FedEx is still a Deep Value opportunity after Q4 results

Let's re-examine FedEx after releasing its fiscal Q4 results!

FedEx shares reached a new high since mid-2021 last week after the company reported its fiscal Q4 and FY24 financial results. As a result, those who bought the shares at their September 2022 low would now be able to lock in a very sweet 100% gain, though I doubt very few of you (me included) bought the shares as investors don’t particularly love this logistics and delivery leader.

In fact, I know FedEx is a company few of you (especially those in the U.S.) like in any way. From what I have seen in terms of reactions to my earlier posts covering FedEx, most of you probably hate every part of it due to poor experiences, and I can’t blame you – I might even agree.

However, despite this, I do really like FedEx shares because, whether you like the company and its services or not, it is one of the largest in both ground deliveries in the U.S. and global express services, which is a massive and critical market.

You see, each of these markets is projected to grow by mid-single-digits, with the U.S. market expected to grow at a CAGR of roughly 4.5% and the global express market, where FedEx is the industry leader, expected to grow at a 6% CAGR through the end of the decade.

With FedEx among the big three players here and not having the option of getting disrupted by smaller players, the company is in a prime position to benefit from this growth. In fact, Wall Street analysts agree, consistently projecting FedEx to grow revenue at a mid-single digits CAGR for the foreseeable future. The only thing that can really impact this is a struggling economy, but overall, investors get a predictable revenue stream and growth.

Now, I know this in itself isn’t the most exciting outlook, but when combined with management’s extreme push for cost savings and a reorganization through the DRIVE and Network 2.0 program, which should lead to many billions in annual cost savings, significantly faster-growing earnings, and a cheap valuation, the situation gets a whole lot more interesting.

FedEx is projected (Wall Street consensus) to grow its earnings by low to mid-teens for the foreseeable future, which makes the shares much more compelling. Add a valuation that sits at a 25% discount to the sector and is in line with long-term averages, and we get a very interesting investment opportunity.

Whereas over the last few months, or pretty much since I covered shares in January, the share price hadn’t really gone anywhere due to doubts over management’s cost savings plan and reorganization and its ability to deliver promised efficiency gains, the tables might have turned now as FedEx has proven it is very much capable of delivering.

As a result of the share price jump following the earnings report of last week, shares have now outperformed the S&P500 since my January buy call. FedEx shares have gained 21% since mid-January, beating the S&P’s 15% return.

Positively, I continue to expect FedEx to outperform global benchmarks as I am confident in management’s ability to deliver, making FedEx one of the best value opportunities in the market today.

Let me show you why current enthusiasm is justified by taking a closer look and breaking down its fiscal Q4 earnings report. It isn’t too late to join the party!

We try to keep all our analysis free for all of you to enjoy and benefit from! Want to support our work a little bit more and show your appreciation? Consider upgrading to paid ($5 monthly).

This allows us to push out even more content and gets you access to our exceptionally performing portfolio and premium subscriber chat!

We appreciate you all!!

FedEx growth turns positive amid market share gains

FedEx reported earnings on June 25, and as indicated in the introduction, the results did not disappoint. Looking at headline numbers, it doesn’t look overly impressive, as FedEx managed to only marginally beat the consensus. However, underlying the business is looking really good as management successfully executes its cost reduction initiatives and continues gaining market share.

For Q4, FedEx reported revenue of $22.1 billion, which marks a turning point from negative growth in recent years to positive growth, as this is up 1% YoY. As highlighted in the graph below, FedEx hasn’t been going through the easiest of times, with impressive pandemic growth turning into a very tough fiscal 2023 and 2024.

Of course, it is important to note that the entire industry performed weakly over the last twelve months. The package delivery/express industry in the U.S. and globally dealt with significantly lower volumes coming from a still relatively high COVID-19 level and a tougher economic climate, which causes more careful consumer spending and, therefore, also fewer packages to be shipped.

In fact, it results in lesser global trade, which impacts the business of industry giants like UPS, Deutsche Post, and FedEx. Each of these saw volumes and revenues decline.

Therefore, I am pretty glad to see growth turn positive again, even if it’s compared to a low base last year. There is a clear, improving trend, which has been in part driven by further market share gains by FedEx, according to management, and verified by data we highlighted in January.

The most recent 2023 data shows that FedEx saw its market share in U.S. parcel delivery grow to 32%, at the cost of its close peer UPS, which saw its market share decline by 2% to 35%. Meanwhile, Amazon continues to gain market share, now sitting at 14%.

The most important takeaway is that FedEx is still gaining market share, helping it outgrow its peers in volumes and revenues. This is helped by the company’s solid e-commerce portfolio, strong global network, and solid delivery statistics like best delivery speed and coverage.

