Booking Holdings Inc. – Delivered a blowout Q1

In this post, we examine Booking's sublime Q1 results, updating our view of the company, financial projections, and target price.

Unlike its close peer and competitor Expedia, whose shares fell by 15% post-earnings, Booking BKNG 0.00%↑ shares gained roughly 3% post-earnings last week on a blowout quarter and simply sublime performance. This once more highlighted Booking remains the undisputed travel leader and continues to outgrow its peers, taking market share.

Wall Street has consistently underestimated booking, mainly due to a perceived weak moat. However, as I laid out in my prior post on the company, its moat is strengthening by the day, it continues to outperform, and peers seemingly have trouble competing, including Airbnb.

Over the past decade, booking Holdings Inc. has consistently outperformed global benchmarks, with its shares gaining over 200%. This robust growth can be attributed to the company's excellent business performance, which has seen its revenue grow at a CAGR of 12%, even in the face of the COVID-19 pandemic.

Positively, today, the company looks stronger than ever and well-positioned to keep delivering above-average returns and to continue outpacing its peers in terms of growth despite its size. Booking today is a $120 billion market cap business, with a significant 40% global market share in the digital travel industry, far ahead of close peers Airbnb and Expedia.

Remarkably, despite its significant size and incredible market share, it consistently outgrows its two closest peers, taking more market share and further adding to its moat. It is about time this business gets the recognition it deserves, and its latest quarterly results once more confirm this.

For those unfamiliar with the business and looking for a deep dive into this OTA leader, check out my March post on the company here. Today, I’ll examine its most recent financial results and underlying developments and update my financial projections and target price.

If you are new to Rijnberk InvestInsights, also make sure to check out our last post on Qualcomm below.

Posts coming later this week:

Uber

Infineon

Booking delivers a perfect quarter

Booking Holdings reported its Q1 earnings on May 2 and blew away the Wall Street consensus. Booking reported revenue of $4.42 billion, up 17% YoY and beating the consensus by $160 million.

Growth has steadily normalized after the post-COVID recovery in recent years but remains solidly in the double digits, driven by market share gains and a healthy operating environment. Travel demand remains relatively strong, considering economic headwinds and declining consumer spending.

Still, shareholders shouldn’t take this performance for granted as it is still significantly better than peers. For reference, Expedia, which reported on the same day and operates in roughly the same industry, saw revenue grow by just 8% YoY, which is significantly slower than Booking, highlighting its excellent performance.

Driving this strong top-line performance is very healthy growth in room nights booked, up 9% YoY to over 300 million nights for the quarter, exceeding expectations. This was driven by very healthy underlying demand, a stronger-than-expected performance in Europe (up high single digits), and a limited impact from the war in the Middle East.

Meanwhile, nights booked in Asia were also up by mid-teens, high single digits in the rest of the world, and low single digits in the U.S., with the latter reflecting some economic struggles. However, even in the U.S., which is Expedia’s focus market, Booking was able to outgrow its competitor.

Supporting this growth is the solid progress Booking is making in alternative accommodations, with room night growth of 13% in Q1, now accounting for 36% of all nights booked, up 300 bps from last year. This shows that alternative accommodations continue to be a growth driver for Booking, supported by solid growth in accommodation offerings.

This led to gross bookings growth of 10% YoY for the whole group, which was also ahead of expectations. This was slightly ahead of nights booked growth thanks to slightly higher room night prices and a positive impact from flight booking, which also grew by 33% in the quarter.

This very solid top-line performance also translated to the bottom line, helped by relatively limited cost growth. Marketing expenses, one of Booking’s largest costs, were up only 6% in Q1 and down 15 bps as a percentage of gross bookings. This was thanks to a higher ROI and an improved mix from direct channels that don’t require marketing investments.

In addition, fixed expenses were up only 11% YoY, further fueling bottom-line leverage. This allowed Booking to report a 53% growth in EBITDA to $900 million. This reflects a 500 bps YoY improvement in the EBITDA margin to 20.4%.

This led to a net income of $700 million and an EPS of $20.39, up 76% YoY and beating the consensus by a whopping 44%. This was driven by a higher EBITDA margin and helped by Booking’s significant share repurchases program, which brought down the share count by a substantial 9% YoY.

