

And even if we ever get to the point where an AI/robot can take a human form and have human-like sentience, this doesn’t change anything for UMG. In theory, this will still be an artist for UMG to represent.

Now, this might be thinking very far into the future, and whether this is relevant today is arguable, but it illustrates how hard it is to disrupt UMG’s business.

Ultimately, UMG, with its dominant market position, resilient cash flows, and the music industry's evergreen nature, aligns perfectly with Ackman's preference for businesses that offer predictable growth over time.

For long-term investors, UMG should be on their watchlist, at the very least, for obvious reasons. From a fundamental perspective, this is a must-own.

But is it a buy today? To answer this question, let’s finally delve into UMG’s financials before moving to the outlook and valuation.

Shares got sold off by 25% on pretty okay quarterly numbers

As already pointed out before, we can comfortably say that UMG’s most recent quarterly results weren’t especially well received by investors, with shares losing a quarter of their value in response.

And honestly, I believe this was a massive and unjustified overreaction based on top-line numbers, not considering the underlying dynamics of the business and recent developments.

In the end, revenue came in 1.6% above Wall Street expectations, and EBITDA was roughly 0.5% higher. It was more so the volatility in UMG’s cash flows and across operating segments that caused concerns, not at all considering the dynamics of the business.

UMG has been historically sensitive to quarterly fluctuations in one source of revenue or another. Focusing and reacting to quarterly results is absolutely pointless here. Furthermore, everything points to the current weakness being temporary.

Starting with the top-line numbers, UMG reported revenue growth of 10% to €2.93 billion. This was driven by a strong 10% growth in music publishing, in part thanks to a 17% growth in digital revenue from continued growth in streaming subscriptions. This growth remains significant.

Growth in recorded music revenue also remained solid overall at 7%, although it slowed down from 12.5% growth last year. Analysts had expected 11% growth.

Positively, the fluctuation and slowdown can be explained by looking at the growth of many music DSPs. The slowdown certainly was in part due to the timing of price increases at Spotify and Apple last year. These are the sorts of fluctuations UMG is exposed to.

Furthermore, global growth in subscriptions has been slowing down somewhat. While the likes of Spotify and YouTube continue to perform well, other large partners have seen adoption slow.

However, the biggest negative of last quarter, and the primary reason for the sell-off, was the 4% drop in ad revenue, whereas analysts expected growth of 8.5%.

Again, at least the negative surprise can be easily explained.

Most importantly, for a large portion of the quarter, UMG music and artists weren’t present on TikTok due to a licensing dispute. Initially, the companies couldn’t agree on a licensing renewal, which led to UMG pulling all its content from the platform. TikTok couldn’t feature any UMG artists, and UMG lost its TikTok ad revenue.

This had quite a negative impact on UMG’s second quarter. Positively, a few months on, the companies reaching a new deal, ensuring artists get their fair share and their rights protected in the age of AI.

On top of this, the company also saw a change in its licensing agreement with Meta. For some time, Meta tried offering premium music videos on Facebook, but seeing little success, Meta pulled the feature, taking away some ad revenue from UMG.

Excluding these two one-off impacts alone, ad-supported streaming revenue growth would be positive YoY. While still far from optimal, the reported numbers do paint a darker picture compared to reality.

Looking ahead, while near-term headwinds might persist with an uncertain macroeconomic climate, longer-term advertising will remain good for UMG as music on social media continues to grow and ad spending moves from physical to digital. So, worry all you want… instead, try focusing on the future.

Finally, both physical and licensing revenue grew nicely once more. Physical revenue grew 14% YoY in Q2, thanks to continued enthusiasm for Taylor Swift and Billie Eilish. While this category will be more release-driven and, therefore, more volatile quarter-to-quarter, the growth we are seeing today isn’t a standout. Physical revenue is a growth factor for UMG.

Meanwhile, licensing revenue was up 18% YoY, , driven by improvements in licensing and synchronization income, higher direct-to-consumer income, and greater live and audiovisual revenues.

Ultimately, looking at these top-line numbers and putting them into perspective, it really wasn’t that bad, especially for long-term investors.

Meanwhile, operationally the company also continues to execute very well. In the three largest music markets, the U.S., Japan, and the UK, UMG accounted for 11 of the top 15 albums in the first half of 2024, including each of the top three. Pretty extraordinary.