And there is more improvement on this front ahead as well, through management’s Network 2.0 reorganization. As of June 1st, FedEx no longer operates a Ground and Express segment as two separate companies as these have merged into “One FedEx,” which brings with it significant efficiency gains.

In simple terms, whereas FedEx used to operate as it existed out of three separate companies, splitting ground, express, and freight, going forward, it will function as one single company, merging operations, personnel, and systems. Obviously, this offers the opportunity for significant cost savings as this is a much more efficient business model, much closer to that of UPS. This alone should result in $2 billion in cost savings, which is significant.

However, it not only allows it to cut significant costs, but FedEx believes it will also result in a more streamlined operation, resulting in better delivery times and better customer service.

Finally, looking at the full-year results, FedEx reported a revenue decline of 3% or $2.5 billion to $87.7 billion, which is in line with expectations and reflects current weakness. All things considered, FedEx didn’t perform all that poorly, especially as management indicated that, while volumes continue to stabilize, there is no real increase in demand yet. This is pretty much in line with what we see in the global economy, so there are no real surprises there.

However, the real highlight is found on the bottom line.

Management is delivering on its promises

Through its Network 2.0 and DRIVE programs, FedEx promised investors to deliver $6 billion in cost savings on a 2021 basis, with $4 billion realized by 2025 and another $2 billion by 2027. This is what I wrote last time out:

“Most of the program is focused on achieving efficiencies in the Express segment and restructuring its operation by reducing routes and deploying crews, aircraft, and commercial linehaul more efficiently. Meanwhile, the largest cost-saving initiative is lowering the number of flights by focusing on cheap transportation options instead of fast delivery, which is in line with the priorities of FedEx customers.”

You see, in recent years, FedEx has seen its margins tumble as it fell further behind UPS in terms of operating efficiency. For reference, the operating margin fell by 33% from a 2017 high of 9% to a 2023 low of 6%, as it steadily decreased. The business has simply become less efficient every single quarter. Just take a look at the cost comparison to peer UPS, which has very similar operations.

However, in recent years, under a new CEO, FedEx has decided to turn the wheel and transform its operations to focus on efficiency. Yet, so far, the market hadn’t bought into management’s ambitious promises up until last week.

But boy, did management deliver this year. It is no secret that Wall Street had many doubts about management’s ability to execute its ambitious cost-cutting plans, but it has now shown it is fully capable of doing so, which may have surprised Wall Street and investors a bit.

After just a few quarters of the DRIVE program, FedEx is showing clear and impressive progress in reducing capital intensity, which has already resulted in impressive bottom-line gains in fiscal 2024, even though the top-line performance was far from impressive.

The company has already hit several targets it initially laid out for 2025, including reducing capex to below 6.5% of revenue. This shows that on certain targets, FedEx is already one year ahead of its “ambitious” schedule, which is pretty damn impressive.

Management met its target of $1.8 billion in structural cost cuts for FY24, coming from $500 million in savings from its air network, $550 million from lowering G&A costs, and $750 million from its ground operations. This is how management broke it down during the earnings call for those interested:

“In our air network, structural network transformation and reduced flight hours drove the Q4 savings. Within G&A, we realized procurement savings by centralizing third-party transportation, short equipment, and outside service contracts. Our surface network continued to maximize the use of rail. As part of that effort, freight now handles nearly 90% of the volume, up from about 25% just one year ago. Looking ahead, we are firmly on track to achieve our target of $4 billion of savings in FY 2025 compared to the FY 2023 baseline.”

As a result, FedEx reported FY24 earnings at the high end of the original guidance, even as revenue came in lower than expected. For the full year, EPS was up 19%. ROIC improved by 120 bps to 9.9%. Also, FY24 operating income was $6.2 billion, up 16% YoY, driven by a 110 bps margin improvement.

For Q4, these cost cuts resulted in a very impressive YoY performance, even as revenue grew only 1%. The adjusted operating margin expanded by 40 bps to 8.5%, resulting in an operating income of $1.34 billion.

Further down the line, this resulted in Q4 EPS of $5.41, beating estimates by $0.04 and up 10% YoY.

Overall, this is just a very impressive bottom-line performance.

Also, as Capex came down significantly this year, full year FCF grew to $4.1 billion, up 14% YoY. Most of this FCF management returned to shareholders to fully profit from the depressed share price, returning a total of $4 billion, with $2.5 billion coming from share repurchases and $1.5 billion from dividends.