Further down the line, this all resulted in an FCF of $2.6 billion, which, together with a debt issuance of $3 billion, allowed Booking to grow its cash position to $16.4 billion against a similar debt position, leaving it in solid financial health.

Booking is exceptionally well-positioned

As said at the start of this post, we continue to be bullish on Booking’s long-term prospects and believe the business is better positioned than ever to benefit from growth in leisure travel demand, which is expected to drive very solid growth in the OTA (Online Travel Agency) industry with a projected CAGR of close to 13% through the end of the decade, according to Verified Market Reports.

Management has several strategic priorities, which it discusses and updates each quarter, which should allow it to grow its market share further and outgrow its peers.

However, before getting to these developments, though, it is worth explaining Booking’s moat, which is built on the fact that it is still the undisputed leader in the OTA market with a 40% global market share, mainly thanks to a very strong position in Europe and Asia.

(Note that Booking Holdings includes multiple travel brands showed in the graph below, together capturing 40% of the market)

Crucially, this significant market share gives it a substantial edge over its peers. You see, within the online travel industry, the platform with the largest and broadest offering is the most interesting to the consumer. Why would I use another platform if the Booking platform offers the most convenience and always seems to have what I am looking for? I don’t.

This is an important part of its moat as it creates a virtuous cycle. Its current leadership position attracts a large number of consumers who are likely to stick with the platform for the simple reason of convenience and competitive pricing.

Thanks to its leadership position and massive user base, accommodations, rental companies, and airlines are also inclined to use the booking platform as it gets them exposed to the largest number of consumers, which then further grows Booking’s offering and also gives Booking a strong negotiating position to keep prices competitive. The platform is simply too important for hotel chains and other accommodation formats.

I hope you can see where I am going here. Booking's current leadership position puts it in the perfect spot for both consumers and accommodations, leading to further market share gains. This makes Bookis ’s leadership position hard to beat and creates quite a strong moat, which shouldn’t be underestimated.

Notably, while its tech stack (which is also best-in-class) might not be too hard to replicate and its business model seemingly not too hard to disrupt (in the end, the Expedia offering isn’t much different), the popularity of its platform and brand, and the way consumers trust the platform, is.

This is often overlooked, but it is what has allowed Booking to grow as strongly as it has over the last decade and what has allowed it to fight competition rather well.

In addition to this strong moat it already possesses, management also has a solid strategy in place to increase the value of each user and win over more customers, focusing on a number of strategic priorities.

These strategic priorities include its connected trip vision, expanding its merchant offering at booking.com, developing AI capabilities, and enhancing the genius loyalty program. These are all aimed at creating a seamless and inclusive user experience, which should lead to further market share gains and higher value per user.

While these might not seem overly impressive or ambitious, we believe this is precisely what Booking should focus on in its position. I mean, it already owns multiple leading travel platforms and now needs to build on this moat, and these strategic priorities seem perfect when well-executed.

What exactly management hopes to achieve through these focus areas is best explained by their CEO:

“By creating a much better experience for our travelers and solving more of the challenges they face when planning, booking, and experiencing a trip, we believe travelers will choose to book directly and more frequently with us, resulting in increased loyalty over time.”

Management is already seeing these efforts pay off, with the number of total active travelers growing and repeat travelers increasing. Also, connected transactions, defined as multiple products booked for a single trip, grew by 50% YoY in Q1, now accounting for a high single-digit percentage of Booking.com's total transactions in Q1, highlighting that management’s strategy is working.

Apart from deriving more value from its travelers by offering more products and a more seamless booking experience, management also sees the addition of new travel verticals like air tickets, rental cars, and experiences (part of the connected trip vision, which focuses on offering all travel aspects on a single platform) leading to healthy growth in new customers. This is what management said about this:

“We continue to see a healthy number of new customers to Booking.com through the flight vertical and are encouraged by the rate that these customers and returning customers see the value of the other services on our platform. Winning a traveler's business is never easy because of the high level of competition in our industry.”

Finally, AI and its growing loyalty program also continue to be important focus areas that can help Booking strengthen its leadership position. With regard to this, management said the following:

“As we have discussed before, our teams continue to work hard to integrate generative AI into our offerings in innovative ways, including booking.com's AI trip planner, price wise generative AI travel assistant named Penny and Kayak's recent release of generative AI powered features and tools.