Then, moving to the bottom line, adjusted EBITDA grew 11% YoY as the EBITDA margin came in at 22.1%, up 20 bps YoY. The EBITDA margin has been trending up nicely in recent years, hitting a high in 2023 and growing further in 2024.

For the operating margin, the story isn’t as straightforward, with this trending down in recent years as the company is forced to heavily invest in its content. As a result, operating costs have been outgrowing revenue, partly due to rapid growth in lower-margin segments like merchandising.

On a positive note, so far this year, the operating margin has rebounded a bit, up 220 bps YoY. I am confident that UMG will be able to expand these margins further in the years ahead as higher-margin subscription revenues outgrow other segments.

Finally, FCF came in negative at €460 million due to ad revenue headwinds and significant investments. Again, quarterly numbers fluctuate highly. On an annual basis, UMG has shown the ability to grow FCF steadily and has been reporting FCF in access of €1 billion in recent years, which is more than solid.

Also, UMG management has shown an excellent ability to succesfully invest in its business, maintaining its ROE above 40% and ROIC in the mid-teens to low twenties. These are pretty impressive numbers.

The company's balance sheet also looks healthy, considering its solid cash flows. Currently, UMG holds roughly €450 million in cash against €1.9 billion in debt. While far from ideal, this is manageable and healthy, earning a BBB+ credit rating from S&P Global.

This healthy position also allows it to pay a pretty solid dividend to shareholders, aiming to pay out 50% of profits. Shares currently yield a sweet 2.2%, translating into a payout ratio of 60% based on FY24 EPS projections, somewhat above management’s targeted range.

However, with EPS growth expected to be quite aggressive in the years ahead, analysts expect pretty solid dividend growth as well, expected to grow at a 14% CAGR through 2027. Ultimately, this is quite attractive – double-digit dividend growth and a 2.2% starting yield.

Once more, there is plenty to like here.

Looking to do your own stock analysis? Consider using StocksGuide, my go-to stock and business analysis tool. Check it out! Many of its features are free. (Note: this is an affiliate link)

Outlook & Valuation

Moving to the outlook, honestly, I have already discussed most of my thoughts. Like I said before, based on everything discussed, this company should be able to grow its top line by at least the high single digits, potentially reaching into the double digits, something UMG management backed during its most recent Capital Markets day.

UMG management now guides for revenue growth at a CAGR of at least 7% through 2028, driven by a subscription revenue growth CAGR of 8-10%.

Meanwhile, further margin expansion should allow adjusted EBITDA to grow at a CAGR of at least 10%, with an FCF conversion rate of 60-70%.

In my view, this guidance from management should quickly end any doubts or fears arising from the Q2 results. This company is well positioned for long-term success, and while quarterly results can fluctuate quite a bit, long-term, this business and its growth are sound, supported by a massively dominant position and solid underlying growth in the music industry.

With this guidance, I believe management might be somewhat conservative, which is a good position to take.

Personally, I am now projecting the following medium-term financial results.

Getting to the valuation, based on these projections, UMG shares now trade at roughly 29x this year’s earnings and 27.5x next year’s earnings, which in no way is a low premium to pay. However, we should consider that getting a massive moat and dominant position such as UMG in a promising industry never comes cheap. And at a PEG of around 2x, better considering future growth, shares don’t look that expensive.

Furthermore, historically, shares also don’t seem that expensive. On a 12 trailing month basis, shares trade at a P/E of 27x, which is far below the 3-year median of 43.1x. Whichever metric you pick, the story is the same: shares trade near their all-time lows.

Of course, this is no massive surprise, considering shares have sold off quite significantly and are still down over 10% YTD, even after regaining over 10% in recent weeks.

Ultimately, in my view, after this year’s underperformance, UMG shares look attractively priced, offering a favorable risk-reward opportunity.

I strongly believe UMG is one of the best buy-and-hold investments out there, thanks to its industry dominance, incredible music portfolio (moat), and the promising future of the music industry.

In fact, I have added UMG shares to my portfolio in recent weeks, and plan to keep adding as long as UMG shares continue to trade at a discount due to poor sentiment.

Current target price = €30

Potential returns CAGR through 2026 = 13% annually (inc. dividends)

If you enjoyed this format and would like to see similar posts in the future, please hit the like button, share your comments, and be sure to subscribe.