And with capex expected to come down further in fiscal 2025, management expects even more FCF growth, which has urged it to scale up its shareholder returns. It announced another $2.5 billion in repurchases, including $1 billion to be deployed in Q1 alone.

In addition, FedEx announced a 10% increase in the dividend, which follows a 10% increase last year. As a result, shares now yield just below 2% based on a payout ratio of just 29%, which is very compelling, especially considering FedEx's earnings growth ahead.

Looking at current analyst earnings projections, FedEx could report almost $27 in EPS by the end of fiscal FY27. If the payout ratio grows to 50%, getting closer to that of UPS (currently at 80%), investors are in for a dividend growth CAGR of 35%. Even if the payout ratio stays flat, this results in dividend growth of 13.5% annually, making this a compelling dividend growth stock as well.

Outlook & valuation

What’s ahead is most important to investors, so let’s take a look at the outlook. In fiscal 2025, management expects a moderate improvement in demand, driven by a slight improvement in ground volumes and a more robust recovery in express. Revenue is expected to grow by low to mid-single digits as a result.

Management added that e-commerce inventories are low, which could boost global shipments if demand improves. Also, Red Sea disruptions could force additional volumes to move to air freight, which would benefit FedEx as well.

This expectation also includes the news of USPS not renewing a big FedEx contract expiring in September, which is anticipated to be a $500 million profit headwind. Management claimed that this will help it drive more efficiencies and create more flexibility, but obviously this is a pretty big loss for FedEx, impacting 2025 financials.

Still, revenue growth is looking pretty good and management still expects FY25 EPS growth of 12-24% (18% at the midpoint), driven by the DRIVE and Network 2.0 efficiency gains. This also includes a number of cost headwinds, including $560 million of business optimization costs, $100 million of inflationary pressures, and an international export yield pressure worth $400 million. Also, fiscal FY25 will have two fewer operating days, adding another $400 million headwind.

Positively, DRIVE gains of $2.2 billion should largely offset this, resulting in the expectation of 15% growth in operating income, which is pretty great!

Finally, in the longer term, management believes a 10% adjusted operating margin based on $100 billion of revenue is achievable, which is in line with our expectations.

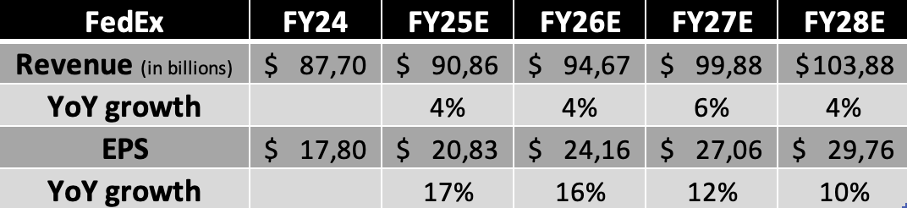

However, even as management fully delivered on its promises and is ahead of schedule, we are slightly nerving our expectations and financial projections to account for some additional economic weakness and some cost headwinds as a result. This way, we also de-risk our projections.

Nevertheless, the outlook continues to look pretty tremendous, as visible below.

Based on these projections, FedEx shares now trade at roughly 14x earnings, which is just cheap compared to the 17x investors are awarding to UPS. Also, this is a 25% discount to the sector average and right in line with its own historical multiples, while it arguably is in one of the best positions it has been in for a while. On a PEG basis, this translates into a PEG of 1, which is right around deep value territory.

In other words, FedEx continues to look extremely attractively priced, even after last week’s share price appreciation and my outlook cut. Therefore, I remain optimistic about FedEx shares.

Looking at the growth ahead, as well as the market share gains and its great position in the industry, I would argue that a 16x multiple is the very least investors should be willing to pay for FedEx shares. This would still leave it at a discount to its larger peer and the industry as a whole.

However, based on this multiple and my FY26 EPS projection, I still calculate a target price of $387. This leaves investors with potential annual returns of around 15%, which should easily beat global benchmarks despite the company's defensive nature.

Therefore, I argue that shares remain in deep value territory. Even based on conservative estimates, FedEx seems like it can turn into a tremendous investment, even if you missed out on the 20% gain in the first half of the year.

In conclusion, I rate shares a very solid “Buy.”

If you enjoyed this format and would like to see similar posts in the future, please hit the like button, share your comments, and be sure to subscribe.

In my opinion, Fedex isn’t the best opportunity to buy right now, as they have 5.64 billion in cash and 37.51 in debt, they have a profit margin of 5.02%. Their net income growth is very unpredictable. Roic is at 6.38%. I think that Uber, Intuit and Duolingo as well as Google are good buys right now. But anyway a very good article.

So comprehensive!