In sum, we believe Gen AI will lower our customer service costs per transaction over time and improve the customer experience. Our Genius Loyalty program, booking.com, also plays an increasingly important role in the multiple elements of travel that we offer. As we expect, our travelers will be able to experience the benefits of Genius in each of our travel verticals over time.”

Overall, we believe these efforts will benefit Booking over time and will help it extend its lead over its peers. Booking has proven it knows how to improve its platform and invest its resources, proven by its historical growth profile and an impressive 35% ROIC (WACC of 11.5%).

While it might be tough for the company to keep growing its market share in a normalized environment and in the face of growing competition from Airbnb and Expedia, we certainly don’t expect significant market share losses.

We’ll say it again: Booking’s moat is much stronger than many believe it to be. Wall Street has been proven wrong over the last decade, and I expect the same to happen over the next decade.

On that note, let’s examine the outlook and valuation to determine the attractiveness of the shares today.

Outlook & Valuation

Looking ahead to next quarter, management now expects room night growth of 4-6% in Q2, a deceleration from Q1 due to a shorter booking window and a more significant impact from the Middle East war, which seems to be only escalating further. Positively, in April, room night growth was at the high end of this guidance range when adjusted for the easter shift.

Regarding gross bookings, management now guides for 3-5% growth, which is sitting below room night growth due to a roughly three percentage points negative impact expected from FX, partly offset by higher prices and flight bookings. This translates into a revenue growth expectation of 4-6%, again including the impact from FX. At the midpoint of the range, this translates into revenue of $5.8 billion.

On the bottom line, management now projects an EBITDA of between $1.7 billion and $1.75 billion, which actually is projected to be down by low single digits YoY “due to about seven points of pressure from the shift in Easter timing and about two points of negative impact on growth from changes in FX,” according to management.

Excluding these external factors, EBITDA would have been up in the mid-to-high single digits, reflecting a normalizing demand environment. While demand remains healthy, this slowdown was very much expected.

Overall, this is still looking pretty good!

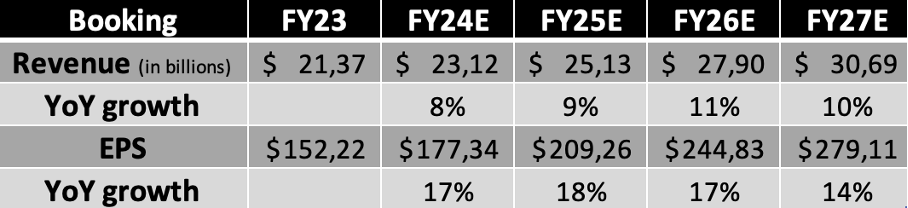

As explained before, we remain bullish in the longer term, and following this blowout quarter, we do not see much reason to meaningfully change our financial projections for the next few years.

Based on these projections, which are actually slightly below the Wall Street consensus in FY24 and FY25, shares are now trading at roughly 20x earnings, which is in no way expensive for a company as dominant as Booking and with a growth outlook, as shown above.

It shows that Booking is now trading at a PEG of just 1.22x, which is far below its 5-year average, and while Expedia is looking cheaper across the board due to its recent struggles, Booking shares are looking far more attractive than Airbnb’s, trading at a PEG twice that of Booking and a multiple of 37x this year’s earnings and even 32x next year’s earnings.

Simply put, Booking shares are still trading at an unjustified discount. Even when assuming a conservative 21x multiple, I calculate a target price of $4400 by the end of 2025, translating into potential returns of over 12% annually from current prices of just below $3600.

Honestly, this looks quite attractive to me, especially considering that Booking has also recently become one of the most exciting dividend growth opportunities out there. While shares only yield 0.25%, considering a payout ratio of just 5% and a terrific earnings growth outlook, we can safely say this can become a terrific dividend grower.

Overall, we remain very bullish on Booking after an impressive Q1. Therefore, we maintain our buy rating!

Let us know your thoughts in the comments! Also, please leave a like if this post was of value to you!

Please remember that this is no financial or investment advice and is for educational and informative purposes only. We are simply sharing our views, actions, and opinions, which we hope will be insightful!